hi, can anyone provide some information about bharat rasayan ltd. its near future. thanks & regards

1 Like

Bharat Rasayan Ltd

Disclosure: Not Invested

CMP Rs 987 (11 Dec 2015), MCap Rs 426 crore

FY15 Debt Rs 141 crore, of which 52% is working capital debt. Equity Rs 113 crore

Cash and bank balance Rs 33 crore.

Book Value Rs 266

Face value Rs 10

Promoter holding 75%, has been stable for past five quarters. Remaining held by retail and others. No shares are pledged.

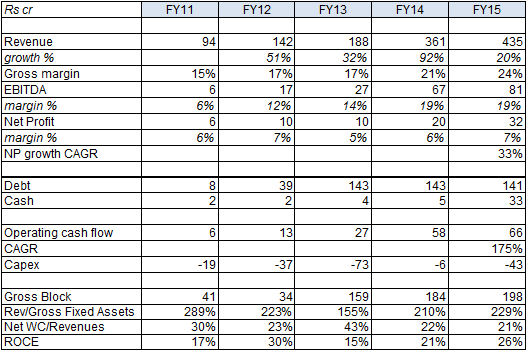

Highlight of the company has been steadily improving financial performance. This has been driven by an increase in Gross Block as well as improving gross margins. The company has added significant economic value by growing while generating increasing ROCE.

About 25% of revenue comes from exports. The company has no forex debt. Raw material is the largest cost component comprising 69% of total costs. Thus fixed cost component is low at 10%.

Effective tax rate has been 33-34%. Dividend payout ratio used to be 10-15% but has dropped sharply to almost nil in last two years.

The company is rated AA-/A1+ by CARE Ratings. Market has rewarded the company by increasing both PBV and PE ratio, the latter increasing from 6.1 times in FY13. However, it seems the strong cash flows and future growth is still not priced in the stock (PE of 13 times), which trades cheap compared to its historical EBITDA growth.

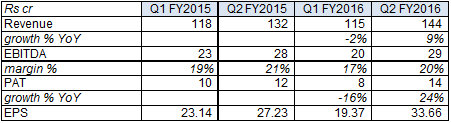

- Quarterly results

The company’s growth has somewhat stagnated in H1 FY2016 and Q1 performance was lacklustre. EPS for the first half of FY2016 is Rs 53, but the latter half EPS tends to be lower (was Rs 24 in FY2015). Assuming a scenario of no growth, the company should post an yearly EPS of Rs 77 in FY2016.

Later posts will focus on company’s products.

To be continued…

8 Likes

Bharat Group –

Comprises 3 companies : Bharat Rasayan Ltd. (BRL), Bharat Insecticides Ltd. and Bharat Agrotech Ltd.

Though in allied businesses of catering to agriculture industry, inter-company transactions / related party transaction are negligible – undermines good corporate governance. Total turnover of Bharat Group for FY2015 is Rs. 1035 cr. with BRL contributing majority of it at ~Rs. 470 crs.

Product –

BRL is manufacturer of Technical Grade Pesticide (TCP). Any pesticide has active ingredient and non-active ingredient. Active ingredient, also known as TCP, is a constituent working to destroy pests.

Non-active ingredient facilitates storage, transportation of product in totality. Basically, TCP is key raw material going into manufacturing of pesticide. TCP seem to be functional equivalent of OEMs to auto manufacturers. Link below gives more insights into TCP - http://www.vikalpa.com/pdf/articles/1990/1990_apr_jun_23_33.pdf

Capacity –

2 units at Mokhra (5000 MT) near Rohtak and Dahej (15000 MT) in Gujarat.

Dahej capacity commissioned in FY2013. It has filliped sales and profitability. Expansion was funded by debt. D/E increased to 2x in FY2013 from under 1x in FY2012.

Sales filliped from 97 crs. in FY2011 to 188 crs. in FY2013 and 439 crs. in FY2015.

Not sure why have OPM has tripled to 18% in FY2015 from 6% in FY2010

Certifications – BRL has ISO 9001:2008, ISO 14001:2004 and OHS 18001:2007 certification catalyzing long term partnership with institutional and foreign clients.

Clients – No meaningful data available. Will have to dig further.

Competition – very thick competitive space including companies like Kanoria Chemicals, Dhanuka Agrotech, Sabero Organics, Insecticides India, Camson Biotech, Kaveri, Rallis India etc.

Some concerns/aberrations –

- Co. passed a resolution in FY2015 AGM to invest/advance loan/guarantee transaction up to Rs. 500 cr.

- R&D expenditure as % of total expenses is too low (0.2%). Google search and some on-ground research suggests, TCP manufacturing involves lot of research to sustain

- What are the growth drivers in coming years – expansion completed 3 years back, no new high margin products underway?

- Raw material price risk – drivers of OPM?

Some highlights from AR read –

- Foreign exchange earnings and outgo almost net each other, hedging exchange rate risk. This is consciously done by management.

- Rising exports are mitigating vagaries of domestic monsoon – Exports as % of sales have risen from 20% (Rs. 27 crs.) in FY2012 to 30% (Rs. 117 crs.) in FY2014

- No equity dilution over last decade while capacity quadrupled

9 Likes

Hi Pratik,

What is your opinion about the company’s quarterly performance? Their financial performance, except the margin improvement, was largely driven by addition to gross block.

Hi Aditya, i agree with your analysis.

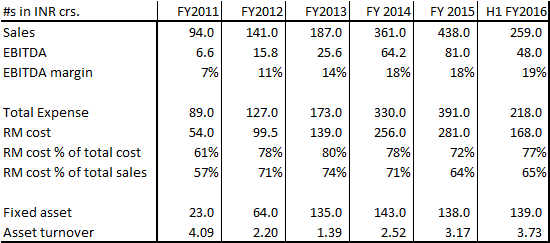

Factsheet -

Takeaways -

Sales have almost grown ~5 times over last 5 years in line with capacity expansion. There is no capex pending to come on stream now.

EBIDTA margins have also doubled. RM cost as % of total sales have declined by 6%

Probable reasons -

a. Am not sure of what are key raw materials for TCP manufacturer and how its prices have fared over last 5 years…Please help with this input if someone can

b. It might be due to increased efficiency of new plant at Dahej , asset turns have increased → leading to improved margins

c. Also increasing share of exports might be key for EBITDA margins to double

Key open points -

a. What is key raw material (RM) for TCP manufacturer? How are the prices of this RM moving over last 5 years?

b. TCP plants generally operate at 50%-60% utilization levels - what is peak estimate of sales from current installed capacity?

3 Likes

with such strong numbers why is the share still trading at 11 pe and 2 bv. is to do with the debt of 141 crs debt/equity-1.25.comparable stocks like PI and dhanuka in the same sector are far more expensive. are we missing out something here

List of 20 agro companies that performed well even in bad monsoon http://news.agropages.com/UserFiles/FCKFile/zkc_2015-11-16_16-43-51_541.jpg

{kind=link}

Read the recent interview by chairman Sn Gupta

This is registration for acarciadies technical grade indigenous manufacture CIBRC 360 meeting

Chemicals Pvt Ltd

9 (3)

Cyflumetofen

Dhanuka Agritech Ltd.

9 (3)

Propargite

Bharat Group

9(4)

9 (3)*: registration only for export, belongs to 9(3) registrations

9(3) registrations: This guideline is for registering a new pesticide (technical grade or formulation) or registering a new import source of technical grade pesticide or first time indigenous manufacture of technical grade pesticide or formulation. This is a permanent registration and does not require any renewal.

9(4) registrations: This is Me-too registration for indigenous manufacture of technical grade pesticide and formulations.

If we refer to CIBRC earlier meetings for the last 10 months it clearly shows that Bharat rasayan late has got nearly 8/9 new registration in pesticides and insecticides all are technical grade

The industry EVEBITA is around 12 BRL is around 7 as of fy 15 operating cash flow of 59 cr BRL is quoting less than PCF Of 10 the fy 15 ROCE 28 and three yr ROCE 25 and 3 yr ROE > 25

The promoter holding is 74.5% out of 42 lac shares HNI holding another 10% literally very low floating stock even though the dividends has been low they have not diluted the equity nor have issued any preference capital and no pending warrants for conversion fy 17 we could see at present growth around 580/600 with ebita of 100 and fy16 around 500 cr and ebita of 85 cr

I think the lower side is limited and risk to reward seems attractive compared with peers

Even on technicals trading above 20 day EMA TMA and WMA

invite comments on future scalability and valuations

Disl invested a small qty

5 Likes

I think Pratik has given a detailed report as per there website they are also doing toll manufacturing for major manufacturers like Godrej agro vet and Mahindra in there excesss capacity in Dahej so without any further Capex can they sustain the same growth because at present the capacity utilisation is less than 70%

And CIBRC registration shows some new molecules pattern pending for approval of commercial production I have no idea How to check this can u please go thru that.

The interesting thing to watch in growing company like BRL is

Sales var 3 yrs. (46%) > Sales var 7 yrs (30%)

Profit var 3 yrs. (46%) > profit var 7 yrs (32%)

ROCE 3 yrs avg (23%)> ROCE (29%)

ROE. 3 yrs avg. (27%) > ROE (32%)

ROA 3 yrs. avg. (15%) > ROA (21%)

This is apart from the growth in gross block over 5 yrs and very good asset turn over ratio with the least inventory and trade receivables

The dividend policy has been poor and debt is little on the higher side but the growth story is very good

Can this be sustained in coming years looking at the prospects of the product registrations it seems possible we have to ascertain the growth but compared with peers at the present m.cap this looks undervalued

Seniors please comment

Invested a tracking qty

Result announced : https://nseindia.com/corporates/corporateHome.html?id=eqCorpAnnouncements&radio_btn=company¶m=BHARATRAS

1 Like

Except management paying itself about 17% of profits, everything else looks good to me. Why is it trading at lower P/E compared to its peers?. Could it be because 30% of its revenue is coming from RPT? (AR 2015)

D/E is also brought down to 0.76 as per 2016 financials.

2 Likes

Bharat Rasayan June Quarter : https://nseindia.com/corporates/corporateHome.html?id=eqCorpAnnouncements&radio_btn=company¶m=BHARATRAS

Disc : Holding (15% of my PF)

1 Like

what is RPT? Whats your take on results?

1 Like

Annual Report LInk : http://linkintime.co.in/website/gogreen/2016/AGM/Bharat%20Rasayan%20Limited/Annual%20Report%20(2015-16)%20-%20BRL.pdf

Amit

1 Like

As per AR Metaphenoxy Benzaldehyde is contributing 21.57% of turnover, that means the company has diversified their product portfolio.

Amit

Why company didn’t report shareholding patters quarterly to exchanges?

Around INR 64 cr are outstanding towards management personal and their relatives. I am not sure if this is a good corporate governance practice as I question the value it adds to the company. Also wont this money better used to pay the debt the company has on it books?

no position, not invested

1 Like

Any queries for Bharat Rasayan AGM? Plan to attend it on 28 Sep 2016

@Vivek_6954 Could you check about the outstanding towards management team and relatives?

Hello,

Any update on AGM of today?

Amit Anam