I want to validate my understanding on how to value the de-merged entities.

- The profit split between consumer and lab is roughly 60-40.

- The sales guidance is for each is 20% and 12%.

- So we get two entities after de-merger for my holding. What will be the starting share price for each of the entity? Will it be same? Of course market will determine it afterwards. If it is same then it likely that there will be large movements in stock price on first day/week?

Thanks in advance

Very disappointing Q1 numbers, just went through the presentation and Consumer division has done OK but scientific there is a collapse in the EBITDA despite 10% rise in sales, has anyone been able to figure out why?

Also when is the con-call scheduled?

I noticed some losses in subsidiary additions maybe due to Goel Scientific addition but is that the only reason?

Notes post con-call:

Q1FY24 - rev 250CR PBT - 10CR EPS - 0.63

- EBIDTA has actually been more or less the same YoY but PAT is very different. 8CR difference in PAT due to one offs (insurance in previous year and some acquisition costs this year) and depreciation has doubled YoY from 8 to 16 CR due to new furnace commissioning.

- LARAH growth remains song.

- Margins should improve due to raw material costs coming down however the marketing spends will increase and this could nullify any benefits.

- Any growth in scientific is due to acquisition of Goel Scientific.

- Klasspack continues to decline and this has resulted in EBIDTA margins halving yoy

- New borosilicate plant in Jaipur will start Q3. - this will result in 3-4x volumes in glassware and he is not confident of selling these volumes at the moment.

- Tubing expansion put on hold.

- Scientific margins there should show some improvement in Q2 itself.

- At the moment nothing overly exciting or overly depressing in terms of Q2/Q3.

- Long term target for consumer wear would be 1000-2000cr.

- Target ROCE of 24% for consumer in 2-3 years.

- Sticking to 15-20% in consumer and 10-12% in Scientific for FY24

Q2 FY24 was in line with other listed players. Not bad and not exciting either.

De-merger of scientific division on plan for January 2024 - Can it unlock more value?

Disc:invested

Today was the date of demerger. Can anyone tell the split ratio between and how much shares will be credited of Borosil Scientific? and when can we expect trading of Borosil Scientific? Thankyou

for every 4 shares of Boro Limited one will get 3 shares of Borosil Tech the new compay

As per recent concall, Borosil Scientific shares are expected to get listed in Jan 24

Spinoff date is today as per the company update:

https://www.bseindia.com/markets/MarketInfo/DispNewNoticesCirculars.aspx?page=20231129-4

3 shares of klasspack (will be renamed to Borosil scientific limited) will be given for every 4 shares for Borosil Limited being held today. Need to get details on when scientific limited will be listed and at what price it gets listed.

First management interview after spin-off

Company has announced the split of acquisition price.

Isn’t this too high for BSL? Current price (around 352) is 20% less to the price on 5th (i.e. 445). What could be the listing price of BSL given the split ratio of acquisition above. Based on this is there a further decline in the share price of BL?

It will be great if someone can throw light on this.

Borosil Q2 FY24 concall notes:

Before getting into concall details it’s important to understand various verticals in the business of Borosil limited:

- What I like about Borosil is, Shreveer Kherukha gives a very detailed update on all the verticals in his opening remarks and spends almost 15-20 minutes giving the overall update about the business. (+1 here for the management style).

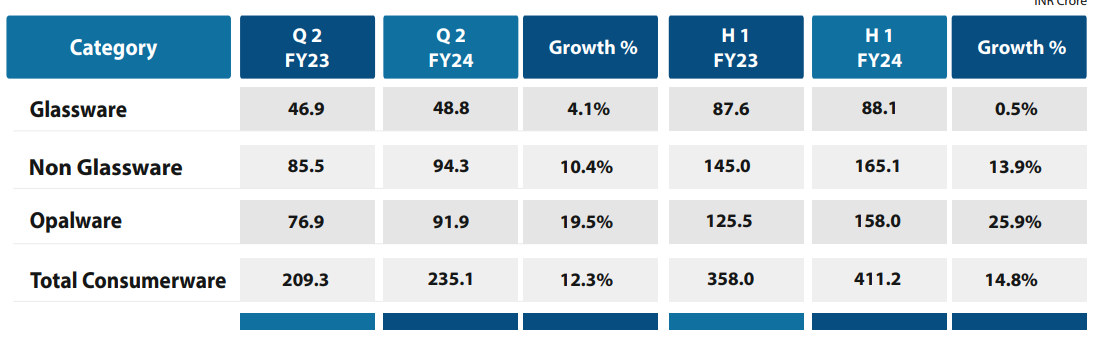

- Consumer business

- Glassware

- Non glassware

- Opalware under Larah

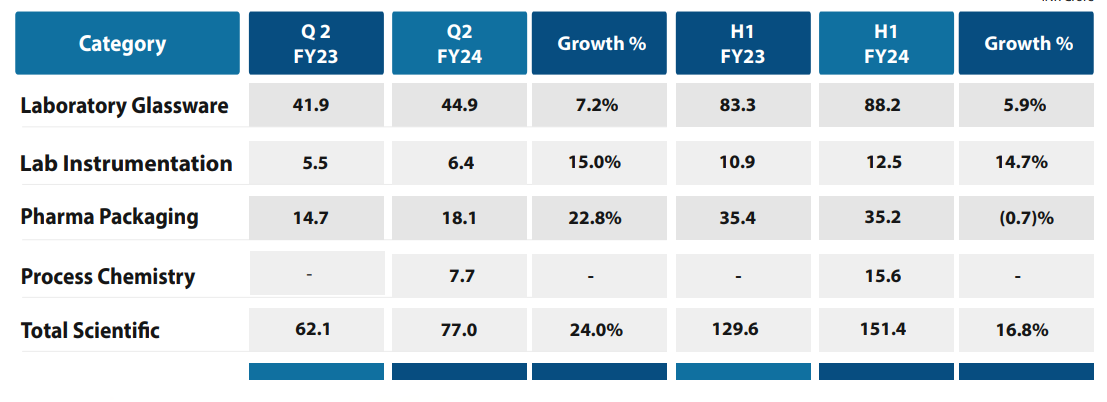

- Scientific business

- Laboratory glassware

- Laboratory instrumentation under Labquest

- Pharma packaging under Klasspack

- Process chemistry under Goel scientific (recently acquired)

- Scientific business will be demerged and will be renamed as Borosil Scientific Limited, 3 shares of scientific limited will be given for 4 shares of holding Borosil limited. Ex spin off date is 12/5/2023.

Financials

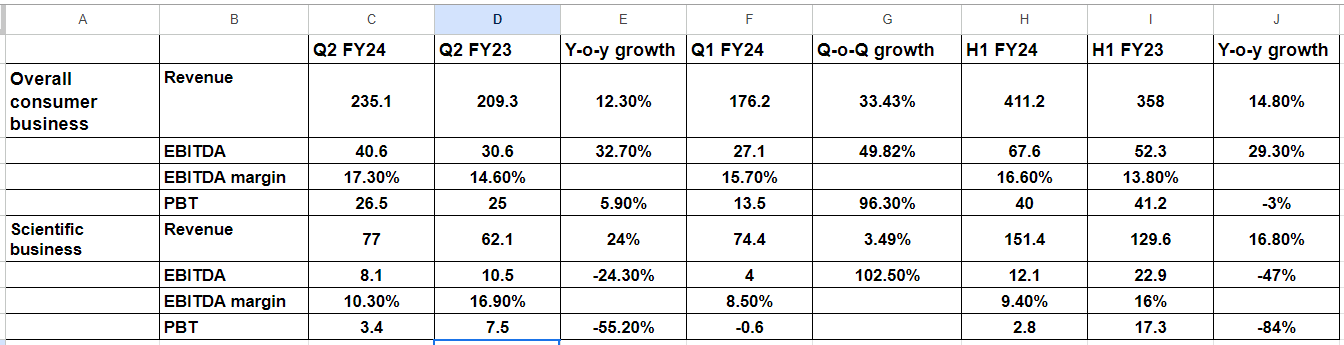

Segment wise revenue:

- Lower EBITDA in H1 is due to the account of following:

- Last year there was an exceptional gain of 5.1 crores due to insurance claims.

- This year there is one time expense of 2.8 crores towards the acquisition expenses.

- Lower profit is on account of:

- Higher depreciation to the tune of 20 crores due to the opalware furnace plant opening at Jaipur plant.

- Also the income from investments is lower by 2.8 crores this year compared to last year.

Consumer business updates:

- Opal ware capacity is running at 75-80% utilization, this is after upgrading the capacity to 84 tons per day from the previous 42 tons per day. Management expects increase in profitability with the 20% remaining sales, and expects to reach 100% capacity in fy25.

- Good growth seen across all ranges and channels (trade or large format retail). Several new products have been launched in the recent past. Roughly 20-30 new designs are launched every 6 months.

- Borosilicate presswork capacity of 25 tons per day will commence from Q4 fy24. Maximum capacity they can make it to is 42 tons per day in the same plant. Any new capacity be it opal ware or other things should be coming in a location.

- EBITDA margins should increase due to the operating leverage getting kicked in. H1-24 16.6% vs H1-23 13.8%.

- No capex planned for FY25, only maintenance capex.

- Diwali sales are neutral, that is nothing too exciting nor depressing.

- 10-15% of sales are coming from exports, focus is on domestic business now as realizations are higher.

- Current debt is about 215 crores and most of it is on consumer business.

Scientific business updates:

-

EBITDA margins: H1FY24 9.4% vs H1FY23 16%. This is due to losses in Labquest & Goel scientific.

- In labquest there are upfront costs for growing the technical team and R & D expenses are more than proportionate than the increase in revenues. Management expects this to take 2 years to normalize. The expenditure here is on people which needs to be upfront, once they become experts and deliver with the knowledge they gained over initial periods margins will start expanding. There is no gross block like consumer division here and is the reason for attractive return on capital.

- Goel scientific: this is due lower sales & higher fixed costs. Management expects this to stabilize once the synergies are put into place.

- Klasspack: Again due to lower sales(lower pharma packaging demand) & increased direct costs could not be passed on to customers. Things are improving in Q2 & should be even better in Q3.

-

Klasspack: Domestic sales are not good, export sales looking good. Two domestic customers had challenges. Lot of capex has been done in this segment but the capacities are very low at this point of time (around 40%). Lat 1.5 to 2 years are on a rough patch, focus is to improve on this to a state where they were 1.5 years back.

-

Goes scientific: Business acquired around early May. Ramping up on the process and expects another six months for the complete ramp up to align this with the Borosil setup. Focus is to expand the sales from this vertical (south India - no sales team, Hyderabad is a big market). Margin profile should be on a similar range as lab glassware vertical, but this is going to happen once the sales potential reaches.

- Acquired with a cost of around 50 crores, current capacity can do 100 crores of sales. Current sales are at around 50 crores.

-

Tubing facility capex is deferred by a year.

Other updates:

- Company spending around 40cr to set up a 6.5 megawatt solar project in Rajasthan, this should help save about 6-7cr of power cost per year.

- Tax rate for this & next year will be 25%.

What to look for in coming quarters?

- What kind of valuations Borosil limited and Scientific Limited shares get traded after the demerger?

- Margin expansion in the consumer business. Already improvement seen, should continue to improve further.

- Keep an eye on scientific limited business performance. Margins took a hit recently.

References:

- Q2 FY24 results: https://www.bseindia.com/xml-data/corpfiling/AttachHis/5759bd6c-6fac-4c14-9ed6-9ca15c7e958e.pdf

- Conall transcript: https://www.bseindia.com/xml-data/corpfiling/AttachHis/f7a1948c-bb4c-4a95-ac5c-599efe46033e.pdf

- Presentation : https://www.bseindia.com/xml-data/corpfiling/AttachHis/f58f2fd7-89f9-452f-95cb-3228761f3d1d.pdf

Overall I feel consumer business continues to do well with improvement in margins, whereas scientific business is facing headwinds and needs to be observed how management can sail this and turn around this vertical.

Disclosure: Currently forms about 3.5% of the portfolio. Might sell scientific business after listing and convert the same to consumer business.

I can’t comment on the whether there is further price decline in store for BL or not, but happy to share the way I have done a quick back of the envelope assessment on what this means as an investment (I am assuming the split has been done in a rational manner and am not commenting on why the split is as is)

-

First the split in equity shares is reflective of the book value of the equity shares (and not the market value). I assume we should see this split when we see shareholder’s equity in the independent balance sheet of the two companies. Current book value is Rs 68.57.Based on this, the Price-Book ratio for these two companies are likely to be quite different given the different nature of businesses. Consumer durable companies seem to have a wide range on Price-Book - somewhere between 6-14 (Havells, TTK, Blue Star, La Opala). Based on the closing market price and the share of book value as per the split, this would result in a 9.6 price to book for BL (Consumerware business). For the Scientific business it is more difficult to find comparables - but seems to be somewhere between 2.5-4 (AGI Greenpac, Tarsons) which would imply somewhere around Rs 95 (this is the value of a share before the swap ratio - so not the expected listing price which needs to be adjusted upwards for the 3 shares of Scientific for every 4 shares of BL. So prima facie there does not seem to be crazy differences with the way the market has priced it

-

For my investment decision, though I would need to build a more detailed P&L / cash flow for each business - which will only be possible once they separate out the accounts - from which I could do a DCF / get a forward PE ratio. However, the company does share PBT numbers (as well as segment wise assets to do a rough forward PBT/PAT assessment) enabling a basic back of the envelope calculation. At a very rough FY24 PBT margin of 12% for Consumerware (assumes a significant improvement in 2H. Unfortunately 2H FY23 was a struggle due to lack of capacity on Larah so difficult to know long term PBT margin), the FY24 PE would be ~50. You can then form a view on whether this is high or low - given the comparables, stage of business they are in, etc. Similarly, assuming a 9% PBT margin for Scientifc for FY24 (which is much lower than long term margins as per management - investments in Technologies, Klasspack demand challenges) - it works out to a FY24 PE of ~40 for Scientific at Rs 95 (pre swap ratio) - which definitely feels high - but could be argued is expecting a turnaround as investments start benefiting the business

I am less concerned about fall in price of BL (there is a price at which it would start making sense to buy more) - but face a similar quandary to you in terms of what to do with Scientific. What seems to be transpiring is that Shreevar Kheruka will probably remain as the CEO of the Consumer Business as they have announced Vinayak Patankar as CEO of Scientific. However this is a whole other discussion if that is of interest.

Hope this helps. Happy to be corrected on methodology if I have got it wrong or other more appropriate approaches exist

Disc. Invested for a long time and likely to be biased. Not a registered advisor - the above is just my approach and not meant as advice

Thanks for the update @akacker, this is really helpful.

Dear Members,

What is the tentative listing date for Borosil Scientific Limited?

These things take some time. I have seen this previously with TIPs. You should see INE02L001032 in your Broker account.

Anyone knows when are we going to see Borosil Scientific shares in Groww/Zerodha? People mentioned mid of Jan would be tentative date

One day it will show up. What is the hurry?

Shares would have already been credited in your demat account with klasspack name, Zerodha/Groww would show them once they are traded…

Excellent Q3 FY24 results from Borosil consumer division. YOY revenue growth of more than 45% with EBITDA, PAT growing 101% & 134%. Looking forward for the concall.

| Q3 FY24 | Q3 FY23 | YOY | Q2 FY24 | QOQ | 9M FY24 | 9M FY23 | YOY | |

|---|---|---|---|---|---|---|---|---|

| Revenue | 302.45 | 207.17 | 45.99% | 234.87 | 28.77% | 713.37 | 565.03 | 26.25% |

| EBITDA | 64.42 | 21.94 | 193.62% | 39.31 | 63.88% | 124.7 | 71.01 | 75.61% |

| EBITDA % | 21.30% | 10.59% | 101.12% | 16.74% | 27.26% | 17.48% | 12.57% | 39.09% |

| PAT | 37.3 | 15.93 | 134.15% | 18.54 | 101.19% | 60.79 | 48.73 | 24.75% |

| PAT % | 12.33% | 7.69% | 60.39% | 7.89% | 56.23% | 8.52% | 8.62% | -1.19% |