I have been tracking biosimilar developments in US for the last 2-3 years and can share my observations. In the beginning when there was no clear cut pathway for biosimilar marketing, selling a new biosimilar molecule was almost equivalent to a speciality generic molecule, where companies required doctors to directly prescribe their version of biosimilar. This was in stark contrast to marketing generics where interchangeability happens at pharmacy level, which means that gaining market share is relatively easy. With the recent interchangeability of insulin glargine, this might change and biosimilars are likely to go down the generic route, where gaining market share is directly a function of price and relationship with a PBM.

Now coming to Biocon, there has always been a lot promise due to their large pipeline and early mover advantage. However, they have almost made no usage of early mover advantage. In the beginning, Biocon struggled against the likes of amgen which had a better doctor connect. Then they have struggled in terms of pricing where competitors (including Amgen which is an innovator) have underpriced them. Lets look at it through market share of individual molecules.

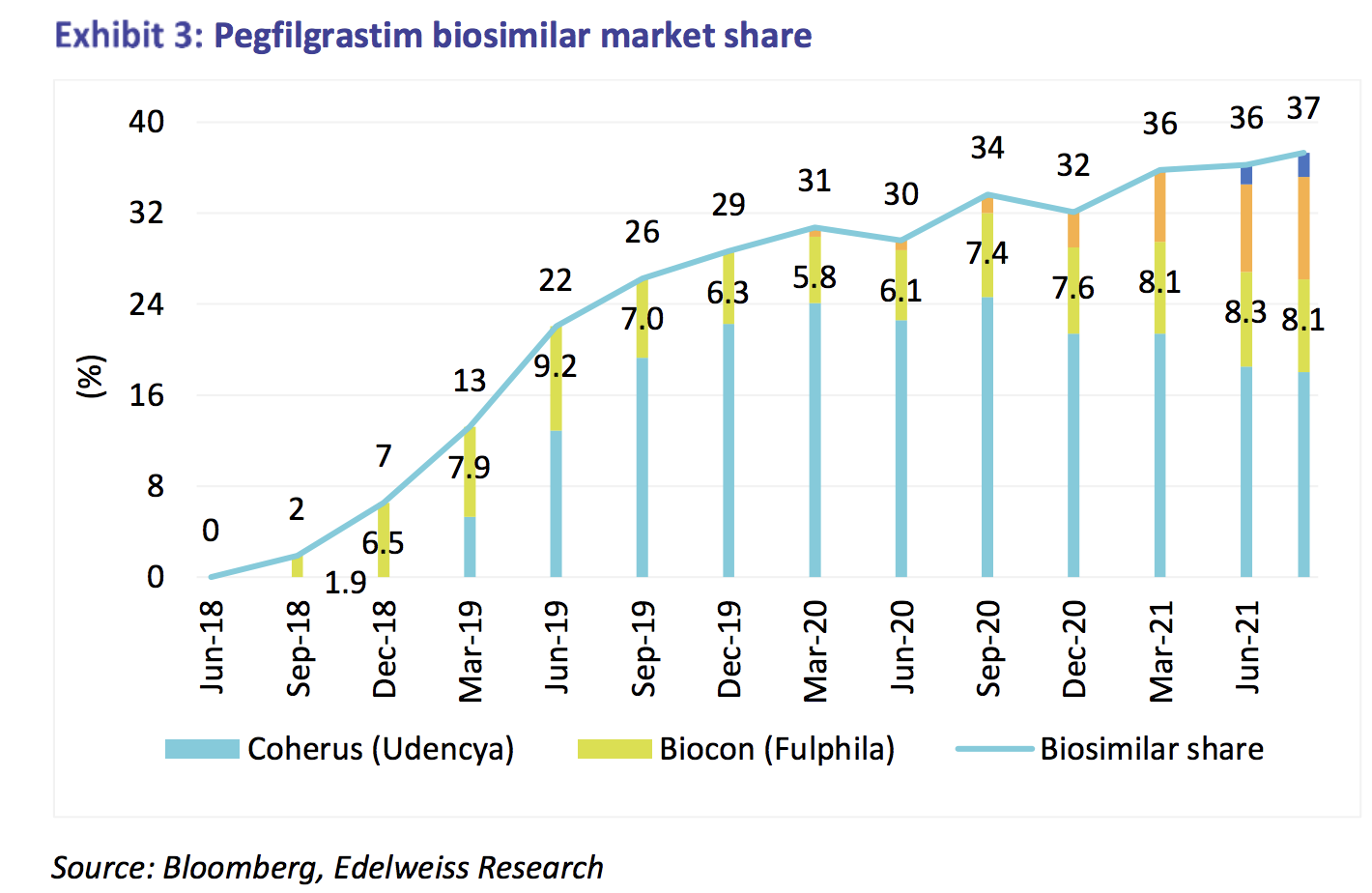

Pegfilgrastim: Biocon got to 9% market share in June 2019 and since has been struggling. This is despite the fact that biosimilar market share has increased from 22% in June 2019 to 37% in June 2021. Over this time time period, all the gains have been made by newer players and Coherus.

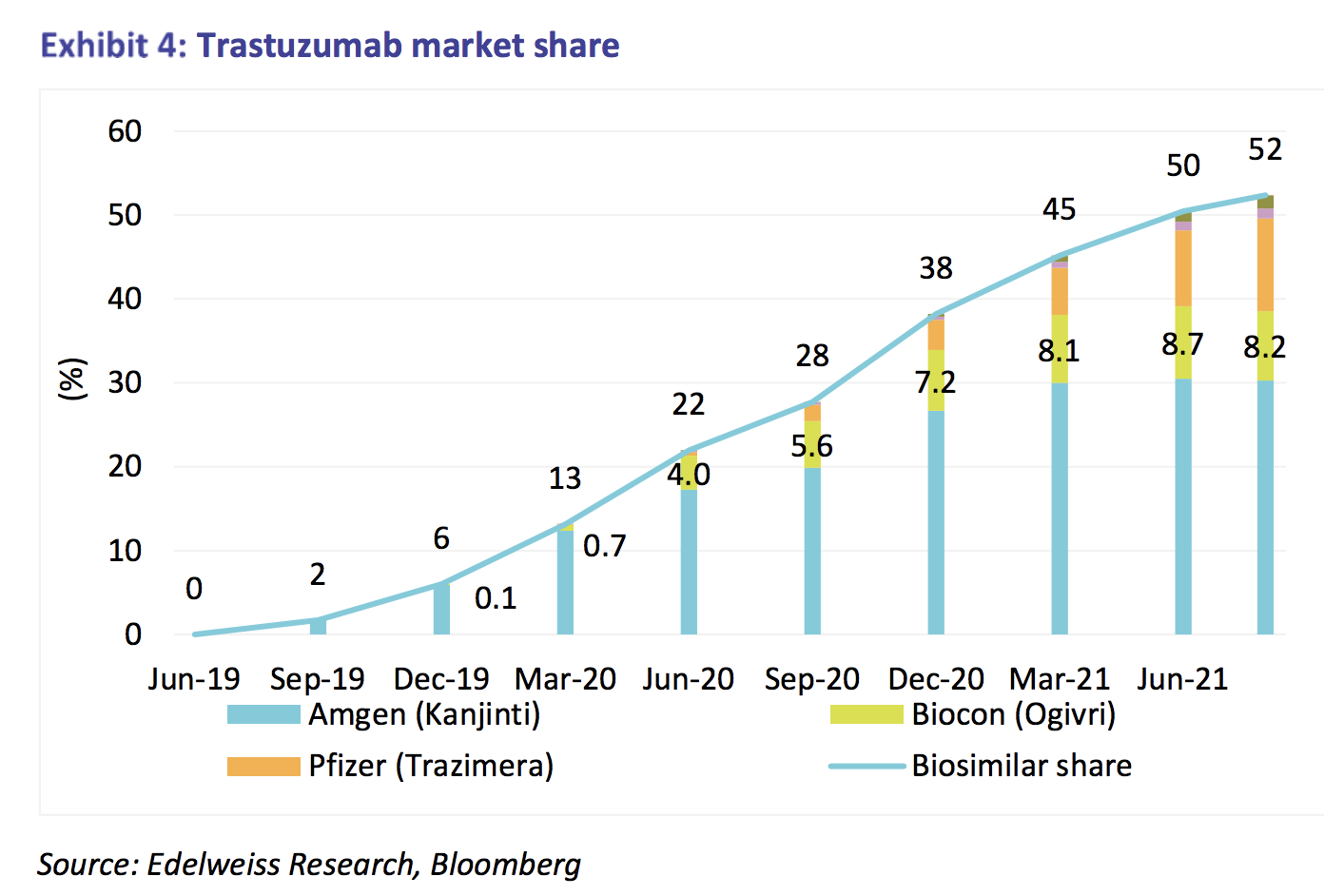

Trastuzumab: Biocon got to 8% market share in a few month and has since been struggling. Amgen has been fiercely competitive and gained market share. The total biosimilar adoption has increased to 52% here.

Glargine: Biocon currently has 3% market share even after >1 year of launch. Their market share should increase as they have supplied and booked large revenues this quarter. However, given their past track record, I don’t know if they can get to a 20-25% kind of market share. Getting to a 20-25% market share is important to have optimum utilization of manufacturing capacity, also this kind of market share leads to better pricing with PBMs.

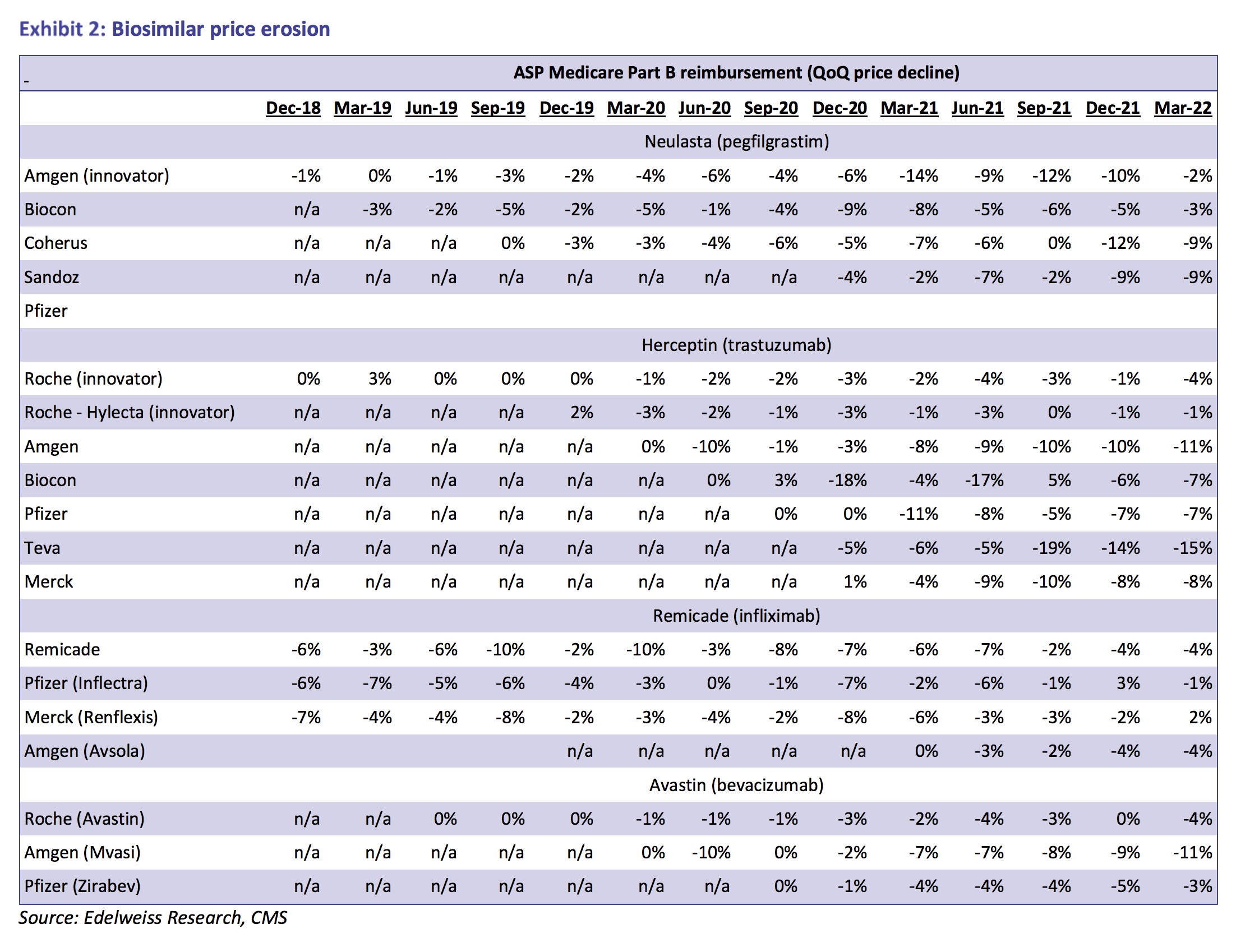

Pricing pressure trends: Biosimilar market has been a bit unusual in terms of pricing pressure where even when there is no new player, incumbants go for price cuts every quarter. The kind of pricing pressure seen in biosimilar in 3-6% on Q-o-Q basis which is even worse than generics. My own thought process is innovators want to capture the biosimilar market as they have been unable to bring new molecules in market, so they cannot simply let the biosimilar market go to manufacturers that operate out of a cheaper geography.

What I have struggled to grapple with is why Biocon is not more aggressive on pricing. Even in India, Biocon has struggled to gain market share against Cadila. I think they lack seriously in their marketing capabilities. Also, I don’t understand as to how taking over the marketing unit of Viatris leads to more synergy as this is the same marketing unit that couldn’t get double digit market share in trastuzumab and pegfilgrastim after 3-years of launch. Also the price paid is quite significant for a simple marketing entity (4x EV/sales vs 1-2x EV/sales paid by other generic companies recently).

All this said, I think strategically it might make sense for Biocon as they have bet almost everything on biosimilars. Its going to be a binary outcome for them as balance sheet will be very stretched now.

All the graphs are taken from an Edelweiss report, its a must read to get a good understanding of pricing pressure in US biosimilar market.

https://www.edelweissresearch.com/Research/Download/13828