Schools and offices are reopening, this will give the much needed impetus for otherwise lagging glassware division. Remaining of FY22 is likely to be a fabulous one for Borosil.

1 Like

Excellent Q2 (both divisions) along with borosilicate glass tubing self-reliance initiative. Company seems to be benefiting from the focus obtained from the demerger. PBT of 1H FY22 gained momentum. Q3 festival season was remarkable for many consumer companies, borosil unlikely to be an exception.

Disc: Invested.

5 Likes

Hi when is the con-call for the results planned? Can’t find any information or the investor presentation for this Q

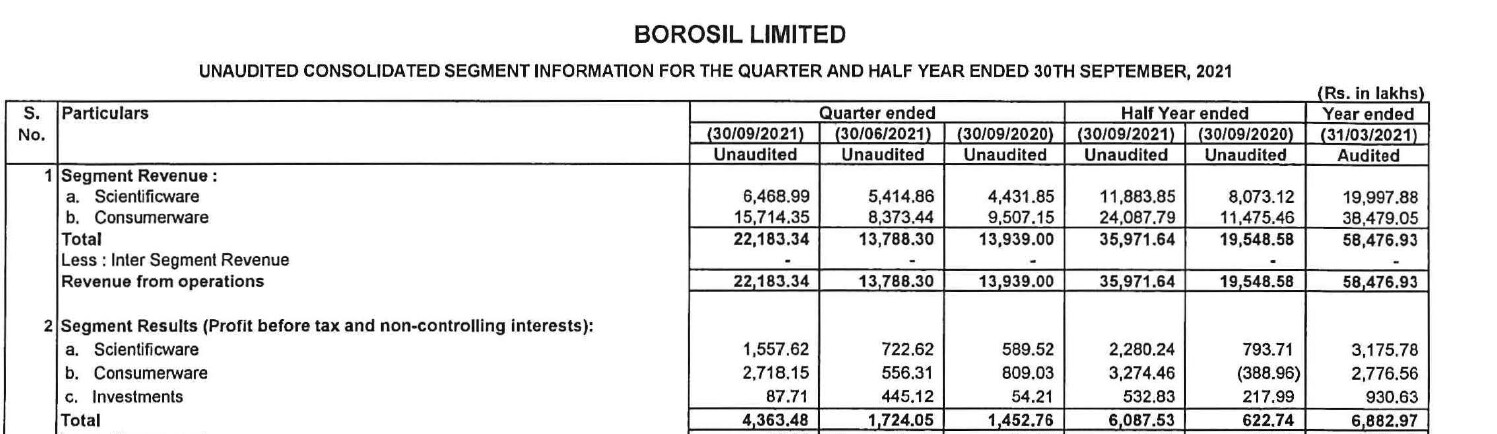

Borosil reported highest ever quarterly sales and profit in a non diwali quarter. From segmental results, one can notice big jump in profitability of scientificware division for a relatively lower increase in sales. Consumerware division is reaping rewards on productivity gains and brand awareness. This shows managements efforts on brand building have started paying off. I expect them to double down on their advertising and marketing spends which may keep margins under pressure for short term but will accrue big gains in the long run.

Their efforts on increasing opalware capacity as well as backward integration would provide necessary margin boost in years to come.

5 Likes

Concall is at tomorrow noon

1 Like

Concall Q2FY22.

1 Like

An interesting take away from the Con-Call for me was regarding the export competition. Schott-Kaisha is making a very similar product and is market leader in exports. As per Shreevar, both export and domestic pricing is similar so is BOROSIL moat in the domestic market really that strong?

Schott-Kaisha is only in scientific glass items (specifically pharma packaging) and not in scientific equipments (as per my knowledge). Also they have no presence in Consumerware which has more than 60% contribution to Borosil’s sales and profit. So roughly Borosil ~= Schott Kaisha+La Opala in terms of product offering.

Having said that, Schott Kaisha is the market leader in pharma packaging and Borosil is trying to gain more market share post acquisition of Klasspack. Hence Schott Kaisha has much bigger foot print in exports

2 Likes

Borosil appliance division seems to be doing really well. It is high time the division to introduce more products to increase its presence in the kitchen . I hope the management would consider their earlier thoughts on gas stoves, hob and kitchen hood etc - Inside kitchen, especially when there is a glass part in an appliance , it makes sense for Borosil to offer that product. Company’s strategy in opalware is playing out well.

Disc: Invested.

3 Likes

3 Likes

Any idea if borosil has any opportunity in semiconductor industry (considering use of borosilicate wafers ) , is company already into it ?Could be the recent price rise linked to the PLI announcement related to semiconductor industry ?

Additional investment in Subsidiary Company by way of subscription towards Rights Issue- Disclosure under regulation 30 of Securities and Exchange Board of India (Listing Obligations and Disclosure Requirements) Regulations, 2015. Pursuant to this, the holding of the Company in Klass Pack Limited has increased from 79.53% to 82.49% of equity share capital of Klass Pack Limited.

- This is a welcome move, this division can bring in additional growth. Klass Pack is already established as a credible No. 2 player.

Disc: Invested.

1 Like

Good coverage from monarch capital.

3 Likes

Brand promotion taken one notch up by launching TV commercial

1 Like

Borosil is at its very early stage of growth. Its brand name commands much a bigger market cap likewise havells or voltas etc. Product portfolio expansion without compromising much on the margin is the key. Company has recently launched high value products like room heaters:-

https://www.myborosil.com/appliances/home-care/room-heaters.html

Management focus and brand value is excellent as of now. Building on these can paint a remarkable growth journey!

Disc: invested.

4 Likes

Q3 result is out - on the expected lines. Listing of Klasspack is a major move, should help the fundraising easier for that division.

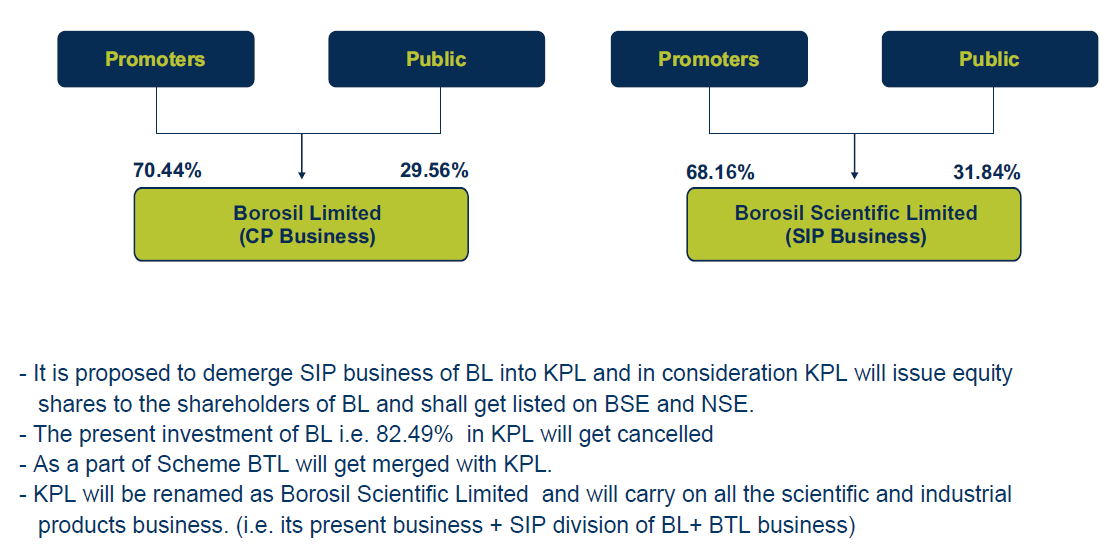

"The Board of Directors of the Company have considered and approved a draft

Composite Scheme of Arrangement amongst Borosil Limited (“the Company” or

“Demerged Company”) and Klass Pack Limited (“Resulting Company” or “Transferee

Company) and Borosil Technologies Limited (“Transferor Company”) and their

respective shareholders and creditors (“Scheme”), inter alia providingfor:

3 Bomsil Limited

BOROSlL OR:L3FIO(HQOICCCzm

a. reduction and reorganisationof share capital of the Resulting Company;

b. demerger, transfer and vesting of the Demerged Undertaking (as defined in the

Scheme) from the Company into the Resulting Company on a going concern

basis and consequent issue of shares by the Resulting Company and reduction

and cancellation of the existing paid-up equity share capital of the Resulting

Company held by the Company; and

c. amalgamation of the Transferor Company with the Transferee Company.

Post effectiveness of the Scheme, the equity shares of the Resulting Company will

be listed on BSE Limited and the National Stock Exchange of lndia Limited

(collectively referred to as “Stock Exchanges”).

The Appointed Date of the Scheme is April I,2022”

Disc:invested.

4 Likes

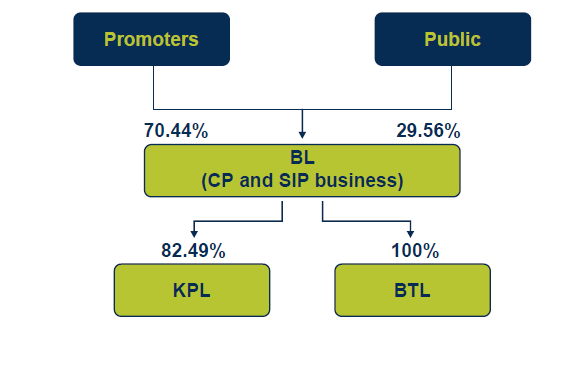

Current status

New structure

Simplifying the corporate structure further, unlocking value for the shareholders. Only downside - another 18 months of uncertainty for stock price due to merger demerger exercise, as happened in the case of Borosil Renewables and Borosil Ltd. It may provide opportunity for long term investors as short term guys get out putting pressure of stock price in the short run

11 Likes

As per the scheme:

“3 (Three) equity shares of INR 1/- each of the Resulting

Company credited as fully paid up (post proposed re-

organisation of share capital), for every 4 (Four) equity

shares of INR 1/- each fully paid up of the Demerged

Company”

i.e 3 shares of BSL for every 4 shares of BL held. isn’t it low considering BL already has 82.49% in KPL and 100% in SIP division and BTL? Can anyone please take a look at this?

There is some error in your calculations. For 9 months, Borosil Ltd has generated topline of 640 Cr so last qtr will be 210 Cr (to make it 850 Cr FY 22) which is in line with expectations. Please recheck

I took standalone instead of consolidated! My mistake i usually keep it on standalone for BRL since consolidated shows pre demerger data, the same continued for BL. Will delete earlier post thank you for pointing out!