When promoter holds 65% stake in BBTC, what any activist investor can do ?

Management never had intent to unlock value but still the stock has gone up 10 times in the past 10 years even after the underperformance seen for the past 6 years. Between 2006 and 2014, stock price remained same and then between 2014 and 2017, its a ten bagger. It is this underperformance for several years that is going to give high returns if gradually weightage in portfolio is increased every underperforming year.

Such deep value stocks are for different kind of investors who wish to invest for decades.

1 Like

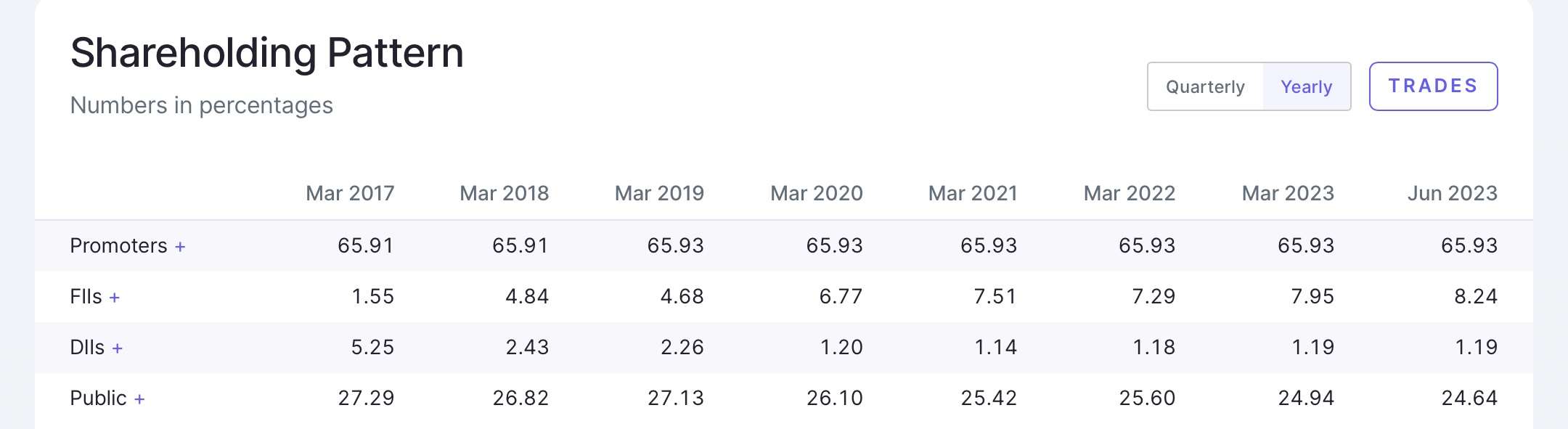

Check shareholding pattern above - Since BBTC high at 2100 … Price fell down but FII increasing holding continuously and Public holding also include Wallace brothers who has 8.11% holding.

Bombay dyeing restructuring and demerger of Bombay realty and Go first exit will add huge value to BBTC …

BBTC is exited loss making coffee estate and tea estates

Remaining Tea estate lease will end in 2026

So hereon BBTC has

- Auto ancillary

- Dental products

- Horticulture

- 24% stake in national peroxide

- 44% stake in Bombay Dyeing

- 50.5% Stake in Britannia

- Other hidden investments through complicated foreign subsidiaries

1 Like

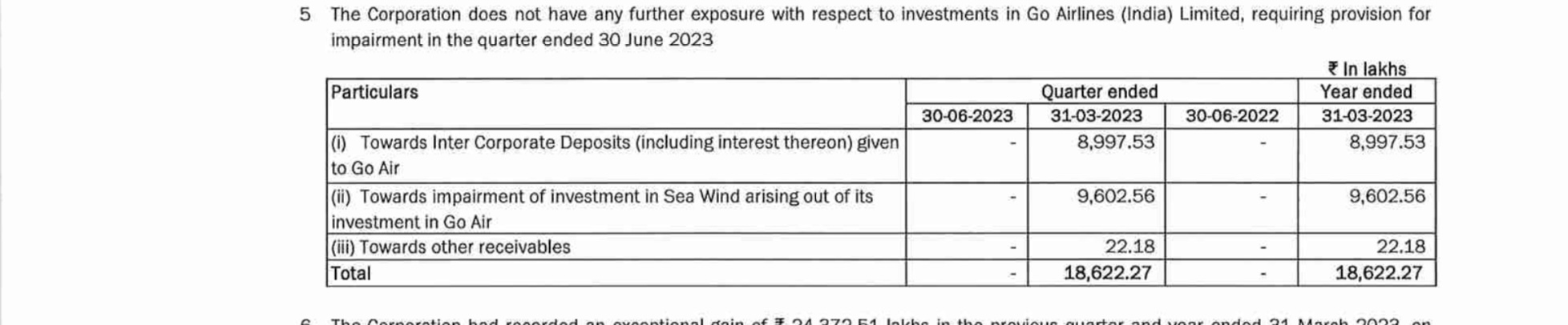

If I am reading right - Go air no more associate company and BBTC doesn’t hold any stake or provision toward it from here on.

So whatever happens to Go air shouldn’t be a concern for BBTC

- Bombay dyeing 5000 land deal can be game changer

- Even after selling coffee and tea estate , Go air and still why BBTC increasing Debt and raising more Money through debentures

Interest rate rising but BBTC is Debt is rising. Worst way to handle the cost

1 Like

So holding Bombay dyeing is better than BBTC right in that case?

1 Like

Some interesting points would like to include here:

Bombay dyeing MCAP 2500 crore

Debt - 3642 crore as of March 31

If Bombay dyeing successfully sell the land as they said at 5000 crore:

Bombay dyeing will be left with 800+ crore cash and debt free badge

Companies biggest drawback in interest paid on debt which eating up all Operating profit and end in huge loss

So Company can turn profitable company post land deal.

They have big land parcel at Worli and Dadar and 700 acre odd lands in Mumbai.

For real estate company biggest cost is land cost where for Bombay dyeing land is almost free of cost so margin of profit is very high.

BBTC offer better margin of safety as it holds Bombay dyeing, Britannia , National peroxide and its own business

1 Like

Today value of holdings BBTC in its subsidiaries or Associate companies

BBTC MCAP 8200 crore

Britannia - 56,000 crore

Bombay dyeing - 1335 crore

National Peroxide - 312 crore

Total 57,647 crore underlying holding value

Kama holdings MCAP 9800 crore

Underlying holding value 34,700 crore

Bajaj holdings Mcap 80,000 crore

Underlying holding value 1,49,372

1 Like

Comparing BBTC with Kama, Bajaj or even Maha scooter is wrong.

The other 3 gives good dividends, Kama has also done buybacks in past. Meanwhile, BBTC has an extremely complicated holding structure. Forget about dividend’/ value unlocking in near term.

Completely agree - all step-down subsidiaries! I don’t think even the dividends from Britannia get reflected in BBTC’s balance sheet due to this reason. I strongly feel this is an operator-driven stock which only provides a good swing trade opportunity every 24 months.

But situations are changing

- Go air closed

- Coffee and tea estate sold

- Remaining tea estate lease will end by 2027-2028

- Bombay dyeing will be debt free company , hoping for turning profitable too In future

- Now BBTC left with all Good businesses no more loss making businesses.

From past 1-2 year complicated structure seems to be reducing

BBTC slowly getting shares of Bombay dyeing and National Peroixde share through inter transfer

National peroxide is getting demerged into 2 companies. One is Naperol investment which has cross holding of BBTC and Bombay dyeing

Which give the hint They are in process of making BBTC ultimate holding company and Reduce the compli

So from here on Dividend from Britannia stay with company. Can’t say Whether they disburse it to shareholders by the way I’d buy back or bonus share.

Will ask all relevant questions in this AGM. Let see what will be their reply

2 Likes

On the National Peroxide demerger, today is the record date and can see that Market cap of National Peroxide is still 955 odd crores, which is more than sum of the holdings of BBTC and bombay dyeing which comes upto 800 odd crores. Am I missing something please.

1 Like

Naveen Jindal is understood to have put in an expression of interest to buy insolvent airline Go First

Would be great to know about your take on the top and bottom line of BBTC for the next 3-4 years

Valuation of BBTC is Depend upon following factors next 4 Years 2028

- Holding value of Britannia , Bombay Dyeing , National Peroxide

- Tea estate Lease will end in 2027

So at end of BBTC will be holding company where as management hasn’t shown any interest to do great things in auto ancillary and dental so it’s not useful to count here

-

Britannia Mcap by 2028 based on current EPS growth rate it can reach 2,20,000

50.5% is 1,11,000 crore

-

Bombay dyeing expect to achieve 15,000 crore revenue from new real estate projects

Based on that Bombay dyeing might easily cross 20,000 MCAP by 2028

44.4% - BBTC holding Value 9000 crore approx

-

National peroxide - 24% let say holding value is 1000 crore only

Total holding value of BBTC by 2028 can be predicted to be around 1,20,000 crore

———————-

Why does BBTC has huge discount to its holding value … reason are many example dividend pass out from Britannia

But due to few changes happening in 2023 could improve situation in future

- Debt reduction

- Increase stake in Bombay dyeing and National peroxide

- Go first has closed down

- Loss making coffe estate sold

5, loss making tea estate lease will end

So in conclusion every bad part in business have been and will be thrown out

So hope discount value will reduce drastically in days to come

Even 60% discount will be amounts to 72,000 MCAP by 2028

Which is share price could be around 10,000-11,000

5 Likes

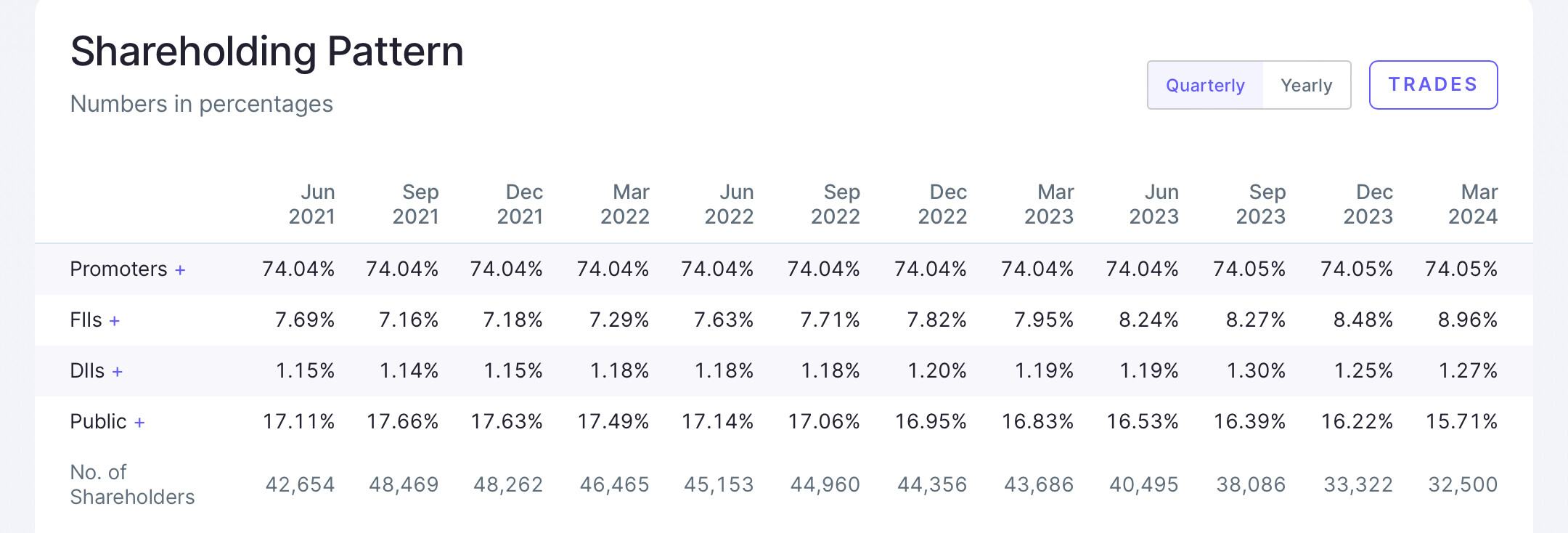

SHAREHOLDERS are decreasing and FII holdings are increasing

1 Like

FII DII increasing and Retailers reducing

Company has seen huge restructuring in last 2 years

Exited all loss making business in last 1 year

- Go air

- Tea and coffee estate

Now BBTC left with

Britannia 50.5% Stake

Bombay Dyeing 49.67% stake

NPL chemical and Naperol - 24% Each

Profitable standalone business - Auto components,Horticulture,Dental healthcare

Received 900 crore dividend in April month - hereon dividend from Britannia won’t be invested in loss making business … good days ahead

6 Likes

SEBI Special aucction in October can trigger the valuation for Holding companies like BBTC. Acction will give more Liquidity to the Holding companies which are been trading at huge discount as compared to Global peers .

2 Likes

BBTC not included in Sebi special auction this time , this is list of some of the companies schedule for special aucction.

Standalone biz:

- Stagnant since last 10 years, loss making at an operating profit level. FY25 Rev: 275 Crs and Operating loss: Rs 40 Crs

- Other income is what keeps the co. profitable, that are dividends from Britannia Inds.

- Promoter holding near 75%, no significant shareholder in DII and FII for BBTCL

Most valuable asset with BBTCL is its Britannia stake:

- Bombay Burmah through Assoicated Biscuits hold a 44.76% stake in Britannia Industries (stake currently valued at ~62,000 Crs)

- Current Yearly dividends from Britannia to BBTCL would be ~900 Crs

- The current mcap of Bombay Burmah is ~Rs 13,000 Crs, a significant discount to the stake it hold in Britannia.

Good things that have happened for BBTCL is shut down of Go First, thus no more further lending into the loss making airline and reduction of company debt by liquidating real estate assets.

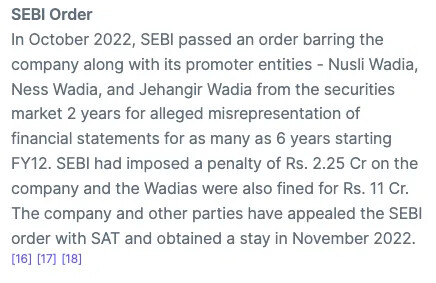

The major issue is to Corporate governance.

- Complex corporate structure with inter-company holdings and lack of transparency

- Found in Bombay Dyeing information:

I wonder whether one should even consider investing in companies with corporate governance issues when there are better companies available.

Disc: Not invested

4 Likes