Our coverage of the midcap IT stories here at Valuepickr has missed Birlasoft, and I thought it’s time we keep a record of the investment thesis, and it’s development for posterity.

What’s the play?

Giant IT services companies like TCS and Infosys are the middlemen between customers that want to adopt modern solutions to cut costs, and pure tech companies such as Microsoft, Google, etc. that form their backbone.

We’ve seen the following trends in the last few years:

-

Having modern digital solutions to legacy problems are often an avenue to improve productivity and improve margins for companies. Covid has accelerated this spend, and will be a key driver of growth going forward.

-

Smaller IT companies have realised they can’t compete with giant incumbents and have healthy margins at the same time. The emerging solution seen across the pack is that they pick a few verticals and become the best solutions provider in their own niche.

Goal is to carve a niche in our verticals where we are better than the big players. We can’t solve every problem, but what we choose to solve, we can do much better than anyone else. - Dharmender Kapoor, interview with BQ, June 2021.

Okay, what are their verticals?

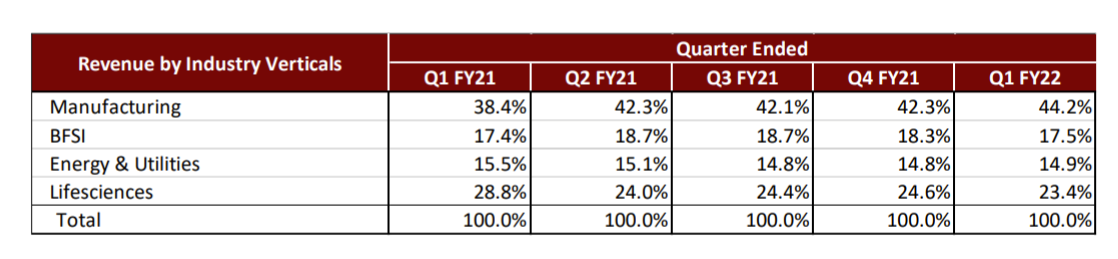

They have four main verticals. From the 2021 annual report:

Birlasoft helps customers in manufacturing to accelerate their Industry 4.0 adoption.

- BFSI - to leverage open APIs and automate both front-office and back-office transformation;

- Energy and Utilities - to enhance field collaboration and real-time service excellence, optimize operations and improve asset performance;

- Life Sciences - to automate drug discovery and pharmacovigilance processes.

Here’s how the revenue mix has changed over the years:

Why now? What has the journey been in the last few years?

The story becomes interesting after 2015, when Birlasoft brought in Anjan Lahiri, and he worked on the company until 2019 when two things happened. They merged with KPIT Technologies and became the digital enterprise company of today, and Anjan Lahiri stepped down due to urgent personal reasons.

After this, they revamped the board, with Mr. Dharmender Kapoor taking over as MD, and in the last two years have onboarded senior talent. Their current CFO has been on the IBM senior management for 20 years, and this trend has continued if one looks at their hiring on Linkedin.

How has their business model evolved?

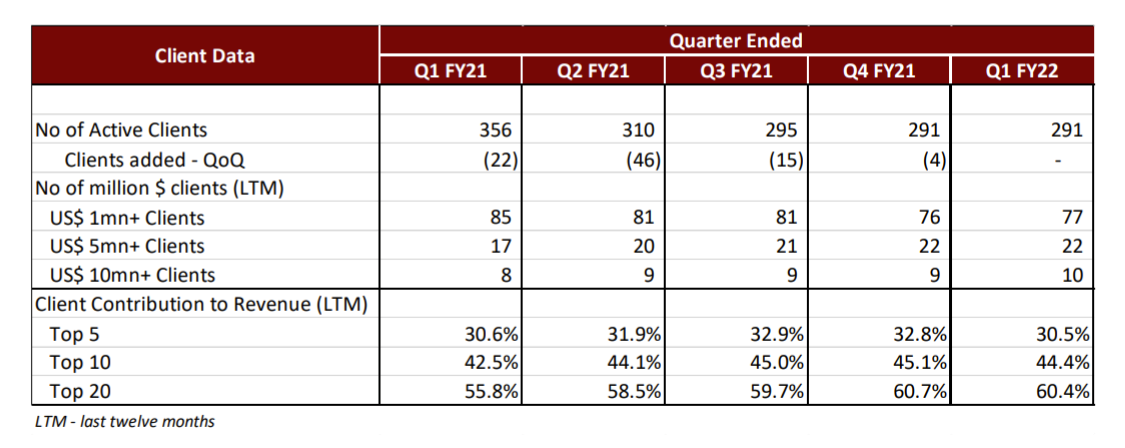

- They’ve started focusing on their top clients and have trimmed tail accounts. Furthermore, they’ve started selling more to their top clients across their verticals. This is seen through three data points in FY21:

- Lower $1 million deal wins, more $5 million deal wins.

- 97% of new deals are from existing clients.

- Increasing TCV trend in deal wins, FY21 was their best year.

- Annuity has improved from 60% in FY20 to 70% in FY21.

- Deals are now multi service rather than single service. New deals don’t necessarily fall into one vertical.

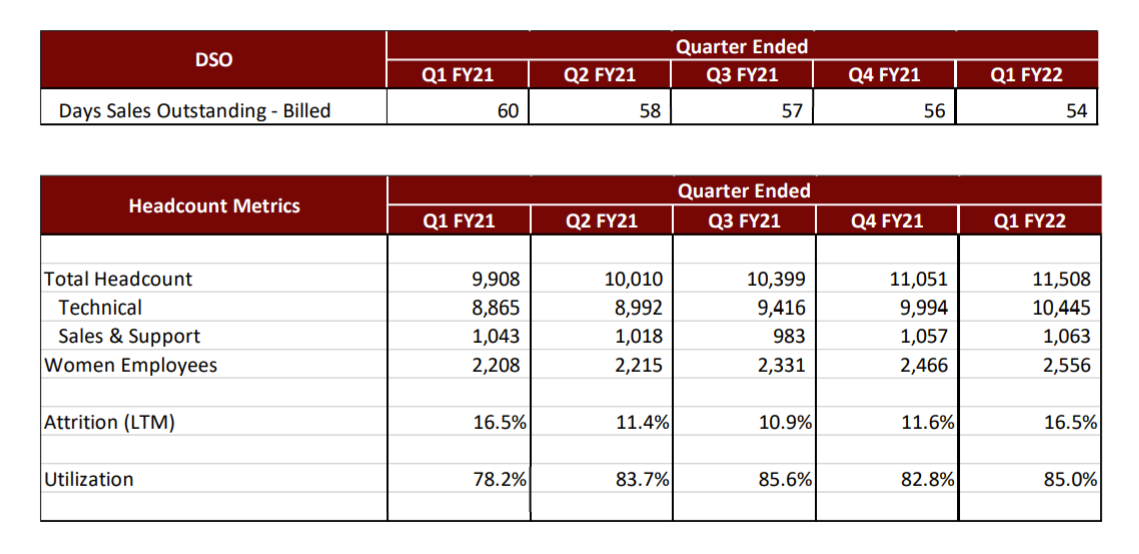

- They are constantly working on internal efficiency to improve operational metrics. The key metric management mentions repeatedly is the Days Sales Outstanding, and Utilisation rate:

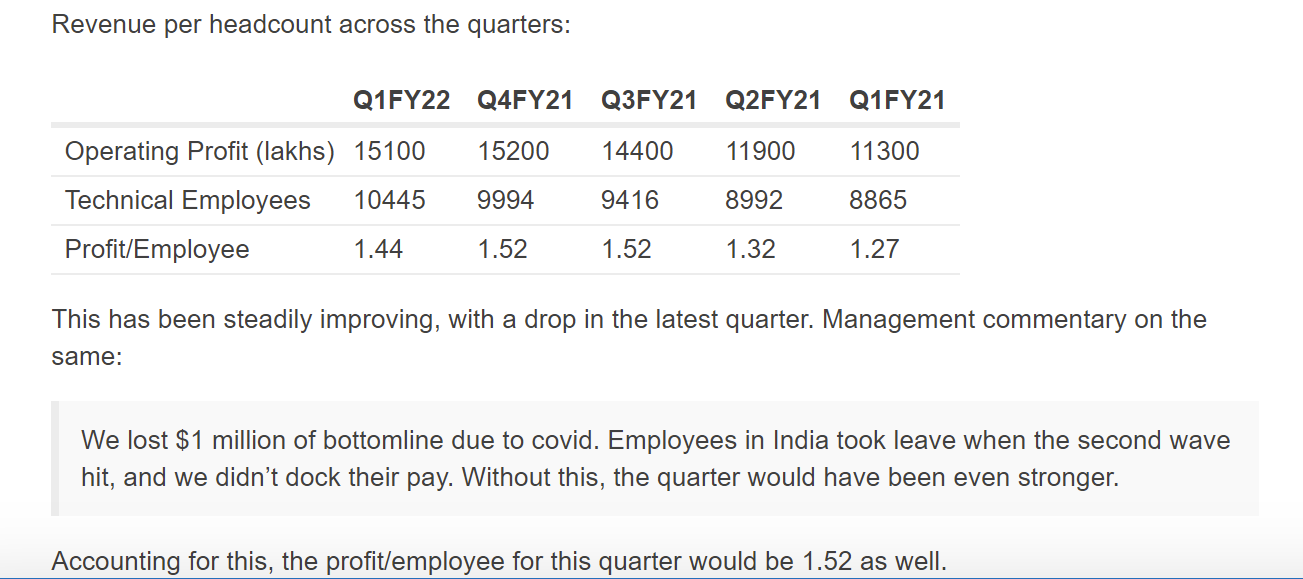

Revenue per headcount across the quarters:

| Q1FY22 | Q4FY21 | Q3FY21 | Q2FY21 | Q1FY21 | |

|---|---|---|---|---|---|

| Operating Profit (lakhs) | 15100 | 15200 | 14400 | 11900 | 11300 |

| Technical Employees | 10445 | 9994 | 9416 | 8992 | 8865 |

| Profit/Employee | 1.44 | 1.52 | 1.52 | 1.32 | 1.27 |

This has been steadily improving, with a drop in the latest quarter. Management commentary on the same:

We lost $1 million of bottomline due to covid. Employees in India took leave when the second wave hit, and we didn’t dock their pay. Without this, the quarter would have been even stronger.

Accounting for this, the profit/employee for this quarter would be 1.52 as well.

The last data point is important while considering the difference in wage costs between India and the US.

From the latest earnings call on the onshore/offshore mix (paraphrased):

We usually hire locals (onshore) if there is a crunch, as the hiring lead time is a lot quicker than in India where there is a 3 month lead time. When we hire offshore, we replace onshore subcontractors. Clients are also on the same page with starting projects on site and finishing it offshore. We improve our margins, they get comfortable with deal structure.

Okay, numbers are improving. Do they have ambition?

Paraphrasing what Mr. Kapoor said in June’s interview with BloombergQuint:

By 2025, we want to have 7500 Cr. of revenues (3500 Cr. today, implies ~18% CAGR). We will do this by:

- Growing top 30 accounts by > 20%;

- Platform strategy: partnership with Azure / AWS to offer solutions across the value chain;

- New channel for sales; good partnerships already in place.

Expecting profit CAGR to be much higher than revenue CAGR in the next 4 years. Profitability will grow. 3-4 quarters ago, this target of billion dollars was a dream. 2 quarters ago it became aspirational. Today, I’m far more optimistic and it’s looking like it can be a reality.

Absolutely no doubt that I and other top management will continue to work at Birlasoft until this goal is met. They’re motivated, excited, and handsomely incentivised to stay. We have our plans set in place for the next 3/4 years.

Financials and Cash Flows

- Are currently debt free and have 1100 Cr. of cash in hand.

Risks

-

The vision is entirely dependent on Mr. Kapoor and his close circle. If they leave in the next few years, big questions to ask.

-

Dependent on their partnerships with SAP, Microsoft, AWS. Currently a Microsoft gold partner, which gives them benefits to companies searching for solutions providers.

-

Execution - Reliant on better deal wins and client mining to meet their 7500Cr. target.

When we acquired KPIT, used to think 75 million dollar deal wins were a great target for a quarter. Today, 200 million dollars should be the average every quarter.

However, Q1FY22’s deal wins have fallen short of their own metrics.

- Their target of 1 billion dollars is a nice headline, but it implies a mid teen CAGR going forward. This is something we have heard from other midcap IT companies like FirstSource. Hence, is their target super normal?

Disclosure: Invested from lower levels, no recent transactions.

With current valuations, it’s becoming increasingly difficult to find low hanging value fruit. This post isn’t necessarily to offer a slam dunk investment opportunity, but to track a company here that may become more attractive/unattractive going forward.

Two amazing sources of information on the company:

From our very own board member:

Finally, to those with a BQ Blue membership, the BQ Edge series with White Oak is a lovely window into the smaller IT companies.

Will write further posts on management commentary, and takeaways from the earnings call.