Biocon has been a underdog for quite some time now, to a point where pretty much folks have given up on them barring contra and high conviction folks with super long term views - silent thread is a good measure

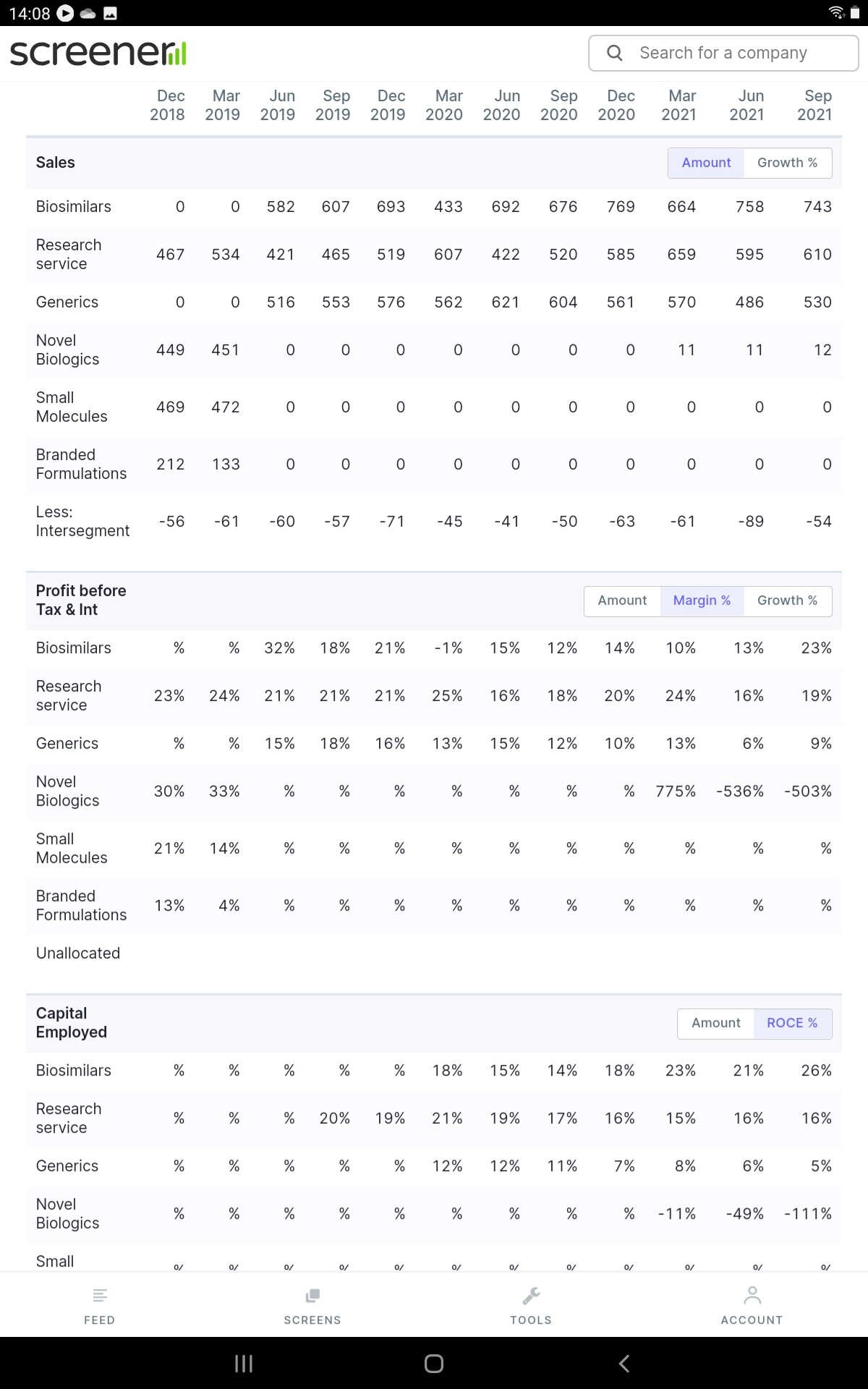

Here is a 12 Qtr view

Some valuation takeaways and Q2 call highlights

- Though PE is not a right metric as they have E under pressure being in perpetual Capex phase, even after that they are below long term median PE range

- with Market cap of 40K cr, available at 5X sales and less than 23X EBDITA- that’s for a global scale Biotech and CRAMS player.

BelowTriggers for turn around in performance ( ignored by mkt for now)

- Biosimilar performance and margins improvement visible with back to back margins improvement - per call Geo mix helping with mkt share gains/steady

- Multiple Biosimilar positive trigers - post above by @stockcollector

- Syngene performance going steady- although hammered by mkt along with Biocon

- Generics can’t get any bad - cycle on pricing pressure to turn around next year as regular cyclical aspect and RM pressure to ease as well as covid stocking etc to normalize

- SII vaccine partnership, Adagio partnership appear to be smart win win proposition

- Good investors with successive raise in valuations for biologics

Monthly chart showing a lower channel bounce back, yet to see volume picking up

Invested , Re-entered recently