Atleast read this thread from beginning to answer so many of your queries already addressed

1 Like

Good report on Bharat Rasayan with good data points. Could it lead to attracting instt investors and rerating?CARE REPORT DEC 19 Bharat Rasayan Limited-12-27-2019.pdf (1.7 MB)

2 Likes

Trade receivable of the company increased from Rs. 221.61 crore as on March 31, 2018 to Rs. 279.09 crore as on March

31, 2019 and further to Rs. 429.37 crore as on Sep 30, 2019. Increase in debtors as on Sep 30, 2019 mostly pertains to

sales in H1FY20. Further, debtors of the company came down to Rs. 190.91 crore as on December 11, 2019.

As per Care report.

1 Like

May the trend continue for the next 10 years and more…

results look just OK

sales up 17 % YoY

PAT up 19% YoY

views from others awaited

stock just fairly valued in my view

since they wont hold any concall

BR executes joint venture with Nissan Chemical Corporation:

https://archives.nseindia.com/corporate/BHARATRAS_18022020142117_NSE_Intimation__BHARATRAS.pdf

4 Likes

Enclosed find press release from Nissan chemical co a biggie declaring BRL as a trustful company with outstanding manufacturing technology . seems recent brownfield expansion at dahej was for above JV only.

BR shud get rerated now post this v positive development. Just hold this gem for next few years and see your money multiply.

discl invested since last 4-5 years and havent sold any share but have averaged on upside.

en2020_02_18_02 NISSAN CHEMICAL PRESS RELEASE ON JV WITH BHARAT RASAYAN.pdf (182.0 KB)

10 Likes

Hi @ankitgupta

I am coming from the Deep Dive Processors thread.

I found out via this pdf https://www.nissanchem.co.jp/eng/news_release/release/en2020_02_18_02.pdf that, NISSAN has already given its “proprietary” pesticide Elsan for toll manufacturing.

Can you shed some light on the international clients and the kind of molecules, BR is doing toll manufacturing for ?

For example, I can see its exporting Lambda Cyhalothrin for Syngenta. Do you have any color if its mere “export” or is it part of toll manufacturing?

7 Likes

@ankitgupta @Donald @rohitbalakrish_

Red Flag 1 and Biggest Red Flag for Bharat Rasayan is the abysmal quality of Cash Flow Conversion

Note the last 3 years specially and also the movement in profits during those years.

Management might argue, that new customers have stricter payment cycle, but here money due from previous year is also not being converted. Ideally even a strict payment term gets evened out in Cash Flow , because dues of last year would be paid this year and so on. I dont even agree with the increasing sales argument

Because the gap in Cash Flow is substantial even after considering Sales increase

Coincidentally during the same 3 years, Debtor Days have also worsened and now stretch to 100 Days+

What might cut teeth is that March could be Season peak for Bharat Rasayan, but from my discussion and understanding and also from observations across various other listed players, this should not be true.

I hope the @adminph2 does not flag off this argument. Nowadays messages are flagged, even when I write a appreciation post

Note : Red Flags are causes of concern and not an insinuation. People should find answers to Red Flags before investing

33 Likes

Red Flag 2 : May not be in control of Company, but nevertheless a Red Flag

The details of top 4 public shareholders - They seem to be controlled by one entity viz Ambaa Securities

Also, some directors in Ambaa Securities are Gupta’s by surname, but I cant draw any concrete conclusion from this

@Donald @ankitgupta @rohitbalakrish_

Note : Red Flags are causes of concern and not an insinuation. People should find answers to Red Flags before investing

Sometimes Concentrated Shareholding is a blessing too

13 Likes

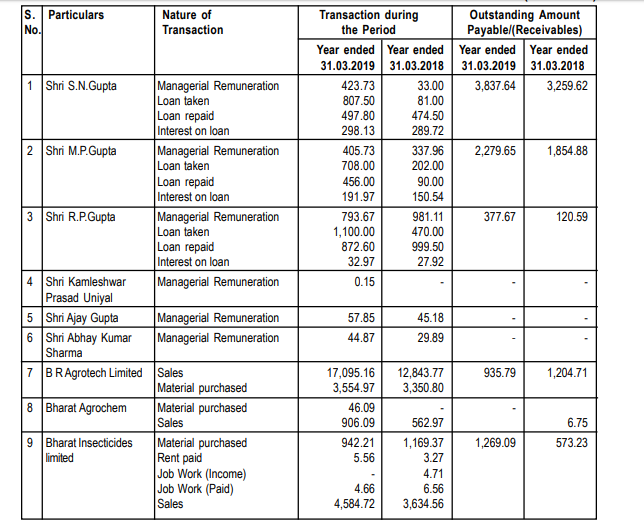

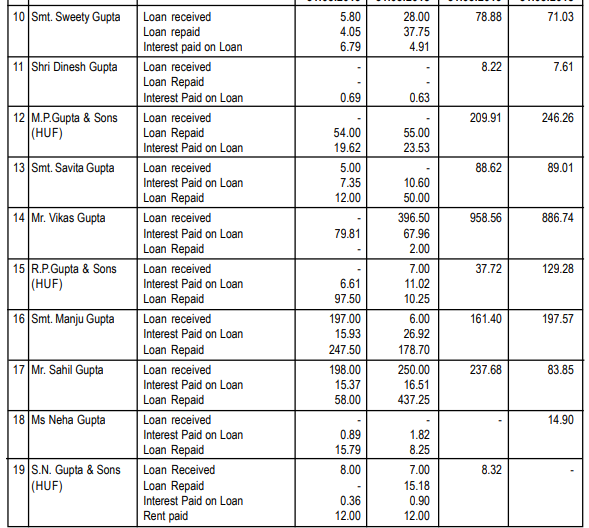

Red Flag 3 - Related Party Transactions

Almost every Director has taken and repaid loans from the company during the year. Worse the Auditor in his report says no Related Parties has taken loans during the year. Refer Caro report where they mention no loans granted to parties covered u/s 189 of the Act. It could be a naive error or maybe an audit quality issue

Not to mention the Salea and Purchase Transactions with two sister concerns

Note : RED FLAGS only are an effort to be careful and dig deeper. They dont comment on quality of company or dont make any allegation on the company. Everything can be purchased at a value

11 Likes

As most of us know that Balance Sheet is a number as on date i.e. March 31st of every year while profit and loss account is for the full year.

Let’s look at some numbers of the company:

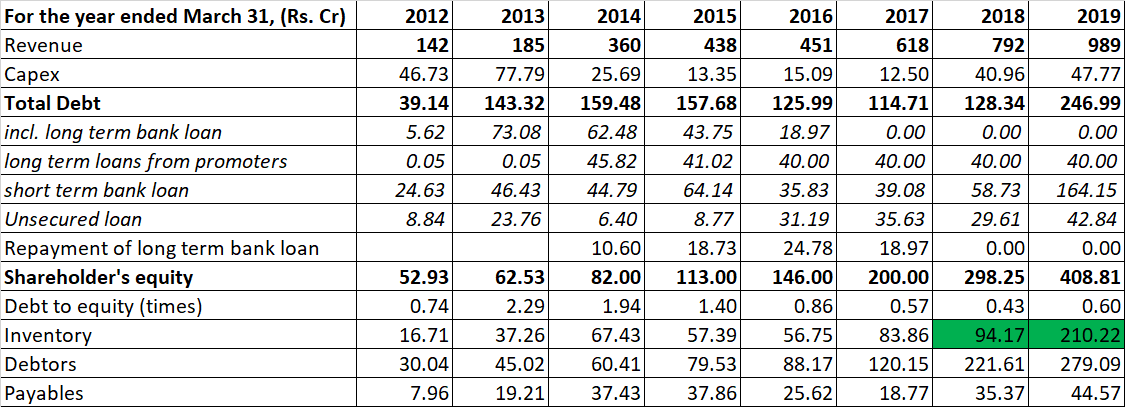

In FY12 and FY13, the company had started construction of its Dahej plant and spent close to Rs.150 crore on it. For the said capex, the company took long term bank loans of around Rs.75 crore. The company prior to the capex, had sales of Rs.142 crore in FY12 and networth of just Rs.53 crore as on March 31, 2012. You would appreciate that company had to even take corporate loan from banks to fund it since it was a large capex given its size at that time. The company post that was successfully able to ramp up Dahej plant and grew its sales from Rs.185 crore in FY13 to Rs.989 crore in FY19. **In the mean time, it fully repaid (in fact, prepaid - you can check from AR about the scheduled repayment and repayment made by them) the long term bank loans as on March 31, 2017. Post that it has done capex of Rs.135 crore (including capex done in H1FY20) which has been fully funded by internal accruals. I would doubt if the company was not generating enough cash flows, how will it be able to fund these capex without taking long term loans (I do understand that good companies will try avoiding taking short term loans to fund capex which company hasn’t done). In the mean time, company’s debt to equity has reduced from 2.29 times as on March 31, 2013 (at the time of Dahej capex) to 0.60 times as on March 31, 2019 while its sales have jumped more than 5 times. Furthermore, out of the total debt of Rs.247 crore as on March 31, 2019, only Rs.165 crore is external bank debt (which is also on the higher side for which reasons will be explained in these post later) and remaining from promoters and group companies.

Now, let’s talk about working capital. Please do understand that cash flow from operations is as much a function of inventory and receivables as it is of payables. In FY13, when company had sales of Rs.185 crore, it’s payables were Rs.19.21 crore as on March 31, 2013. Six years fast forward, the company’s sales have increased by almost Rs.800 crore while its payables have increased by just Rs.25.36 crore (RM purchase have increased from Rs.100 crore during FY13 to Rs.725 crore during FY19) Please understand that the company’s management thinking is such that they want higher discounts/cash profits form its suppliers for paying them in cash. I don’t agree with your argument that dues of last year haven’t been recovered as receivables are as on date. As long as receivables are rolling, we shouldn’t have any problem. Let’s look at whether dues are recovered during the year or not. The following statement is from the CARE press release dated December 29, 2019. Attached for your reference Bharat Rasayan Limited-12-27-2019.pdf (629.2 KB) :

Rasayan’s debtors peak as on September 30th every year and not March 31st as you have mentioned in your post. Domestic agrochemical sales (formulation players are customers of Bharat Rasayan which supplies them technical) for Kharif sowing happens in September quarter and you can check receivables of formulators like Rallis, Dhanuka etc to verify the jump in receivables which happen in their balance sheet as well during September quarter.

Now coming back to negative cash flow from operations during FY19, let’s look at what led to such cash flows. Major reason for negative cash flow from operations during FY19 was increase in inventory from Rs.94.17 crore as on March 31, 2018 to Rs.210.22 crore as on March 31, 2019 due to increase in finished goods inventory from Rs.56.41 crore as on March 31, 2018 to Rs.127.83 crore as on March 31, 2019.

These finished good inventory got shipped in Q1FY20 which also resulted in company’s sales jumping from Rs.245 crore in Q1FY19 to Rs.354 crore in Q1FY20.

I do agree that company’s debtor days have increased but for that enough reasons have been provided and discussed.

16 Likes

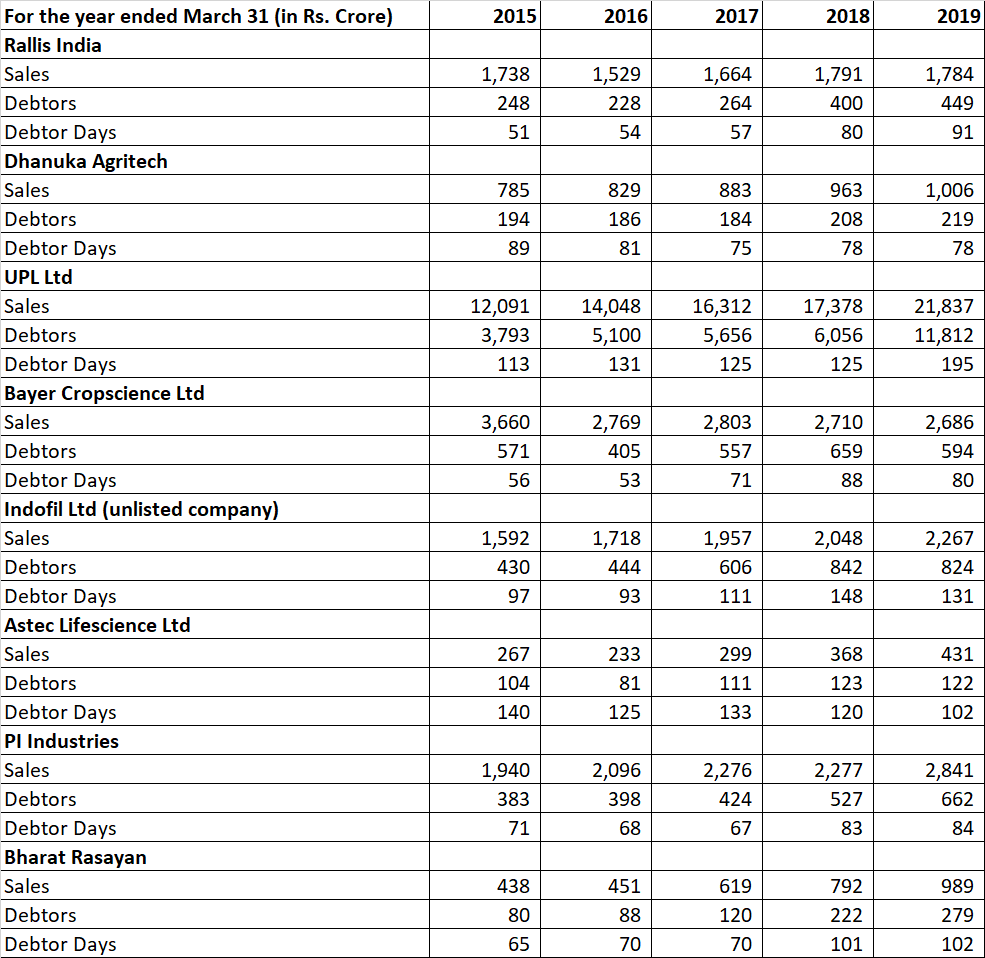

Also, please find below working on the debtor and debtor days for few of the agrochemical companies. You can see that in many companies debtor days has increased. The only direct comparable of Rasayan is Astec Lifescience which is a pure play technical company while rest of the companies are either pure formulators (serving largely to domestic market) like Dhanuka or have dual models (formulation plus CRAMS/CSM/technicals) like PI, Rallis.

11 Likes

I have already mentioned that Red Flags just needs more probing and is not an insinuation. We just need more probing on Red Flag nothing else.

So let me again try to share my version

Your first point relates to Total Cash Flow, which is a bit different from the Operating Cash Flow Argument.

As you would have seen, I have not commented on Cash Flow by just looking at 1 or 2 year but on 10 year aggregate basis. On 1 10 year basis, there is too much volatility in Bharat Rasayan. If normally Cash Flow is negative in some year, then there should be a huge positive in some other year and on a 5-10 year basis there should be instances when Cash Flow goes above 100% also, if there has been a huge shortfall in some year. In the end if on a 10 year basis if things are around 70% mark, then its always ok.

If FY 17 had some new situation, then FY18 should even it out or else FY19 should even it out.

You have tried pointing out the FY 19 abnormality, but what about FY17 and FY18.

Simple argument is if FY17 collection was low then FY18 should have filled in the gap. Sometimes if sales is on a very fast trend then maybe gap does not get filled, so I looked on to FY19 also. For this reason itself I compared Rising Sales with Rising Cash Flow Gap.

Meanwhile FY20 half year end nos of Cash Flow do not show recovery of Cash Gap left behind from FY17, FY18 and FY19

Also Inventory Ratio on screener shows no such huge variation in FY17 and FY18 and is around the same mark of 8-9 times in FY15-FY 18

10 Likes

The role given to me in this instance is to Ask Tough Questions and highlight negatives. @ankitgupta May be I have lesser or even more knowledge than you in studying both business and numbers, but I atleast know what role I have to play where.

I can insult you back in more ways than one, but the partial @adminph2 will not take actions against VP Top Comtributors and instead ban me.

Infact one post of mine was flagged because I appreciated the good insights of a person (positive comments)

3 Likes

Hi Ashwani

Can you please state in which clause of CARO Report auditor has opined that the Company has not accepted any loans from directors.

Kindly note clause iii) states that “(III) The Company has not GRANTED any loans, secured or unsecured to companies, firms or other parties covered in the register maintained under Section 189 of the Act. Accordingly, paragraph 3(iii) of the order is not applicable.”

In clause (IV) it is mentioned that “According to the information, explanations and representations provided by the Management and based upon audit procedures performed, we are of the opinion that in respect of loans and investments the Company has complied with the provisions of the Section 185 and 186 of the Companies Act, 2013.The Company has not provided any guarantees or security as specified

under Section 185 and 186 of the Companies Act, 2013.”

185 and 186 prevent Companies from granting loans to directors (to prevent siphoning off of funds)

In clause (XIII) it is mentioned that " According to the information and explanations given to us and based on our examination of the records of the Company, transactions with the related parties are in compliance with Sections 177 and 188 of the Act where applicable and details of such transactions have been disclosed in the Standalone Ind AS financial statements as required under Indian Accounting Standard (IndAS) 24, Related Party Disclosures specified under Section 133 of the Act"

188 requires all related parties transactions to be at arms length and approved by shareholders.

A Company is well within its rights to accept loans from shareholders directors and it should be seen as a positive sign as long as company is not paying exhorbitant interest rate on that.

However, I think you are considering reverse scenario that company has given loans to director.

That would also be a very serious offence since penalty for violating section 185 is imprisonment of directors.

However that is not factually correct in this case as can be seen from BR balance sheet and related party balances disclosures. Hence I feel this is no red flag.

2 Likes

As you can see, many promoter/directors have paid interest on loans granted to them by the company. I was of the opinion that such granted loans should have been mentioned in the register maintained u/s 189 of the act

1 Like

Yes you are right that all related party transactions have to be entered in the register maintained u/s 189. But Auditor has to only comment on loans “granted” as per CARO requirement given by MCA under companies act.

I know this because I am also an auditor.

Red Flags never point to fraud alone.

Red Flags point out to flaws in the business model.

Red Flags alert us when not to overpay.

Red Flags highlight things which we might have overlooked

Red Flags highlight improvement areas

However, some people might be having their own agenda in pushing stocks and hence are not bothered about listening to shortcomings in the stock.

How can one pay same thing for Emami and HUL.

Red Flags help you in finding that difference in quality.

No where have I said, Bharat Rasayn nos are not true. But probably if we look at some numbers differently then we can judge that maybe 17-20 PE is enough for a BR and hence not a buy at this price.

Or maybe we can probe deeper and conclude that we are ok with the issues and they are not material enough and there is margin of safety compared to the bright future

9 Likes

They have granted loans to promoters na…That is why promoters paid interest