It’s great to see spirited arguments from both sides. This is exactly what is needed to enliven discussions back, at VP.

We are passionate folks, so we do lose our cool sometimes, jibes at each other happens occasionally. At the same time, we must be able to retain objectivity, especially appreciate the roles we are playing.

Part of willingly playing a role is the pre-knowledge that some roles are tough to play - it requires a little bit of thick skin . At the same time as pointed out very succinctly, others in Team VP must appreciate that it’s a “role” being played. And for good effect. To polish our own output, maybe maybe alert us to some shortcomings, point us to some parts of the puzzle our attention could be little lax due to over-familiarity, over-attachment?

Having said that we acknowledge - this is something that is new to VP - as we get used to more organised attacks, we have to get better at defence, avoid personal comments, NOT shoot the messenger, and defend civilly.

I am sure things will settle down better as we go on and conduct 5-6 more such intense exercises. VP Culture has never been about one-upmanship (but does happen once in a while among passionate folks - those who know us closely know - what kind of big fights Ayush, Hitesh, Donald can also have - as recent as Feb 2020 in Gujarat). We are quick to acknowledge our mistakes, shake hands and share hugs - smiles back.

This should happen in this BR thread too. Great friendships are forged from the respect that develops from even adversarial positions - once we better understand the intent - and the role played.

Thank you Ashwini and Ankit both for understanding this and handling this with maturity. Please reach out to each other.

We VP Seniors are watching with interest. Will intervene when necessary- don’t think we will need to too often. Please keep up the good work!

Apologies, if my language was a bit harsh. I have edited some part of my reply as well. Sometimes, when you are following a company for long, you do get emotionally attached with it and get carried away! I do agree with many points you have highlighted in your post and people investing in the company should be aware of these issues as well.

I do understand that you are doing a tough and thankless job of forensics and people who are invested in a company will get offended by it. Keep up the good work.

Ashwini

If you remember your first post on cash flow, you said there are problems with cash flow without explaining what those are.

Maybe there were but I think they were not explained properly.

Most then have 2 options, first one is to ignore you as a new comer who doesnt understand financials and just says something they have probably been told by someone as they dont have enough data or depth to explain or 2) a stern post by someone who takes offence

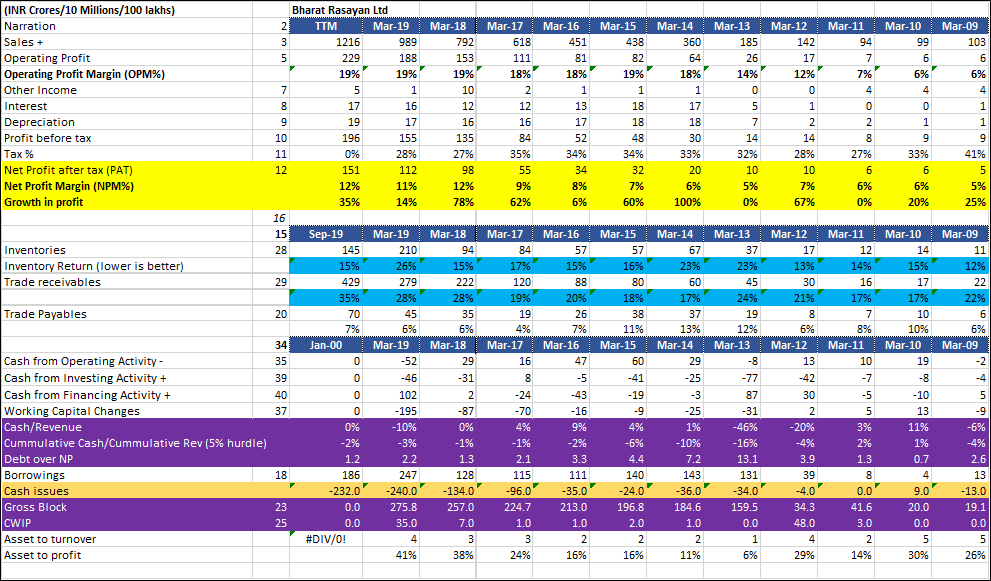

If you see Bharat Rasayan figures below, cash flow to revenue, that is how much of revenue is converted to cash flow, they have gone from -16% to -1% to now -3%.

You can also see where that cash is used. Accounts receivables have been getting higher which is a red flag but inventory and payables are still managed well. But most of the negative cash flow from -1% to -3% from march-19 to now is because cash was used to build capital work in progress

These are just my first draft figures as I use ruby to pull and populate before studying the script further.

Usually when you have cash/revenue of a big minus with constant addition to capital work in progress, like you would notice in manpasand, thats the sign of profit being capitalised

By all means, its your decision how you want to participate in the forum but I think the message was if you are going to say cash flow is a problem than you need to back it up with very strong arguments.

Aren’t we getting a bit testy and hasty in coming to conclusions?

Should we NOT be giving folks enough time at least 24 hours to respond to forensics posts - without hurling accusations of INSULTS, YES MEN, and all such unwarranted stuff.

It is also NOT a good practice - going around spraying the same allegations (of mal-intent) at multiple threads. It doesn’t serve any purpose, and forces us to also defend ourselves (as much as we can ) at multiple places without any value-addition, and getting distracted form the job at hand.

If only we had shown some patience just 24 hours - I am sure these reactions would have been tempered down (?) because the affected parties would have had time to look at the objections objectively and responded/corrected their mistakes even, apologised for any un-intended passionate rebuttal that might have ruffled some feathers. [We CANT expect everybody (Seniors) to drop what they are doing and respond/intervene into passionate discussions just as soon as they occur; highly un-realistic I would think]

As mentioned before - this is a new role - its an attacking role - both sides have to get used to each other (without seeing INTENT when there is none). Urging both sides to wait and suspend judgements till 5-6 such passionate exercises are done and dealt with. A much better appreciation (where each of us are coming from) is bound to happen! Let’s allow that to happen, shall we?

At the same time if the positively inclined optimists are being nudged by this necessary exercise to do their job better (by exposing the blind spots, and/or tendency to brush under the carpet inconvenient aspects of the business (found plenty in every small business - show me one with a clean pristine record, even Mayur Uniquoter had blemishes and SEBI orders against it), it becomes incumbent upon the Forensics guys to do his/her job better increasingly and NOT be blind to biases (inherent, no one is perfect and tendency to opinionate) and get better at the Attack - for example Cash Flows deeper examination was certainly possible.

What deeper analysis of Cash Flow do u want. Have already highlighted my point.

Have Already explained the entire yearly angle of Cash Flow. Shouldn’t cash flow shortage in one year, made up by excess in another year…that’s how businesses operate, it’s never a smooth line up or down. But in this case from what I observed past 3.5 years now have had no excess cash flow (compared to operating profit). Shouldn’t this even out.

Did I not mention right at the start that I’m not raising an issue of fraud, I’m only highlighting that we should be cognizant of risks of overpaying (if we were to), given that things are not fully blemish free…ofcourse nothing is blemish free, and hence you pay more for something and less for something else.

As regards other issues, I might want to reiterate, actions of some Admin guys have not been above board. Case in point is the way a private conversation on IEX thread was handled and how a thread was locked overnight, though there was nothing wrong there. So much so a congratulatory post was also flagged off

For now on suggestion of @Anant, I have reconsidered my decision and deleted all posts blaming few guys.

I get your point but the net profit percentage as considerably increased as well suggesting a change in revenue mix.

Debt has remained the same and as a percentage of balance sheet or a percentage of profit has actually reduced considerably over the last few years since expansion.

Average receivables have been 70 days. In 2013 they were 89 days, roughly the time of last credit crunch. They are now 100 days so basically from 2 months we are talking about payment delay of 3 months after shipment of goods.

This in itself when considering other things like level of loan and conversion of cummulative revenue is not of much concern.

@ankitgupta Do evaluate the Trend here and seek more answers… In March 2017 and 2018 Receivables were the biggest figure in Balance Sheet. In March 2019, while Trade Receivables reduced marginally on absolute basis (and reduced substantially if u compare to days of Sales), the Inventory figure zoomed off…

Then come back to Sep 2019, Inventory reduced and Debtors have become again huge in absolute and Days of Sales terms.

Again this can be due to peak seasonality and may give a wrong impression. May be if a Balance Sheet dated December is prepared things will look very different.

Ideally I would want to see both nos coming back to Normally acceptable levels in March 2020 balance sheet, with no simulataneous increase in any other Balance Sheet Assets side figure.

Note : Red Flags highlight things to watch out for and are not an insinuation. Help us in identifying improvement areas.

My view is that in any stock story/discussions, the most important part is “poking legitimate hole” in hypothesis around that story as it brings out vulnerability/blindspots that gets created. This happens because one starts getting attached to the hypothesis by virtue of having put in lot of effort in understanding the business and then forming an opinion around the same. However, these are typical achille’s hill and one gets self absorbed that he/she is unable to see the downsides/negatives lurking around. The forensic analysis definitely helps in highlighting these blindspots so @ashwinidamani, I feel doing such analysis is important to ensure we don’t get carried away. Hence, perfectly alright and desirable to raise redflags.

At the same time some one like me or @ankitgupta who have tracked BRL story for 3-4 years have tried to unerstand the nuances around the business dynamics. We too have tried to understood some of these aspects highlighted as redflags by either interacting with industry people, company management or subject matter experts. We get answer to some questions and some remain unanswered so we have to live with ambiguities.

I distinctly remember one instance wher I had put up the question of high receivables of 90+ days to a small API company that derived 75% of it sales from exports with high hgh vigour implying they must tighten AR part…however when management explained how the business dynamics work (saying it takes 40-45 days for shipment to reach the destination and then there is credit given to customer of 30-45 days) hence the best possible AR days will be 75 and on average it will be 90 days. They clearly indicated that this is how industry works and we too will have to work on the similar terms thus one will have to live with high AR days. So data was not vert comforting…but the explanation was making perfect sense especially after I checked that out with couple of other players.

Hence I have started to realize that redflags that we raise.see in the story are always a starting point to ask pointed questions to management or industry folks…but many a times if one stops at redflags raised in analysis phase and moves on then the available universe of opportunities may shrink dramatically…when actually there exist a very plausible explanation for the redflags that one has identified. This is even more relevant for small/micro cap companies…the space many of us at VP focus on…because the managements of small/microcaps are in scaling up phase, operate like a promoter owned/driven company, have limited resources for company/themselves and are not the strongest players in the industry who can dictate the terms of business. While tackling all these challenges, the solutions found/decisions made around business porblems may be suboptimal either from business/coporate governance perspective. However, if we start probing deeper, we understand the context and the materiality of the redflags may wane. I have learnt a lot of things from @ayushmit, and one of the most important thing that I have learnt is what is ignorable and what is not. He is extremely good at it…he doesn’t come to conclusion, doesn’t become judgemental, always looks at both the sides of argument before deciding. I think what we as group must strive for is to get this discretion right…Not raising redflags and vilifying someone like @ashwinidamani who is showing blindspots in a story will be counterproductive for those who have conviction in a story…at the same time making redflags only data driven and taking that as “the absolute truth” is equally inappropriate. The key is to work together and find balance…put context around the vulnerabilities and finally agree to disagree with respect if there is diveregence of opinion

@ashwinidamani, though we have not met personally but we have interacted on this forum and on others on various companies and have always appreciated your inputs/analysis. I have been associated with VP forum for a long time now and my experience on VP forum is that the variant views/criticisms are always welcomed and appreciated. In fact, many people whom I know write on VP becuse they think by putting out their views/hypothesis on the forum will lead to strong rebuttals that will give them more insights about the business. VP as a forum has progressed because of the divergence of views/skill set it brings and then people collaborate to arrive at common ground. Hence, if you are getting that impression that VP as community only wants to listen onesided views, it may be because of challenge in articulation and/or spur of the moment comment but as community, most of us would agree, the only way to grow is to listen to diverse view points so my request to you is to put that doubt to rest.

It was great to read the two sides of the story for Bharat Rasayan. Both have put in a lot of efforts to drive home their points in logical ways. For someone who is not invested in Bharat, Rasayan, I read the recent posts on the thread only recently and hence don’t know what actually was there in the earlier posts prior to modification/deletion.

But all said and done, both of you have played the attacking/defending roles quite well and that’s how it should be for most companies. I personally would like such interactions to continue and feel that was what was missing till now. It always helps to get the other side of the story.

I could not find too much objectionable from either side but maybe its so because I am late to the thread and modifications till now have been done. But kudos to both of you for the excellent work.

Only request is to maintain decorum on the forum and if needed try to talk it out with each other if there is something contentious. With other guys on VP I have similar differences of viewpoints and especially with Donald I have in the past had furious arguments as recently as Feb 2020 (Ayush being a witness ) when he was at my place. (he must remember it ) We are accustomed to give it back to Donald too if we feel like it. So there is no culture of shielding anyone at VP. But next day we are absolutely fine and our equation is always better than before. And that is the hallmark of VP ethos. Agree to disagree and shake hands and part with a smile and meet again with love. So all the best to both of you to continue with the good work.

I think both me and @ankitgupta have put everything aside last night itself. Let’s move on… Like all ideas, its best to have a thesis and test it.

My thesis about red flags can easily be tested and accepted/discarded in the March 2020 results and beyond.

Infact if the thesis is disregarded, I would be the first one going ahead and investing because by and large the company looks good and has delivered.

Infact, even if there are some truths in my thesis, I will still invest at a price .where I feel the valuations/opportunity size discounts the negatives.

People and companies both evolve and we have many a great examples for that. When we are starting off, we often focus on more important things like survival and growth and the attempt at building investor friendliness and other things come a bit later.

Have we also analysed the financials of Related Entities in same line of business. That will be an important point and will be a great takeaway based on our learning from Kitex

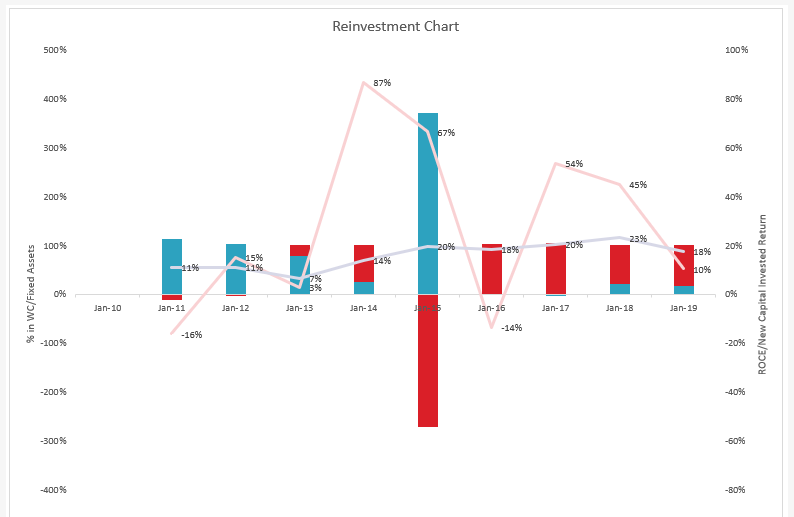

In this, the blue lines are ROCE for last 10 years, pink line is return on incremental capital invested – and bars are % of incremental capital invested in Fixed Assets (Blue) and Working Capital (Red).

The takeaway for us from this chart was :

Till 2015, majority of capital used to go in fixed assets – however, post that the company has been putting more capital in working capitals.

The ROCE has increased in last 10 years, because of higher return on incremental capital, when compared to ROCE. For the last 2 years, ROIIC is reducing, and has gone below ROCE. In last 10 years, whenever it happened, the curve jumped back up significantly. However, in both cases, preceding periods had major capital invested in Fixed Assets.

In my limited understanding, if FY20 does not see a reduction in WC – then we need to understand why this is happening. As we know that the company has been increasing its export sales, and also trying to change product mix (to more patented molecules) – could this be the reason of higher working capital investments, and if yes, when will they saturate?

Or, is it operational efficiency that is questionable here – which means that customer power has either increased significantly or the quality of products have deteriorated?

There is no denying that receivables have increased for the company and debtor days have also increased and now hover around 102 days (as on March 31, 2019) which I think isn’t that alarming. However, one would also have to acknowledge that the scale of the company has increased from Rs.360 crore in FY14 to Rs.989 crore in FY19 and Rs.1215 crore on trailing twelve months basis. Also, as I had posted from the CARE report, the debtors came down from Rs.429.37 crore as on September 30, 2019 to Rs.190.91 crore as on December 11, 2019 (as mentioned in the CARE Report - Bharat Rasayan Limited-12-27-2019.pdf, snapshot of which is given below)

The issue of increase in inventory as on March 31, 2019 has already been addressed in my above post.

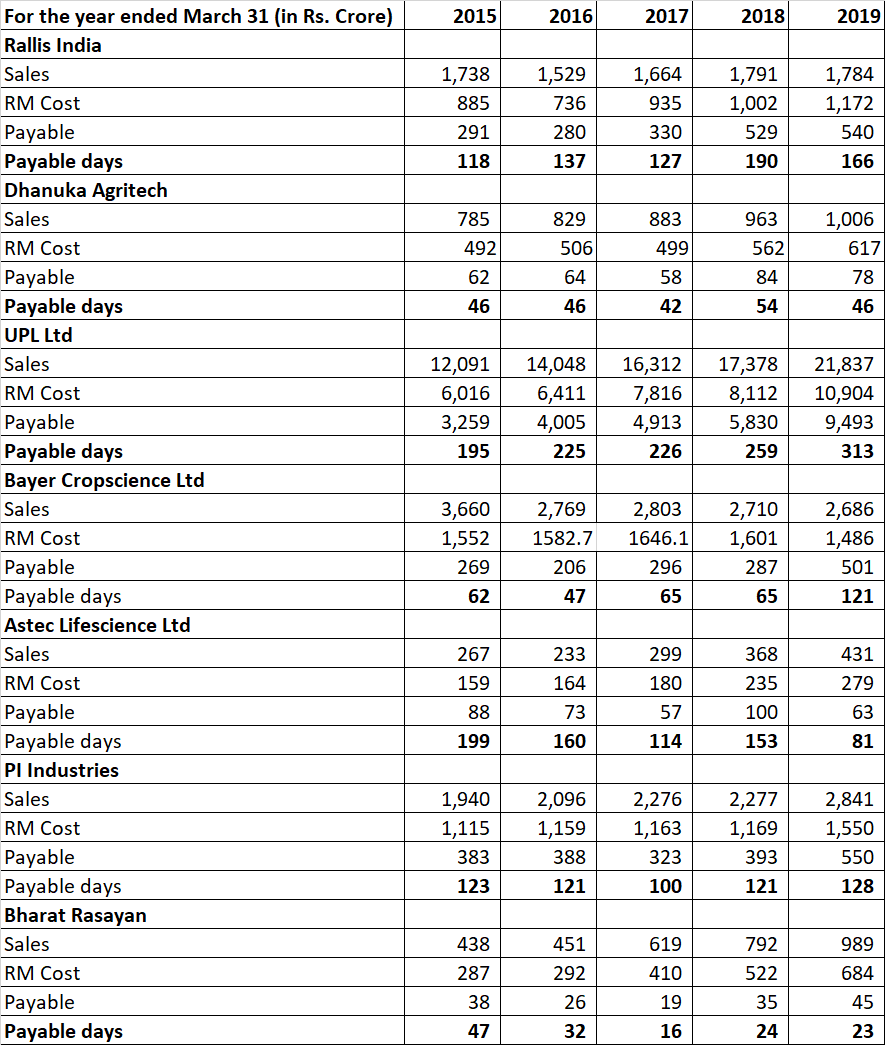

One the issue of cash flow of operations, one major element of cash flow apart from debtors and inventory is payables. A company can stretch its payables and generate higher cash flow from operations. Let’s look at how the payables have panned out for companies in the sector across a 5 year time frame:

You can see that payable days for companies range from 23 days to 313 days with least payable days being of Bharat Rasayan of 23 days. In fact, many companies have increased their payable days while Bharat Rasayan has reduced it. What is the reason for low payable days of Bharat Rasayan? As mentioned in my above post and even earlier, Rasayan’s management believes in paying its suppliers in cash and taking discounts from them. These also ensures loyalty from the suppliers in time of distress where availability of RM is under stress. Lets, assume if the company stretches its payables to 120 days, then payables would increase to Rs.228 crore as on March 31, 2019 and one would get better cash flow from operations. Also, in a growing company, one should also look at how external debt has grown in addition to cash flow from operations.Furthermore, the company has not diluted a single share post listing.

On your point of related party transactions, lets divide the discussion into two parts:

Loans and advances: Bharat Rasayan has taken loans from promoters and related parties and not the other way round. I would be more worried if the company extends loans & advances to the promoters and group companies. Let’s have a look at the trend of loans and advances extended by promoters/related parties to Bharat Rasayan:

The promoters supported the company in FY13 and FY14 by bringing in unsecured loans when the company was executing a capex at Dahej which was pretty big given its size. In fact, promoters have increased the unsecured loans over the years even during FY19 when inventory increase led to higher working capital requirements. One can argue whether the unsecured loans extended by promoters/group companies are fair or not but I personally dont think there are any issues in that (promoters do get interest rate of 9% on the unsecured loans). Also, the transactions related to loan taken and repayments are for promoters/related parties unsecured loans which they have extended to Bharat Rasayan and they might withdraw it as and when required. In fact, as mentioned in the table above, the unsecured loans extended to the company by promoters/related parties have increased over the years.

Transaction with group companies: Bharat Group is the fourth largest agrochemical group in India in terms of revenue (source: AgroPages-Top 20 Indian Agrochemical Companies in FY 2018-19: Backwards Integration, Forwards “OpenAg”-Agricultural news). The group comprises of Bharat Rasayan which is a technical manufacturer and a listed entity & B.R. Agrotech and Bharat Insecticide which are into formulation of agrochemical products. Since inception, Bharat Rasayan was incorporated for manufacturing technicals while these companies were formulation companies. Formulation companies are largely marketing companies (like Dhanuka) and don’t require much fixed assets. Both these companies are debt free. They procure technicals from technical manufacturing companies like Bharat Rasayan, Astec etc or even import it from China or Japan (like PI used to do for Nominee Gold from Kumei in Japan) and market it across India. Their strength is their strong distribution network. In Bharat Rasayan’s case, BR Agrotech and Bharat Insecticide procure some technical from it. These transactions happen at arm’s length (as per promoters) and one way to check is whether these group companies exploit Bharat Rasayan by taking higher credit period. Let’s have a look at sales to group companies and recevables due from them over the years:

As can be seen from above, the receivable days from group companies is infact lower than the receivable days of the overall company. In addition, whether to invest in a company which has other group companies in the same industry (but not same business) is a call that an individual will have to take.

I do agree with @desaidhwanil & @ayushmit that in small and mid sized companies, not everything will be perfect. One can get better understanding about the business model, promoter’s integrity, their vision of growing the business by meeting them and getting feedback from suppliers, competitors etc (which has been pretty good in case of Bharat Rasayan). I have been tracking these company for almost four years now. One needs to ponder why would a Japanes company like Nissan form a JV with the company for manufacturing its patented products (it is very difficult to get into manufacturing of patented products). Let’s have a look at what Nissan has to say about Bharat Rasayan in its press release:

When @Donald wanted to discuss about the company and have a framework on understanding the business in detail, our motive was never to give a view on whether to buy the company or not. It was one business which was gaining strength over the years and we wanted to higlight its journey and strengths.

However, we can still go wrong in any business how much work we do!.

Surely…Have never seen a perfect company except maybe a CIPLA or WIPRO. My role is to highlight negatives for the sake of it and these are real challenges which need to be factored in.

Anyways lets hope for BS of March 2020.

Also, if I remember correctly (I could massively be wrong), BR used to declare results with a timelag on NSE, than on BSE. Did we find any reason for that

As far as Loans, we can always have two views

Why take loans from Related Parties, when you can take from Banks/NBFC.

Sometimes Banks/NBFC do not think far ahead and are not willing to lend cheaply to all promoters. Better to take loans then if available from RPT.

Let us try to find what was the reason for taking loans from RPT

RAY Consulting hosted a webinar on 25th of April, 2020 -RAY Talks series –“COVID 19 - How Indian Ag Chem Industry is coping up….”

We would like to thank everyone who registered for the webinar from across the globe.

It was an awesome experience listening to stalwarts from the Indian Ag Chem industry.

We are pleased to share a link of the same.

Abhishek Agarwal - President, Bharat Rasayan is part of the Panel and speaks lucidly, and at length on Raw Material procurement situation, China situation & sourcing from China. Rahul Dhanuka - Marketing Director, Dhanuka Agritech provided his assessment of what has gone well, and what hasn’t, Dr Rajshekhar - Head Manufacturing, Rallis, and other notable industry persons

I find it extremely intriguing how the total debt from promoters / promoter group ballooned during 2012 to 2014 (assuming your numbers are correct).

2012-13

In FY13 - the promoters/promoter group extended loans totaling ~15 crores to the company.

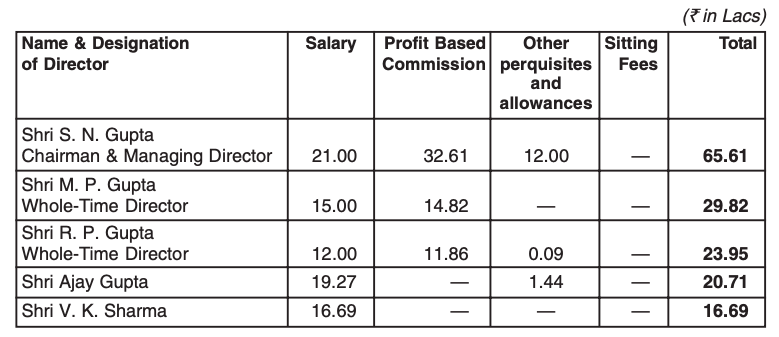

As per 2013 Annual Report, the 3 promoters received combined compensation of 1.19 crore

Fun Fact - The total market cap of Bharat Rasayan was around ~50 crores in May 2013 and the total debt outstanding to promoters was almost half at ~24 crores. Not sure if someone with more experience in markets has observed this before but definitely a first for me.

2013-14

In FY14 - the promoters/promoter group extended loans totaling ~28 crores to the company.

As per 2014 Annual Report, the 3 promoters received combined compensation of 2.92 crores

So assuming promoters compensation was always around 10-15% of PAT over all these years - have the following questions and observations -

What is the source of 20-25 crores of own money lent by promoters over 2012-2014 assuming rest is by group companies?

*** By rough estimates, the total compensation of all promoters across 25 years of Bharat Rasayan’s operations would not be more than 10-15 crores. So they could never have compiled this sum of money from the yearly compensation** Based on the data available till 2008 on screener - Bharat Rasayan has never done PAT more than 10 crore before FY13 and was doing only single digit PAT across 2008-12

If the source of money is legitimate such as inheritance, etc. - I’m assuming the total net worth of the promoters during 2012-14 was at least 50-75 crores.

Given that you’ve met the management in 2017-18 and mentioned this in one of the initial posts - do you know anything about how/where they live, which car they drive, etc.? Very few promoters worth multiple crores would have extremely simple living and especially after the company’s market cap exponentially increased by then.

Also one of the promoter’s sons did their MBA from XLRI, Jamshedpur - curious again given the resources at disposal for them. Could easily have gone to an Ivy league college.

Note: I’m not saying there is something more here than meets the eye over here. I completely understand how promoters use their personal finances is solely their prerogative. However, I’m just trying to put on the hat of a rational logical human on managing one’s net worth - asset allocation - some of the promoter’s actions appear to be quite aggressive and some quite conservative wrt own finances. Then again, they could be the perfect role models of how one should behave despite achieving huge success.

. . . i was reading through last 10 yrs of Balance Sheets of Bharat Rasayan; and i noticed that in initial years one of the agenda items for approval during the AGM was donations - which were strangely of large value relative to profits then earned by the company.

Here is the compilation of all donations made by the company over the years: Donations.pdf (1.1 MB)

Strange one is: of the INR 7.17 Cr. that the company realized from Sale of “Land and Building in Hyderabad”, 5.29 Cr. were donated.

I am not sure if all this info is of any materiality; shall leave it on experts to comment!

The challenge is that these are very subjective opinions and can’t be independently verified. It is perception based so need to be considered with a pinch of salt. But good to know.