And why would you think that SNF, which is a market leader with a lot of muscle power will not enter water treatment segment for powders? btw; the local production is <1%, so be it oil field or water treatment requirement, the 99% demand is met only through import from Europe and Asia.

As per environmental report of snf, out of 258k, 100k is for internal products

External market size is 200k

Will have to see if blaclrose can service the gap of 42k

1 Like

I sold off my entire position in Black Rose about a week ago @ around 130. Upcoming capacity from SNF is huge and could have an impact on the supply side. This was my concern so I booked the profits.

Thats understandable but SNF capacity is as follows

Acrylamide - 120K

100K of Acrylamide will be used again for Polyacrylamide

20K for merchant sale

Polyacrylamide capacity:

Powder 60K

Liquid 42K

Emulsions 36K

20K merchant sale + 138K costed 400 crore

Blackrose

20K acrylamide is for merchant sale

Polyacramide:

Liquid 40K

Solid 10K

source: https://www.bseindia.com/xml-data/corpfiling/AttachHis/86e13386-c65b-4dba-a012-52e9a11f759a.pdf

50K costed 60cr

Imports

Solid : as per blackrose filing when applying for environment permit, India imported 59K

Liquids : there was no import, I am not sure why both SNF and Blackrose went for higher capacity for liquids as all demand was already met. Most probably they anticipate due to requiremnts for cleaner water etc this will rise

source: blackrose environment report. http://environmentclearance.nic.in/writereaddata/FormB/EC/EIA_EMP/08032018SDWJSZMBEIAReport.pdf

I think Blackrose is still a very good bet as I dont think the market will not absorb the production. Maybe not 100pc production but for any expansion the idea is to have a little bit of room for further demand so it was never the plan to have a capacity to have 100pc absorbtion from day one

Just my thougths, do your own research but project execution, cost of project etc is all in Blackrose favour

Just because alibaba, ibm, microsoft have all introduced cloud computing doesnt make amazon cloud redundant. Where there is demand there cant be monopoly unless its via some very srewd marketing and business contacts

6 Likes

https://solenis.com/en/news-events/news/EMEA-polyacrylamide-price-increase/

The new polyacrylamide plant went live in January and prices of both acrylamidr and polyacrylamide have gone up however crude is down significantly as is butadiene and the raw material used by blackrose

The Chinese manufacturing probably has significant issues due the ongoing Coronavirus crises

Water treatment and probably other cleaning is need of the hour

could this be a big quarter for the company ?

1 Like

Water treatment is likely less now, since industries using water are shut. Acrylamide is useful not as any cleaner in general but only specifically as a flocculant (to trap fine particles) useful only for water treatment.

https://en.wikipedia.org/wiki/Flocculation

2 Likes

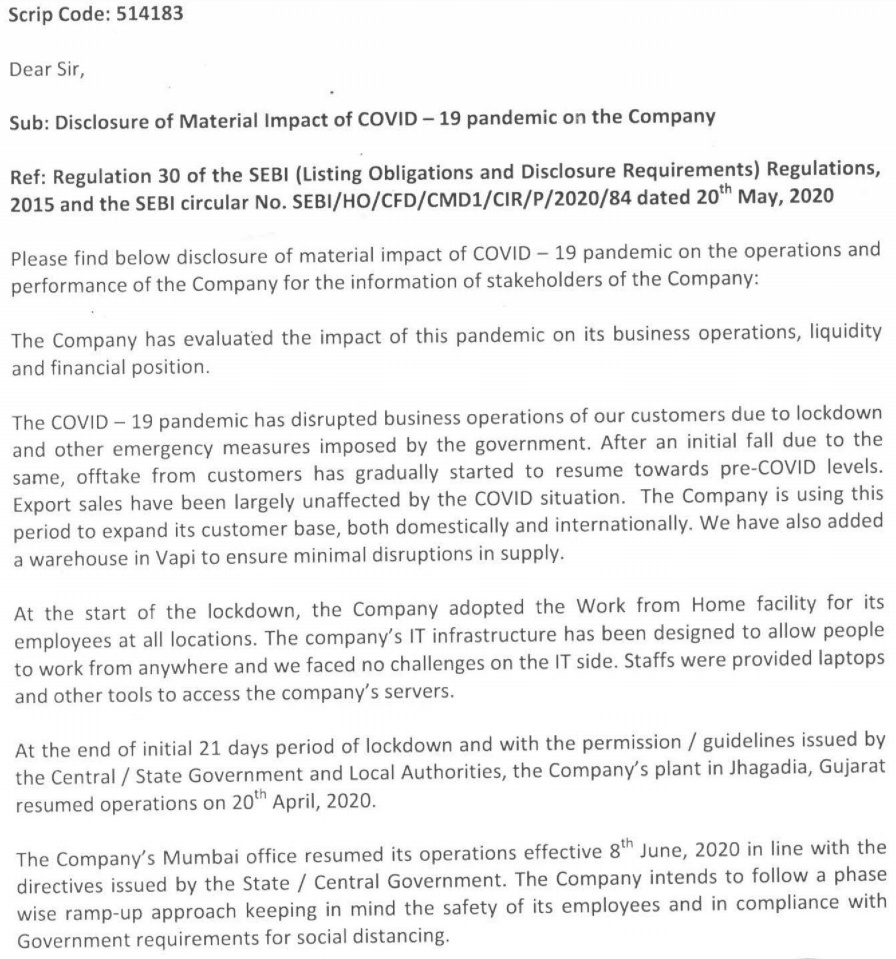

Covid impact, quite less, 3 weeks lost in Q1 FY21.

https://www.bseindia.com/xml-data/corpfiling/AttachLive/b7255794-fa90-4130-a717-9aaf732e59a2.pdf

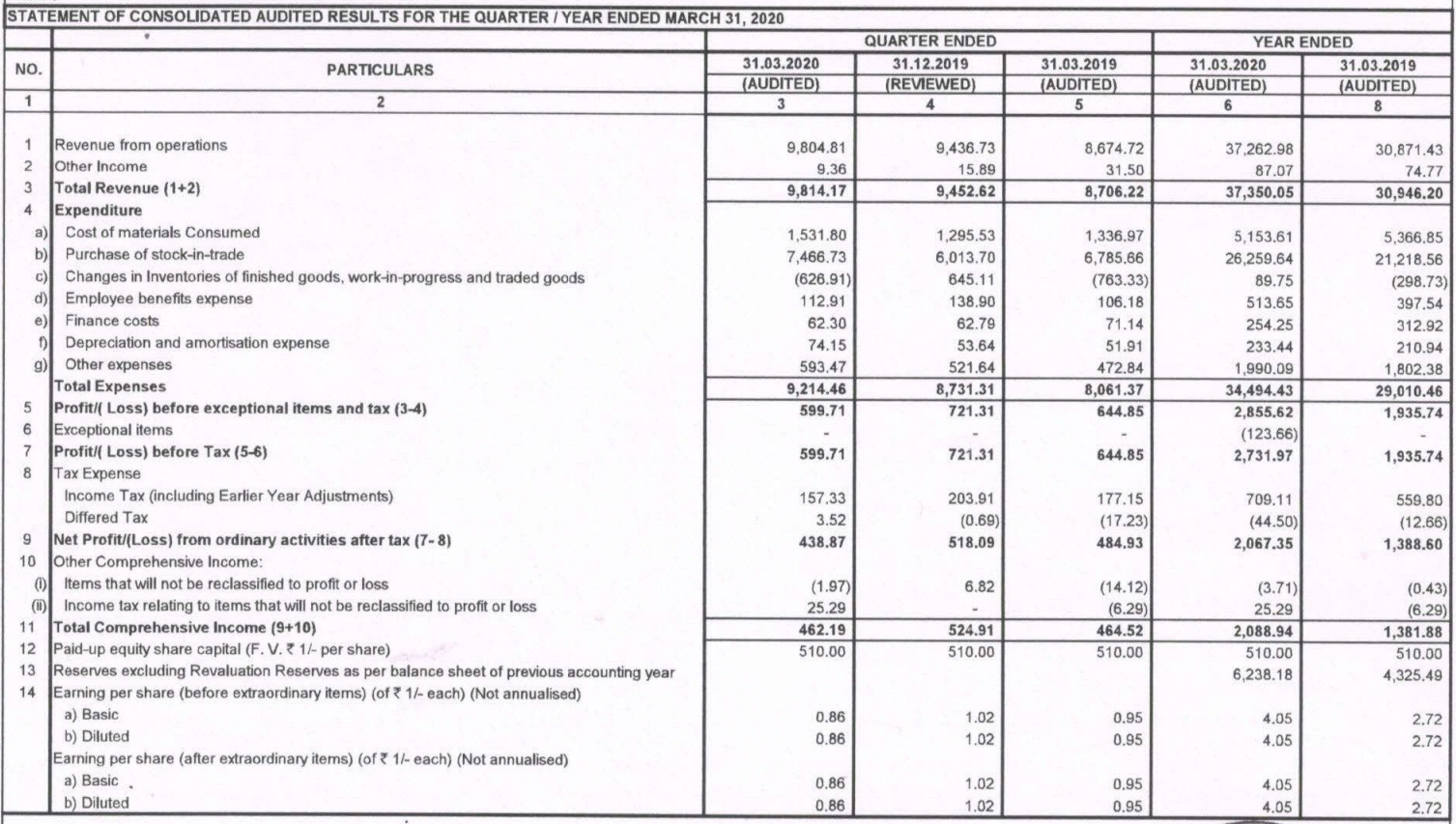

Q4 FY20 results are not bad, impacted by fall in INR.

https://www.bseindia.com/xml-data/corpfiling/AttachLive/4001d2dc-ce8e-4a7f-b910-b97f06c8e27d.pdf

Its actually a 20% increase from 3.5 lakhs pm to 4.2 lakhs pm.

Previous salary was not 42 lpa, there are taxes etc remember

2 Likes

Any idea on their product pricing trends in Q1/Q2 and also the raw materials pricing trends?

There has been some stock buying in last 3-4 days.

Thanks

As per annual report,they had done capex of around 60 cr.

But why it is not reflected in cashflow study

Their capex in

2020@7.66 cr

2019@1.09cr

2018@0.47 cr

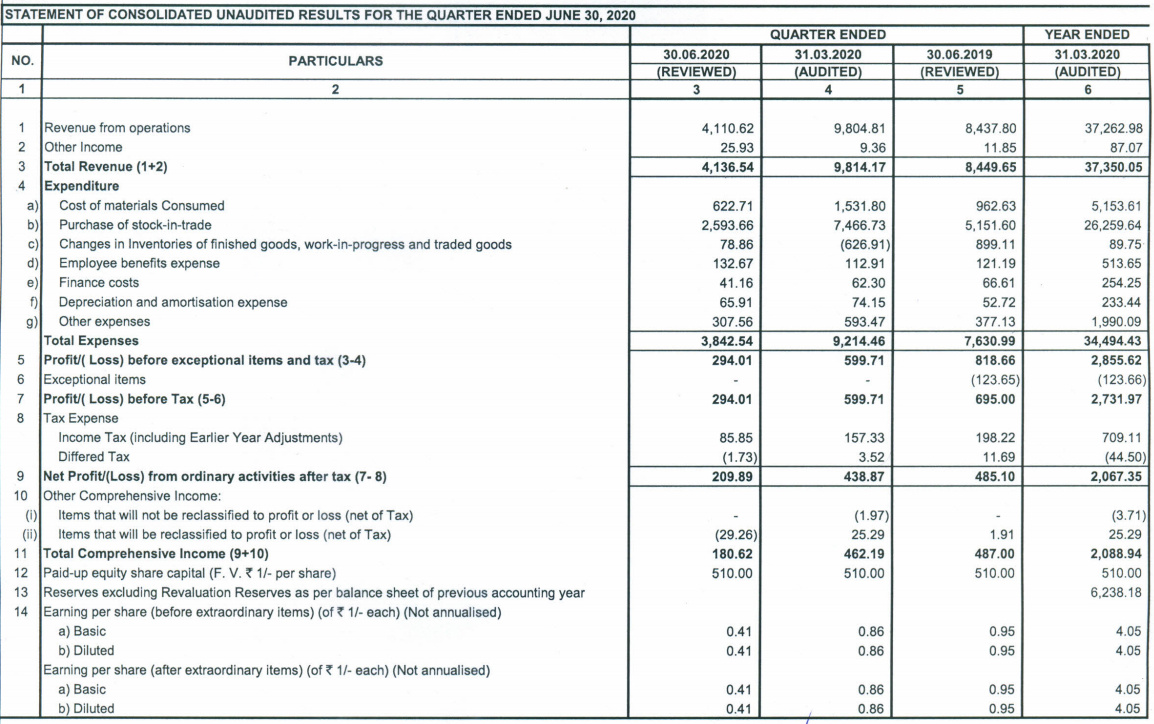

Q1 FY21 results:

As expected, covid impact, revenues and profits both fall by little less than half.

https://www.bseindia.com/xml-data/corpfiling/AttachLive/44f0a262-c7fd-45e0-b56c-3d7f417ad1df.pdf

1 Like

I have presented my views on BlackRose. Sharing it to everyone for reference. Views are welcome

Disclosure: Invested

6 Likes

Vishal, I think you have got a couple of data points wrong.

For ex:

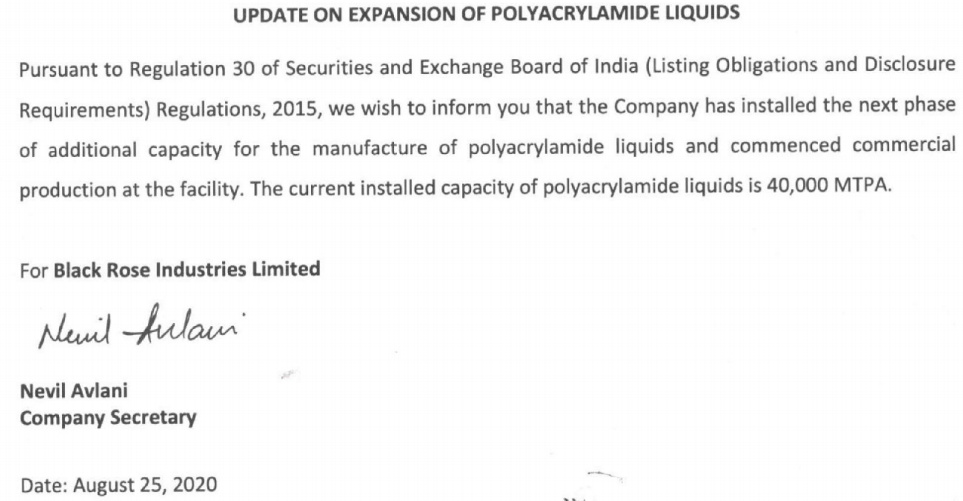

“Commencement of Polyacrylamide manufacturing plant would be expected to add EBIT of minimum 50 crores for the next couple of years with the production capacity of 40,000 MTPA”

The production capacity of 40,000 MTPA is for poly liquid which sells in the market for Rs. 25 per kg on an average. This can only give sales of around 100 cr for which EBIT of 50 cr is not possible. The main thing to focus on for topline and margins is poly solids which is much more technically difficult product to make (10,000 MTPA at a price of Rs.200-300 per kg) and it hasn’t started yet.

I also think you need to cross check your acrylamide nos. for FY18 and FY19.

Good effort. Liked the way you covered it.

Disc: Invested

10 Likes

Thanks @Vishal_Jajoo for the note and @salonihemnani011 for the clarification.

With the entry of SNF, we are looking at a combined supply of 40k acrylamide (20k each) for the Indian and export markets (since 100k of SNF’s production will be used to make poly).

We know that the Indian demand is around 20k and is growing at 8%. Assuming that BR and SNF will cover the Indian demand, there will still be 20k total surplus supply which they will try to sell internationally.

My question is, what are the kind of margins they will expect to get on these exports? If these margins are significantly lower than the domestic margins, then we can expect a bit of a price war in the domestic market as well which will not be good for BR.

Similarly for poly liquids, why has BR increased capacity in an already overcrowded market. Alternatively, will potential curbs on acrylamide imports restrict the poly production capabilities of other players in India?

Disclosure: Invested since mid 2018. Considering selling.

1 Like

Hi Vineet, Thanks for putting up these questions.

Regarding the 1st question, the company has mentioned in its presentation that exports in Acrylamide at 14000 capacity earlier already used to account for 45% sales and it has penetrated into US markets as well…so I don’t think there is need to worry about surplus capacity in domestic markets as the company has a balanced geographical approach in Acrylamide.

Disc: invested

4 Likes

Thanks for correcting the analysis. I made the mistake of presenting incomplete information, as well as error in examining the polyacrylamide liquid prices. Corrected the same.

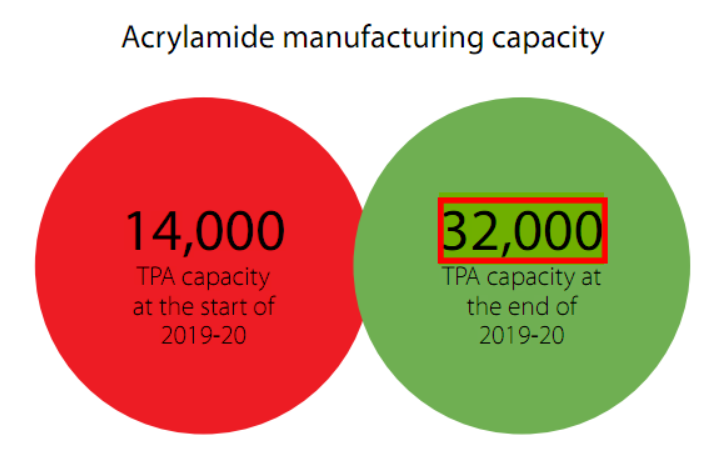

Has the company announced any expansion plans in Acrylamide, or it is a typing of error of 20000 MTPA? If anyone can clear this??

AR: 2019-20 PAge 10

1 Like

Quoting from the AR:

“The present capacity consists of 20,000 MTPA for merchant sales and additional capacity for the captive consumption of intermediate monomer for polyacrylamide manufacture”

1 Like