leaving the question of rates aside for the time being, the price per sqft of shops/showrooms is always higher than offices and the price of offices is always higher than residential apartments. So it stands to reason that whatever is the price of residential apartments (you can take whichever number you feel comfortable with), the prices of offices and shops is always going to be higher - hence the overall price realization for the project as a whole is going to be substantially more than the going price per sqft for residential apartments ( which if the 99 acres report is to be believed in Perambur is Rs 5792 psf )

Secondly, this is the first large scale development in North Chennai. There was a severe paucity of land here and there was simply no space anywhere left to build. Perhaps that is the reason why majority of the construction is happening elsewhere in Chennai

The primary purpose of the development is to decongest the dense, populated marketplace and uplift the standard of living in North Chennai.

Thirdly, and this is important - North Chennai is primarily a marketplace - and the demand for project is going to come from those wishing to shift from their small & tiny shops & showrooms to a bigger commercial place with better amenities. With that, they would probably want to shift their residences as well.

I will post details about my interaction with Codename City and try and understand how much has been sold.

70 lac sq ft (FSI) times Rs. 6000/sq ft is 4200 crores. This would mean Binny’s share is 1600 crores. I think there is some double counting somewhere in the calculation fo 3300 crores

I am taking the price realization psf around 11000 and not 6000. I think the project will do that much. But this is my opinion and should be taken cautiously as I have invested a large portion of my portfolio in it and views are biased towards the positive side. I am exceedingly bullish and also prone to making mistakes just like other investors.

Hi Bheeshma nice write up , thanks for sharing your research.

The stock does seem undervalued. price of 63 acres land (basis similar related party transactions as per AR) should be approx 63 x 20 = 1300 cr approx. The stock is quoting at 300 cr and is at good discount to book value. The company has purchased a parcel of land from RP Mohan Distilleries at Perumbar road @ 20cr / acre.

The stock may give good returns due to narrowing of the discount.

however, below are my concerns

First phase is 23 acres. I am not an expert but total built area as per your post of abt 70 lac sq ft .IS IT SAME AS SALEABLE AREA or does it include common areas like roads, parking, terrace, alleyways, etc.

Also 11000 rs sqft price for Chennai is too high. Commercial rates are higher but i believe that the cost and time for approval is also high. Otherwise most of the builders will be interested only in commercial property . The cost of construction is same. So why not sell a commercial space @12000 rs per sqft rather at 6000 rs sqft.

The place where i live is 18 acres project and roughly 600 flats. So @ 6000 rs sq ft , each flat will cost abt 1.2 crore, so total revenue of 720 crores. The buildings are 10-12 floors each. Don’t know about FSI of the project. Assuming that buildings in this case of Binny are higher and common areas are less so more flats, even if I assume 900 flats and a rate of 1.5 cr per flat gives me about 1350 cr for 18 acre and abt 5000 cr for 64 acres. 8300 cr looks higher but may be achievable due to commercial segment but i believe the costs incurred by builder will be higher. This is my assumption.

The promoter quality is not good.

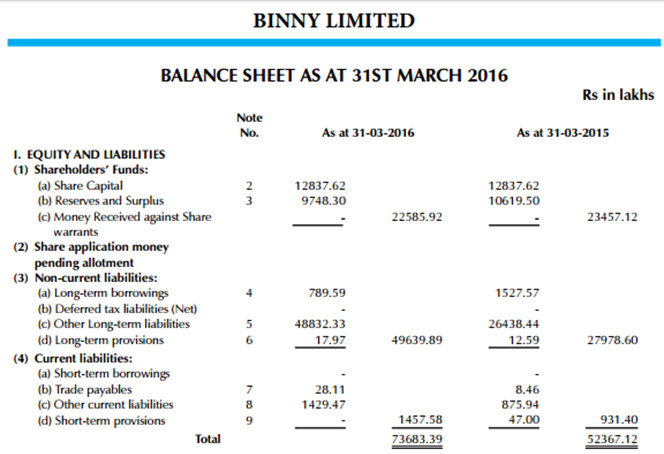

WARRANTS : Money worth 225 cr received against warrants. This is HUGE w.r.t to the market cap of company and may lead to huge dilution.

Do you know the beneficiary of the warrants, at what price alloted and if this 225 cr is 25% of the total paid or if it is 100% paid.

the promoters received about 450 cr from JDA partner plus sale of land in past. Why didn’t they use the amount to retire the Cumulative preference shares. Instead they used the amount to buy land from Related Party Mohan Distilleries. So, the money is gone, there is no cash, no current investments.

they have changed the terms of Cumulative prefernce shares to RP (Mohan Distilleries) from 9-9.75% to NCD of 18% in Sept 2014 and awaiting Court approval. CONTINGENT LIABILITES - If they get court approval they have to pay about 140 cr to RP as interest due. If they don’t get approval they pay about 100 cr as interest. So the RP is getting a benefit of 40 cr over a period of 1.5 years just by changing the terms.

The share of revenue with JDA partner SPR - 40 : 60. I assume the fig is correct as I did not find it in AR. What are the terms of agreement. Does Binny has to bear a percentage of costs ( cost of approvals etc) ?.

In present scenario with ROE of real estate developers in single digits and NP margins of about less than 10%, lets assume since the land is free, that the builder SPR makes a NP margin of 40%. So on a sale of about 8000 crores he will make a profit of 3200 crores. In such case how can the builder give 40% i.e the entire profit to BINNY. There can be an error in my calculations but still it seems high.

there is an income tax demand of 114 cr pending litigation.

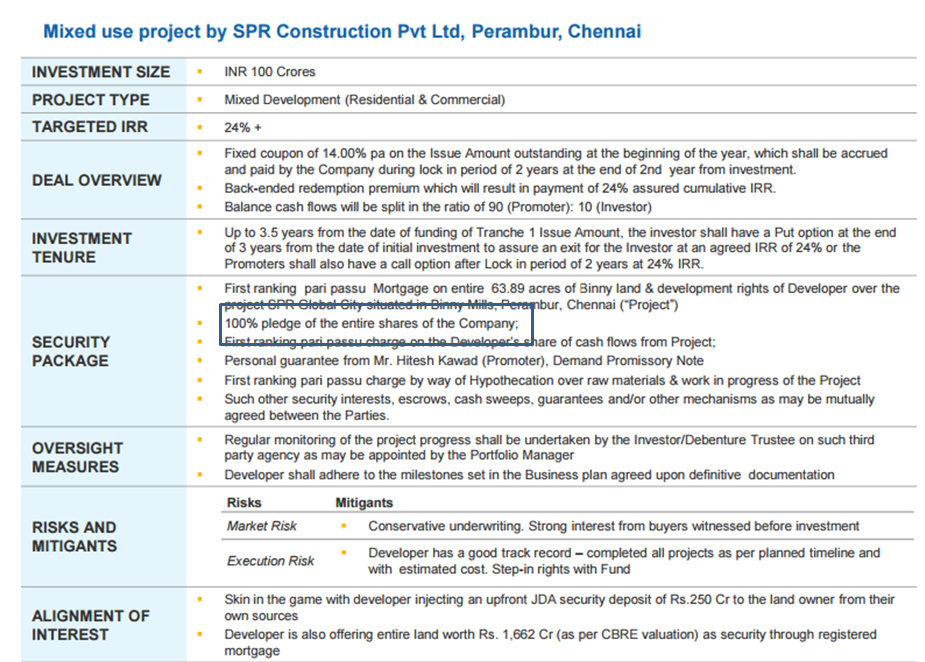

also giving 24% IRR to Piramal capital seems very high. anything above 18% is very high.

I decided to do some scuttle on this project. They have prelaunched the residential component of it called codename city. I will post the details as soon as i compile it. But i can tell you right away that it has done well.

I dont think the company has received money against share warrants

[quote=“manishinlucknow, post:24, topic:9392”]

the promoters received about 450 cr from JDA partner plus sale of land in past. Why didn’t they use the amount to retire the Cumulative preference shares. Instead they used the amount to buy land from Related Party Mohan Distilleries. So, the money is gone, there is no cash, no current investments.

they have changed the terms of Cumulative prefernce shares to RP (Mohan Distilleries) from 9-9.75% to NCD of 18% in Sept 2014 and awaiting Court approval. CONTINGENT LIABILITES - If they get court approval they have to pay about 140 cr to RP as interest due. If they don’t get approval they pay about 100 cr as interest. So the RP is getting a benefit of 40 cr over a period of 1.5 years just by changing the terms.

[/quote]

Mr Nandagopal is also the owner of Mohan Distilleries. a few years back (2014) the board approved a merger plan with Mohan Distilleries but that did not happen because of some complicated state excise rules

The idea was to merge the land bank of Mohan Distilleries with Binny Ltd for its real estate plans. Since then it has issued Cumulative Preference shares which will be converted into NCDs. In effect it is an ongoing payment for acquiring the landbank for Mohan Distilleries. The current CRPS quantum is 117cr

in a typical JDA the developer ( SPR ) bears the cost of construction from its share ( which in this case is 60%) and the land owner ( Binny ) bears the cost of the land from its share ( 40%). On a sale of 8000 crores Binny share is 3200 crores which will be paid to it periodically over time as registrations happen. The cost of land for binny is negligible as it is legacy land. Almost all of the 3200cr is pure cash receipts. The building approvals etc is all the headache of the builder. Thats why JDA are attractive for the landowner

That is all SPR’s headache. As long as Binny receives its share how SPR wants to finance the construction is their lookout. I have no specific views on whether its high or low but i do know that 20%+ is the standard interest rate for financing construction activities

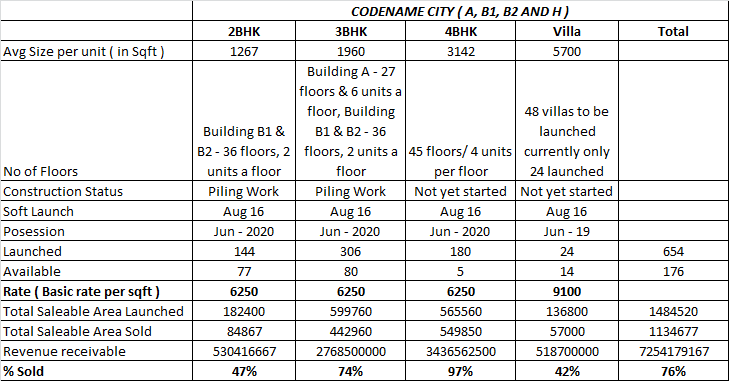

Based on my scuttle - Codename city - the residental component of the larger project has been soft launched in Aug 16 with 654 units. It has sold 76% of all its units. This is the situation as on today

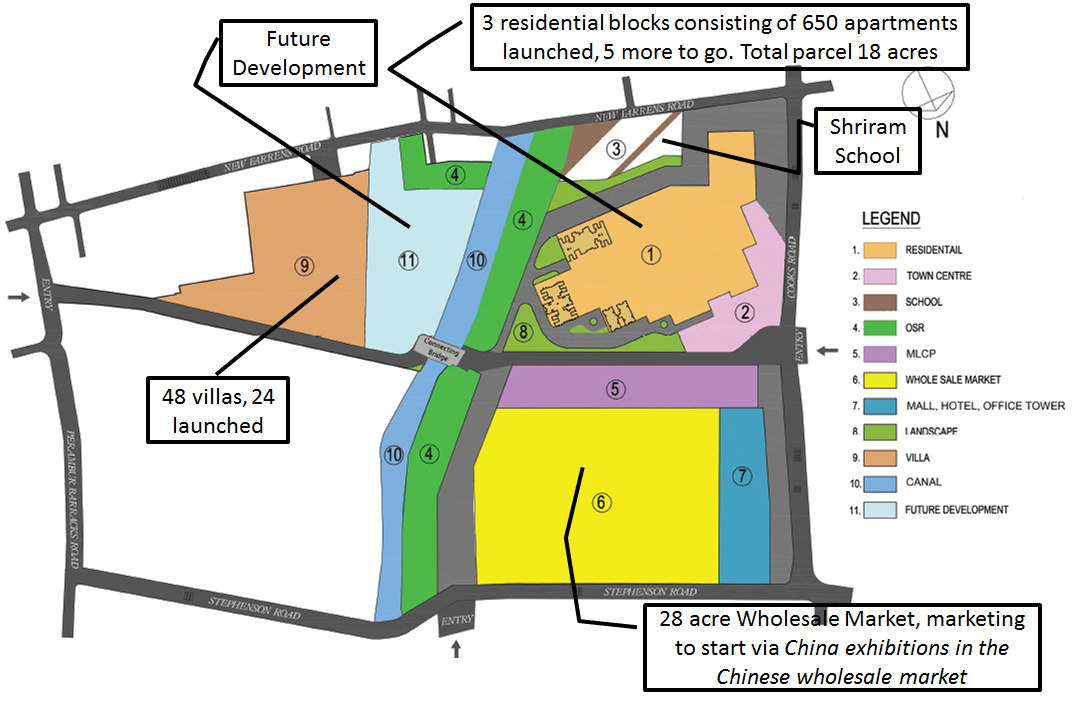

This indicates the robust demand for the project. The basic rate is Rs 6250/psf and most of the demand is for the 3 & 4 BHK’s - as you can see from the sheet. 2 BHK’s have not done as well as their larger counterparts. The entire residential component is on an 18 acre parcel of land. This is just a small start.

Another risk and thanks to @shaunakmisra for highlighting it is the high pledged % of the promoter. Truth be told the pledge is puzzling and needs to be investigated further. I would love to hear views on why the pledge

Nice work @bheeshma .

Out of the 725 cr. receivable, Binny’s share should be 290 cr. spread over 12 quarters, which comes to roughly 24 cr. income every quarter (96 cr a year) plus any additional bookings income on the remaining area.

Promoter’s privately owned Mohan breweries plant is located in Valasaravakkam chennai. This plant is being relocated to kanchipuram, to help unlock the real estate value of the land in valasaravakkam. Could the pledge be to fund this relocation?

(note that the merger plan discussed in the article was subsequently dropped as already mentioned here by @bheeshma )

The pledge is because of the security package embedded in the terms of loan between SPR and Piramal Capital. In fact we can expect the promoter pledging to increase to 100% as collateral for this project

From my scuttle, they will market the wholesale market concept in China by participating in a series of chinese exhibitions. They have roped in 50 channel partners to market this project. It seems a large quantity of Indians come to these large chinese exhibitions from all over the world & chinese traders also want to expand in india through their indian representatives.

In real estate location,product mix, pricing and community play an important role. I think all these 4 account 95% of the sucess of the project.

I think the location is outstanding and will do a world of good to the North Chennai infrastructural woes.

Product mix they will slowly discover. I personally feel they should have a larger sized apartments - which if you look at the scuttle i have done are the fastest moving product category

Pricing - i think they have priced their apartments on the higher side but given that the there are a lot of larger sized apartments its ok. The main thing is the commercial area when it comes up. That is going to be a serious game changer.

Community - I like the fact that the community targeted is not the IT/ITES group. Their salary increments are not going to be high at least for the next few years. Its the business-people that are the main target group and they are cash rich and home poor. Plus the family sizes are bigger in that community and they require more space. And they all buy in herds - if one buys the other follows - it is literally a competition and it is this particular tendency of the trader community that has made me very positive about the prospects.

I think all 4 triggers are in reasonably in place. Only time will tell now if my “thesis” is in the right direction

I am guessing they will be sold outright. Since this is a JDA, having rented spaces leads to complications and potential disagreements between partners. SPR can also buy out Binnys share and then they would own the entire project and can do whatever they think will make good business sense

“The company has entered in to ‘Joint Development Agreement’ (JDA) for development of land

in to a Township. As per JDA the company has received Rs. 24400.00 lakhs, as interest free

Security Deposit and a sum of Rs. 25.37 lakhs has been received from JDA escrow account

which are shown under ‘Other Long-term liabilities’.”

It appears that this amount is refundable back to SPR.

if we agree that the project is worth somewhere around 5,000cr (given current sale prices), a max of 2,000cr will accrue to Binny over 7-9yrs? the present value of that is maybe 1,000cr (i’m assuming a high discount rate)?

Binny’s liabilities today include: 244cr repayable to SPR, 117cr of redeemable shares, 96cr of accrued interest on these preference shares, future 70cr of payments on these shares (10cr/yr for 7 years), 20cr of debt on books, and potential contingent liabilities of approx. 150cr (we can debate how much of this will be payable). The sum total is 697cr

so we are left with 300cr of accrual to equity shareholders, before taxes. that’s 200cr after tax. with a market cap of 304cr, where is the value?

note: i have left out any discount most people would apply to a promoter group that has behaved the way Binny & co. have in the past

please criticize my argument, i’m trying to understand where i’m wrong

I am of the view that the project will do sales in the region of 8000 Cr. The final revenue figure we will know only as the project progresses and we get some additional information on the numbers. I dont know how you have calculated the present value of 1000 crores, since the land itself is worth 1662 crores (CBRE numbers in the piramal document).

While the 244 cr deposit is classifiable as refundable - it is income received in advance - hence shown as a liability. The preference shares convertible to NCD’s and all the interest accrued on it is liable to be paid to Mohan Breweries. As already outlined Mohan Breweries is owned by the director who wanted to merge its operations with binny but couldnt because of excise complications. The idea was to access the land bank of mohan breweries. Since then, they have issued preference shares to mohan breweries which are convertible to NCD’s @18% pending shareholder approval. The reason why that move is done is simple & effective - Interest payable is deductible from income which reduces income tax. It is a more efficient form of payment for the landbank of Mohan Breweries. In return they are getting land which will again be used for a JDA.

I am not sure what you are referring to. If anything all the moves of Binny Ltd management is to enhance shareholder value.

[quote=“manishinlucknow, post:24, topic:9392”]

[quote=“manishinlucknow, post:24, topic:9392”]