It has been a long time since I posted an update here although I have posted on company specific threads where I was invested or interested.

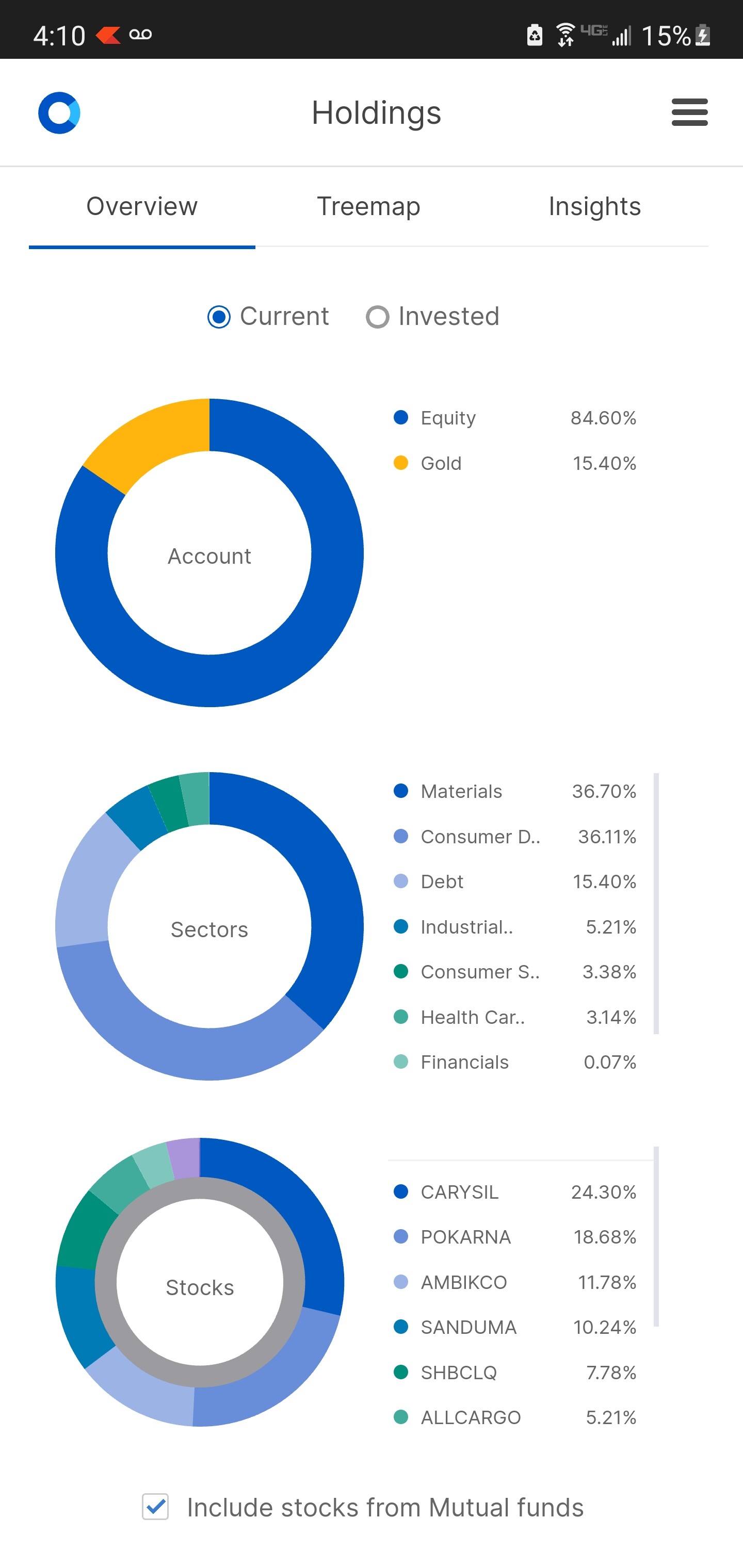

Following is the breakdown of the portfolio.

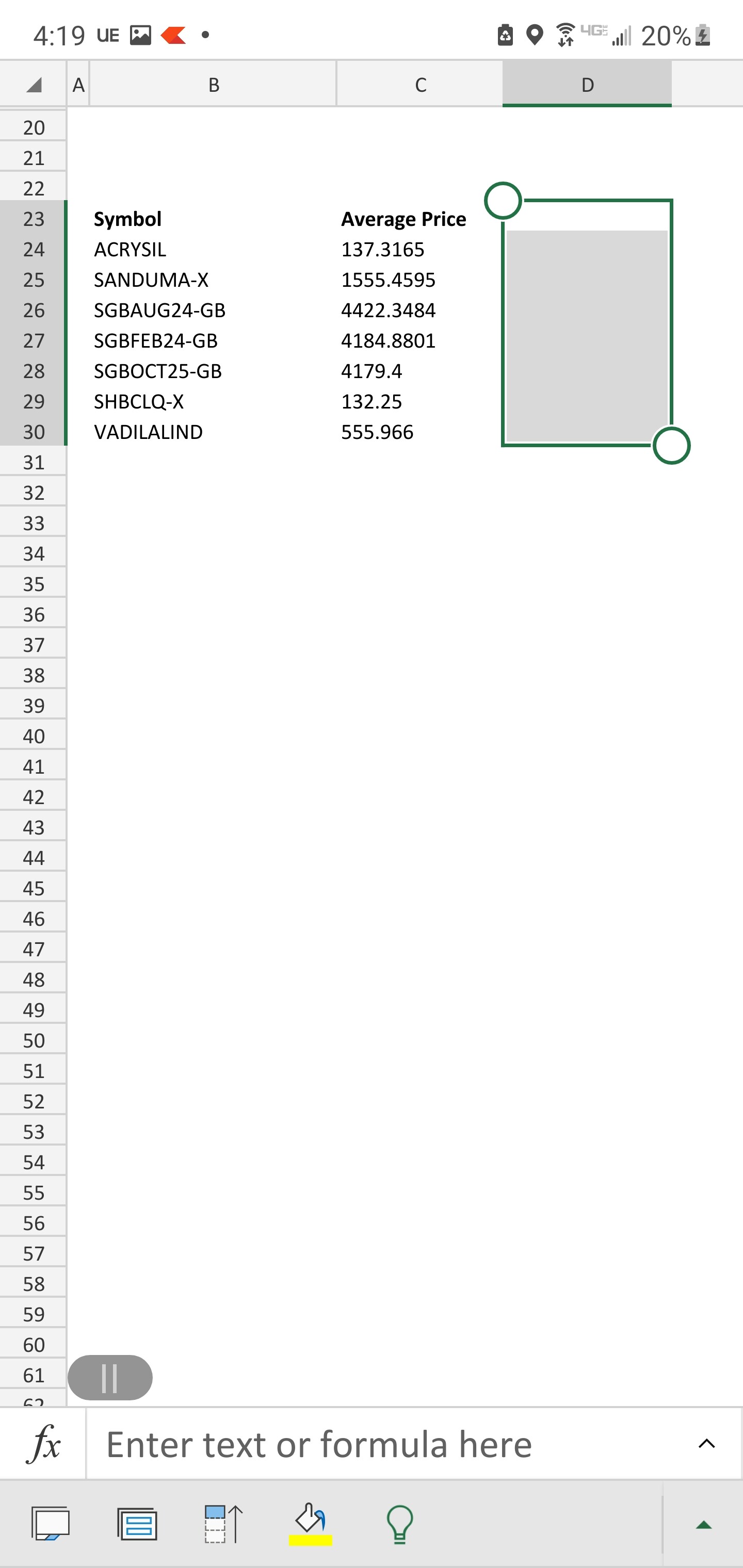

Stock. Avg buying price

Carysil. 180

Pokarna. 376

Sandur. 525

Ambika 1767

Allcargo. 128

Kopran. 192

Shivalik. 88

Vadilal. 555

It remains more concentrated than what I would like but I have been trying to follow a strategy which involves very low churn and focused investing as well as exploration.

There are many names which I was invested in but have booked profits when they ran up significantly. Some of these names are still very good but just felt that valuations were discounting the positive hypothesis already.

- Oriental Aromatics

Well positioned small cap in niche segment. It was in sweet spot for some time and gave good returns but at some point they were running at full capacity utilization and new capex was going to take years. Price had ran up quite a lot. I booked my profits after some days of writing following post. Bought it at about 200 and sold at about 500. Frenzy continued after that also like it happens many times in small caps and stock went up to 1000 not too long after sold out but no regrets since we have to make logical decisions and it’s perfectly fine to leave some profits on the table. Today it’s at about 350. This is one good quality small cap. Management is expert in this niche segment and quite an established player. I will be definitely be interested in investing in it again at some point.

- Black Rose

Again a niche player with decades of experience in trading and distribution that got my attention when they were commissioning new manufacturing plant. It looked very much probable that their entire new capacity will be fully utilized almost immediately. It was also an import substitution product. I booked profit when significant new capacity was expected from SNF.

-

Madhya Bharat Agro Ltd.

My first big multibagger It was a microcap so my position was small. But good run up in price made the needle move at portfolio level because it went up 7x very quickly and I booked profit at those level after which it doubled but again I have no regrets cause I would happily see it go up further than regret losing all gains. Many things can go south in microcap and such a run in short time should only be considered a pure draw of luck because I would have never predicted it. So count the blessings and book the profits. Small investor like myself have little to no visibility in such microcaps so it’s very hard to build conviction here.

It was a microcap so my position was small. But good run up in price made the needle move at portfolio level because it went up 7x very quickly and I booked profit at those level after which it doubled but again I have no regrets cause I would happily see it go up further than regret losing all gains. Many things can go south in microcap and such a run in short time should only be considered a pure draw of luck because I would have never predicted it. So count the blessings and book the profits. Small investor like myself have little to no visibility in such microcaps so it’s very hard to build conviction here. -

Nikhil Adhesives

Small player in adhesives marker with a brand called Mahacol. There was a good trigger for growth in 2 years period as company had entered into agreement with really large American paints company to manufacture for them. I love such situations where business is already secured and then an investment is made to execute it. Much simpler situation. On top of that their retail brand seemed to be gaining traction. Their products looked good. Famous CANSLIM investor Varun Daga and Charandeep Singh were invested which gave me confidence because their entire process is focused on new and good products that actually work in market. They don’t predict. They invest based on reported numbers. In terms of today’s price my entry was at about 10 and sold it off during pf churn when COVID hit to safe guard capital at about 20. It’s a regret for me because it went up 10x after that. During those days of uncertainty I reshuffled my pf to get out of risky investments like this in order to preserve capital. Sar salamat to paghadi hazar!

In hindsight, I should have kept monitoring the company and when COVID related risks were more clear I should have taken a call. But laziness got to me. If COVID like blue moon event happens again I would take same decision of selling such microcaps but I will not stop monitoring them! -

Modi Naturals

Similar story and result as Nikhil Adhesives. -

Poly Medicare

Great minds of VP had already done tremendous work and identified this company. This business went into long consolidation from 2013 to 2017. Their competition was making it difficult for them by litigation in various geographies. However by 2017/18 company had resolved most of the cases in their favor. I was lucky to stumble upon this company at the time and I allocated good portion. I sold off at about 1000 RS when they declared QIP. It was more than 3x for me so I booked profit but this is one business which I will always keep on my shopping list when there’s blood bath in markets for non company specific reasons. -

Sharda crop chem

Light weight business run by an expert. Sold off during pf churn of COVID. -

Sonata software

Same story as above. -

Suprajit engineering

Again this was well analyzed here on VP. I invested because their new capacity was being commissioned but Auto cycle did not revive. I realized my limitation as a retail investor trying to track an industry cycle like auto and sold off in favor of other simpler investments. -

Swaraj Engines

Same as above. Excellent management. Might be interesting at this time though. -

Vadilal industries

Being in USA I saw the products and their traction first hand. I loved the products. I loved the brand. What made me allocate a small position was the dispute between brothers who owned it. I didn’t want to get into such situation but other factors made me invest a very small amount and I am glad I did.

Mistakes:

I made fair share of mistakes in the beginning but thankfully my pf was small at the time.

- Tejas Network

I had to book loss of about 20% and as you can see above Tejas formed a huge part of my pf. I loved their products and IPs. It was one of very product based tech company with huge addressable market. I sold off when management kept making promises that were never achieved. Moreover, management used statistical magic to hide some dark areas. I was following the company from early on and I could see how management was trying to deceive retailers on their presentations and transcripts. I sold off when I realizer this. After that Tata group acquired it and Vijay Kedia happened but I don’t regret my decision.

Learning: It is better to invest in small caps based on reported numbers rather than anticipation of growth specially in frenzied sectors like Tejas’s.

Also, never rely on past 3 years numbers of a company that has just done an IPO. Every company starts window dressing with numbers and balance sheet at least 3 years prior to IPO. Those numbers aren’t real. And once they have your money, such company will invariably report subdued numbers because they have to adjust for the magic that they have done in last 3 years !

-

Sterlite Technologies

Again it was a top down kind of approach thinking that 5G will fire up the demand for optical fiber and it’s a structural change.

What I didn’t realize was that this is a commodity business and tons of new capacity was being commissioned.

I also made a mistake of taking peak cycle numbers and thinking that they will continue. -

KCP

Looked like a value buy with several possibilities that never realized like their new hotel business. Sugar and cement were obviously commodities. -

Edelweiss

Thankfully it was a tiny investment. I did it after watching a presentation on YT. I thought Mr shah was a genius.

Obvious mistake of betting on a person whom I know only superficially. And being an IT guy it’s very hard for me to analyze their business which is another mistake I made. It’s down 85% from my buying price but thankfully it wasn’t even 1% of my pf.

Overall, this forum has played significant role in my journey and I wanted to share my experience. And I also have a selfish motive of getting some counter views that can broaden my perspective.

I am re-evaluating my allocation in Pokarna as it can face risk of ADD considering how quickly US commerce department keeps changing their stances like a trader!