Biocon Ltd. announced today that it has won a U.S. court ruling that invalidated a Sanofi patent on the Insulin Glargine device , removing a key legal hurdle to commercializing Semglee® (Insulin Glargine) co-developed with Mylan, in the U.S.

The U.S. District Court of New Jersey found the device patent claims (U.S. Patent No. 9,526,844) asserted by Sanofi against Biocon and Mylan’s Insulin Glargine product ‘not infringed’ and ‘invalid’ for lack of written description. Separately, as previously announced, Sanofi’s formulation patents (U.S. Patent No. 7,476,652 and U.S. Patent No. 7,713,930) were previously affirmed to be invalid by the Federal Circuit.

The 505(b)(2) New Drug Application (NDA) for Semglee is under active review by the U.S. Food and Drug Administration (FDA). The FDA has set a Target Action Date for our Insulin Glargine application in June 2020. Biocon remains confident of being able to commercialize the product in calendar year 2020. The market opportunity for Insulin Glargine in the U.S. is estimated at US$ 2.2 billion.

I think this significant positive development

Even if there is price erosion this is significant opportunity for Biocon as insulin is almost used lifetime for diabetics patients

Biocon has escaped the meltdown, at least for now, why…my thoughts below

Biologics - not reliant on APIs!! Demand will be lower as non-urgent cancer treatments are postponed due to covid-19, but will quickly ramp up as the situation normalises.

Biocon is the number 1 manufacturer of many APIs (statins and small molecules in particular), so unaffected by the Chinese shutdown recently

Debt is highish, but manageable - this is probably the only negative for biocon

Biocon share price hitting all time highs! Good news flows also helping the share price (EIR from FDA)…

I personally think that 4th quarter 2020 (vs 4th quarter 2019) will be weaker due to covid - due to postponement of cancer treatments (trastuzumab) including supportive therapy (peg filgrastim). Also, statin use will be much lower as well since non-urgent doctor visits have reduced significantly and this results in delayed renewal of repeat statin prescriptions…thinking out loud

Additionally - @stockcollector you raise a good point, I am not sure myself how to think about the pandemic’s impact, although I’m a little more optimistic (and biased, ) but I guess we’d get to know definitively later this week on the earnings call

Additional Municipal Commissioner Suresh Kakani said Biocon will now provide the drug to all BMC hospitals treating critical care patients. “KEM will be the principal hospital that will oversee the drug’s use.

Good opportunity for poor patients and Biocon for clinical trials of Itolizumab on covid 19

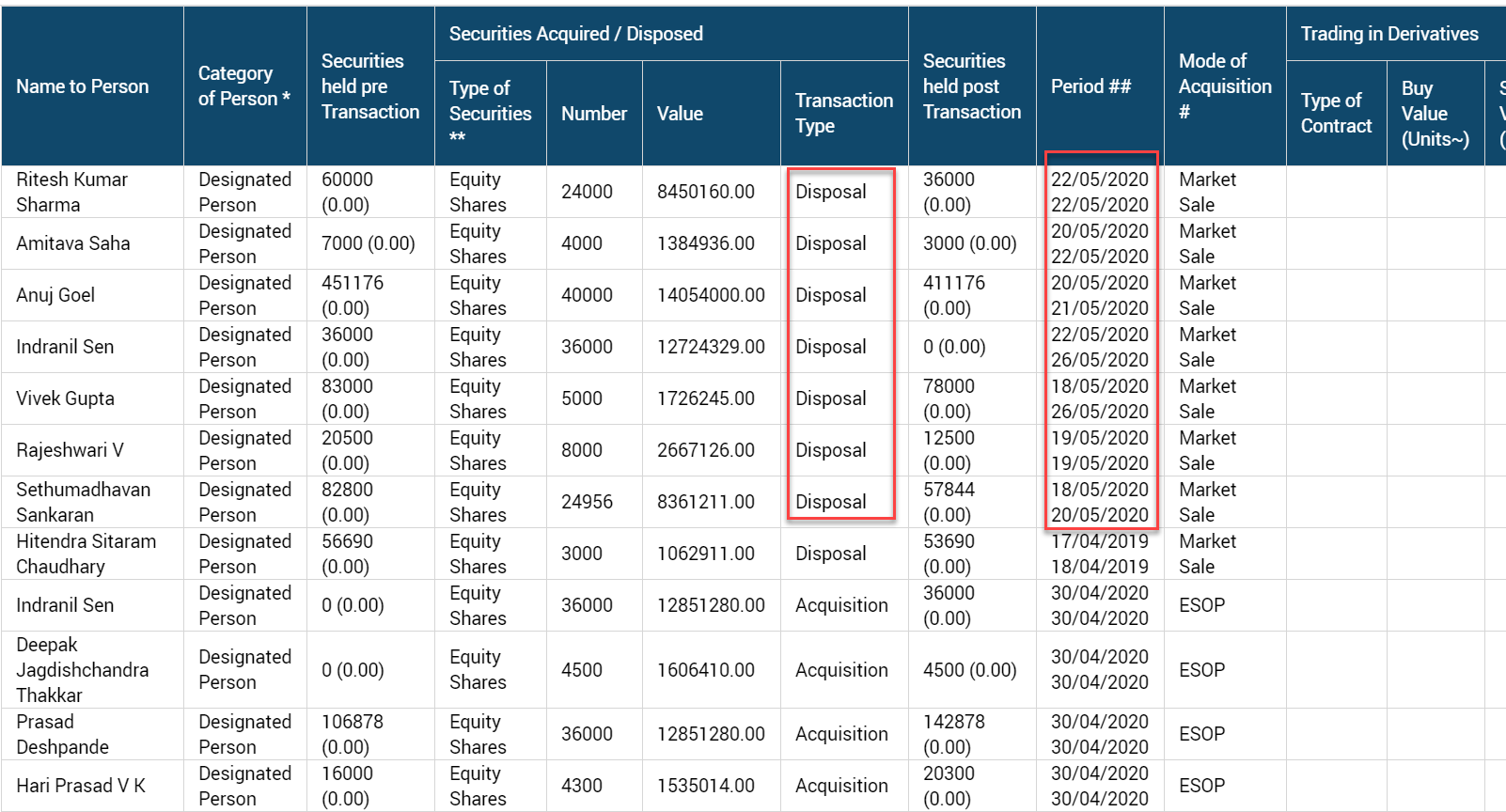

So many of the ‘Designated Person’ have sold their holdings in this month alone. Why would these varying and designated people sell out in same months and in such close days? Are they aware of things not going too well in company?

It is not a cheap stock so people who got stock options will sell stock and diversify into something else. Major investments and job is same company is very high risk concentration.

Biocon Ltd. (BSE code: 532523, NSE: BIOCON) today announced that the U.S. Patent and Trademark Appeal Board (PTAB) has ruled in favour of Mylan, Biocon’s* partner in inter partes review (IPR) proceedings finding all challenged claims of Sanofi’s Lantus® SoloSTAR® device patents, U.S. Patent Nos. 8,603,044, 8,992,486, and 9,526,844 unpatentable. The PTAB found three claims of the 9,604,008 patent unpatentable, and two claims to be patentable. However, Mylan and Biocon have previously obtained a covenant not to sue from Sanofi on the ‘008 patent and therefore this ruling does not impact Biocon and Mylan’s ability to commercialize Semglee® (Insulin Glargine) upon final approval from the U.S. Food and Drug Administration. The PTAB also found Sanofi’s proposed amended claims for the ‘486 and ‘844 patents unpatentable.

Some companies when offering ESOPs mention a couple of dates as vest date for everyone. If Biocon follows such approach, there is a good chance for most of them to sell (at least to cover IT) around same period. Also the stock at all time high, ESOPs would have doubled since the offer rollout so it makes sense for them to liquidate.

Updates on Insulin Glargine (Semglee/Lantus) (Market size: $6.4bn)-

Target action date: mid-June 2020

Launch: Second half of 2020 if it gets approval

Patent held by Sanofi was proven to be invalid on 01-06-2020

Competition: Only one other biosimilar from Lilly.

Will get to know about interchangeability status at time of approval (i.e. a patient who were recommended Insulin Glargine can go with Mylan’s biosimilar).

Refer this - https://www.investors.com/research/ibd-stock-of-the-day/biotech-company-rattles-amgen-mylan-biosimilar/

As per the above website in the quarter Sep 19, Coherus which got an approval for Pegfilgrastim after Mylan/Biocon had a 18% share compared to 6% of Mylan/Biocon. This was primarily because Biocon was suffering from capacity issues. This aside, I tried to understand the price fall due to arrival of new players by looking at the revenue of coherus who’s only product was pegfilgrastim. For a 18% market share Coherus made 111 million USD and 45% PBT margins on a 3.6 billion dollar product. If I assume this to be the standard and that biocon will get all its biosimilars approved (60 billion of sales), then the potential profit from these will be 111*72 / 3.6 * 60 = 5700 INR crores of PAT on 12600 INR crores of revenue which is around 47 EPS. Now Mylan needs to be paid too - if I assume 15-35% on sale price, the incremental potential EPS falls in the range 10 to 31 per share.

The key therefore is for Biocon to get all its approval right. One mis-step and the current price could no longer be justified.

Your numbers do not add up, if market size of Pegfilgrastim is $3.6 bn and revenues for a 18% market share are $111 mn, it implies a price erosion of 83%. You don’t get a price erosion of 83% in generics in their first few years with 5-10 players, how can you get a price erosion on biosimilars with 3 players in the market?

Udenyca (Coherus biosimilar) is priced at 33%-40% discount. Also, EBITDA for 2019 is USD 111 mn on a revenue of USD 356 mn. At Neulasta (the reference drug) pricing, that works out to USD 540 - 600 million of pre-discount sales value ~ 18 percent of USD 3.6 billion. Comparitively, Fulphilia (Mylan/Biocon) has market share of 6 percent, down from a peak of 10 percent last year.

Frankly, its quite an embarrassment for Mylan that a one product company has outsold their biosimilar even launching after them. And now Sandoz has launched too with Pfizer, Amneus, Fresenius Kabi also to enter. Need a major turnaround to prevent pegfilgrastim market from slipping away.

From Coherus 10-K:

"Sales and Marketing

Our strategy is to retain or acquire commercial rights to biosimilar products in the United States.

The sales call points to oncologists in the United States are highly concentrated and addressable by our relatively small commercial organization. Similarly, for our ophthalmology franchise products, we anticipate that the number of accounts to drive 90% of sales volume is approximately four- to five-fold smaller than that for the oncology support of care market. As a result, we anticipate a relatively small incremental investment in additional sales force will be needed to address the ophthalmology marketplace."

From this it would seem that Mylan’s scale is not much of an advantage in selling biosimilars - unless there is interchangeability. In fact, the caliber of reps needed to engage with the sort of KOLs who drive volume in biosimilars may only be with the innovators and niche cos like Coherus.

So with 2 players in the market, the price erosion is close to 45%. Its a good data point to have. Thanks @shivramrca and @vivek423 for pointing it out.