I’m trying to figure interest rate charged by directors but I’m unable to do so.

I’m trying to figure interest rate charged by directors but I’m unable to do so.

Brief note on the company

About the company

Bharat Rasayan Limited (BRL), the flagship company of the Bharat group, was incorporated in 1985. The company is engaged in the manufacturing of technical grade pesticides, which in turn is used from manufacturing of formulations for agrochemical industry. Apart from BRL, Bharat group also has two other group companies, Bharat Insecticides Limited and BR Agrotech Limited, that are engaged in manufacturing of formulations and packaging material of the products. Together, Bharat Group is amongst the top 10 agrochemical groups in India. The company has two plants, one at Rohtak with installed capacity of around 4000 metric tonne per annum (MTPA) and the other one at Dahej with installed capacity of around 7000 (MTPA). One of the key differentiation for a technical grade pesticide manufacturing company is the chemistry reaction skills and relationship with clients. The commencement of operations of Dahej plant from FY12 onwards was turning point for the company.

About the promoters

The Gupta family, Mr. S.N. Gupta, Mr. M.P. Gupta and Mr. R.P. Gupta (all brothers), are the promoters of the company and hold 74.79% stake in the company. The promoters came across a humble, cost conscious management (they don’t bother spending much on the quality of paper used for printing their ARs and when we visited their office, they didn’t even offer us tea/coffee ) who had hands on approach towards running the day to day operations of the company. The management maintains that the BRL is the flagship company of the Bharat group and all the intercompany transactions (sales of technicals from BRL to group companies) happen at the market price and the group maintains pretty high standards with respect to the corporate governance. One other thing which was pretty interesting about the promoters was that they did not provide any guidance for the future during AGM as well as during one to one meeting and said that the agro-chemical markets is highly volatile and becomes extremely difficult for the company to provide any projections. The management even said that the PE players are not even allowed in their office.

Operations of the company

The revenue breakup of the company is given below:

• Group companies – 25%

• Exports – 30% (which includes MNCs and other players. Primarily in Asia and Middle East)

• B2B (MNC, Domestic companies) – 45%

Currently, MNC constitutes around 15 – 20% of the total revenues of the company which the management wants to increase to 40% over the medium to long term. There is stiff competition in the domestic markets and profitability margins are low. MNC contracts are sticky in nature, have higher profitability margins and take a long time to develop. BRL supplies to agrochemical majors including Syngenta and Nissan. In general, there is no exclusive relationship that these MNCs have. Nissan can tie-up with Dhanuka for certain products and BRL for others depending on chemistry skills and sustainability of the product/promoter/company and quality apart from the price. There is a shift happening in the Japanese agrochemical companies where they are shifting their manufacturing from China and Japan to India. BRL seems to be in talks with these companies for manufacturing of off-patented as well as patented molecules.

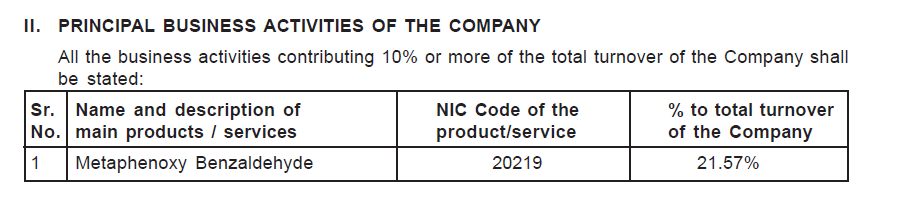

The group has market leadership in many products which include Meta Phenoxy Benzaldehyde (MPB), Lambda Cyhalothrin (LC), Piroxofoppropinyl, Thiamethoxam and Cypermethrin among others for which the company is a preferred supplier in the international markets. During FY16, MPB contributed 21% of the sales (50% increase compared to FY15 on a y-o-y basis) while LC contributed 5 – 7% and Chlodina/Pendamethil (Herbicide) contributed 5 – 7%. The company has around 200 international registrations primarily in Asia and Middle East. Company tries to commercialize 2-3 products every year. The company is planning to register some of its products in the Latin America markets primarily Brazil. Registration in Brazil take a lot of time and even cost of registration is pretty high at Rs.3 – 5 crore. Furthermore, the company might register its products in US markets which also involves a lot of cost (~Rs.20 crore for one molecule) only if it has firm orders in hand. We have been following the registrations of the company on Central Insecticides Boards & Registration Committee (CIBRC) where all the agrochemical companies have to get any of their molecules to be manufactured at their plants to be registered with them. Interestingly, over the past two years, the company has been increasingly registering for molecules which have low competition. However, the management in our meet reiterated that although a low competition might mean the volumes required for the molecules are low although it might have higher margins.

The capacity utilization for the both the plant is around 100% during peak season (H1) while it is 80% during the lean season (H2). The capacity utilization is measured by utilization of equipments. The company over the past 2 – 3 years has been doing capex of just Rs.12 – 15 crore. The management has reiterated that it will only do a large capex (of more than Rs.50 – 60 crore) only if it has firm orders in hand. The Dahej plant is hardly utilizing ~50% of the land available currently and the company can easily expand over the surplus land available there.

Financials

• The growth trajectory for the company commenced from FY12 onwards with construction of Dahej plant. Post commencement of the plant, with better product mix and higher realization, company’s PBILDT margins have also expanded significantly.

• Even during FY16 (as per management), the company’s volume had grown by 30% on a y-o-y basis but on account of decline in prices of crude, the company reported just marginal growth in revenues.

Key Triggers

• Contract manufacturing opportunities with MNCs: The management has stated that there is a shift happening for manufacturing from Japanese agrochemical players to Indian counterparts. Apart from these opportunities, there are other opportunities from European players as well. These relationships take years to fructify and these MNCs follow strict procedure regarding quality, timeliness, environmental norms, strengths in chemistry etc. It is not very easy for any new entrant to get big contracts from them. Furthermore, management also said that they are also looking for contract manufacturing of ‘patented’ molecules. We have seen that to get contracts for patented molecules is very difficult and sticky in nature. These contract can be very long term and sticky in nature. In other terms there can be ‘longevity’ to the business.

• Registrations in international markets: The company is looking for registration of its molecules in Latam markets especially Brazil. Brazil is one of the largest agrochemical markets in the world and can open big market for the company. Furthermore, the company is also looking for opportunities in US and European markets but since the registration in these countries requires lot of investment and time, they want to file only after getting confirmed orders in hand.

• Conservative and ‘baniya’ management: The management came across as an extremely cost concision and conservative who understand the importance of capital allocation. They have hands on approach to the operations and have never diluted in the past. Any big capex announcement can be perceived as company having got big orders in hand. Furthermore, they hold 75% stake in the company and have never diluted in the past. One might have some inhibitions two other unlisted companies into formulations space (who are debt free), but management clearly stated that all the transaction between the companies happen at arm’s length and at market price.

Key risks

• Very limited information shared by the company: The company doesn’t share much information with the shareholders and one will have to rely on quarterly results, annual reports and AGM for any substantial information. One will have to trust and have faith in management for being invested in the company for long term.

• Linkage to crude oil prices: During last year, although there was 30% growth in volumes, the revenues hardly grew because of decline in crude oil prices. Any significant volatility might have an impact on the realisations and hence the profitability of the company.

• Working capital intensive operations: The operations of the company are working capital intensive and it has an operating cycle of 80 – 100 days primarily on account of high inventory and receivables. However, the company has generated positive cash flow from operations in five out of six last financial years.

• High competition and dependence on monsoon and agroclimatic conditions

Valuations

• The company has achieved EPS of Rs.73.20 in H1FY17 as against EPS of 79.74 in full year FY16. H2 is relatively weaker compared to H1. It is trading at a trailing P/E of around 17 – 18 times earnings

Key financials of the company.Bharat Rasayan_Key Financials.docx (12.9 KB)

Disclosure: Invested from lower levels. A lot of information in the note is as per our discussion with the management.

@ankitgupta

Your analysis is to the point! and highly informative

Going thru the report of 2010 & 2016, couldn’t find revenue contribution from each product, where else we can find? Capital expenditure R & D is meager…Where do they have moat? Can you throw some light on their new product plans and launches…

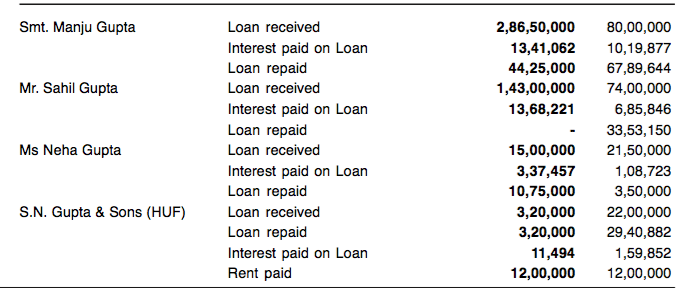

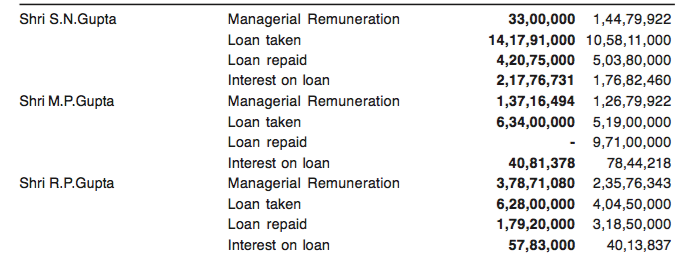

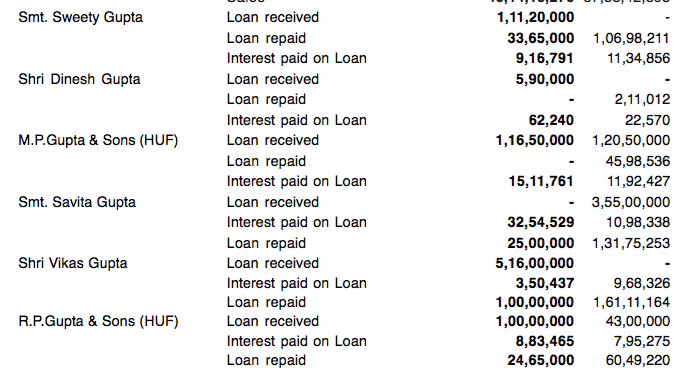

How do you view related party transaction like loan to directors??

As I mentioned before, the company does not reveal much about their operations and products in their annual report or doesn’t even conduct concalls. Most of the information that I have shared is as per some data available in their AR and our discussion with the management during the AGM. Some data is available in their AR:

The company had done huge capex during FY12 and FY13 for setting up Dahej plant. Furthermore, they do small capex of Rs.15 - 20 crore every year to increase capacities by adding new machineries. The management stated that their focus currently is to manufacture high margin products and reduce debt. I track their registrations by following the CIBRC monthly molecule registration data (http://www.cibrc.nic.in/369rc2016.pdf).

I think ‘MOAT’ is one of the most abused word used by value/momentum/short term investors. There are very few businesses which have moat (the way Patanjali is giving competition to the FMCG companies, the list is ever reducing). For me, the investment thesis is based of following factors:

I am happy that the funds are coming into the company and not going away. The company has taken unsecured loans from promoters/group companies and not given any loan. Many of the companies do the opposite.

Thank you for the immediate response

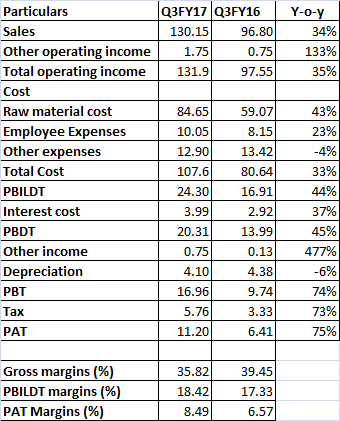

Bharat Rasayan has come up with good set of numbers for Q3FY17 with 34% growth in sales and 75% growth in profit after tax.

Key financials:

Operating leverage seems to have played out during the quarter resulting in higher PBILDT margins despite decline in the gross margins.

Thanks @ankitgupta for the detailed work on this company.

How do you foresee the topline growth panning out for next couple of years on the high base of FY17. Although YoY sales looks optically better due to subdued FY16, 2 year cagr sales growth is around 16% on TTM basis.

Interest cost spike (up 37% YoY) mostly from working capital loans(?) is a point of concern.

The company is known for sweating its assets really well, with historically high fixed asset turns so given a visibility on order book execution can pan out well.

Disclosure: Invested from lower levels.

Hi Rudra,

It’s very difficult to predict the growth in the topline of the company as the company doesn’t share much. However, having met the management, I do have some confidence on their abilities (might be biased as well). I also know some of the growth drivers like entry into contract manufacturing for MNC customer especially Japanese client for patented molecules and registration in foreign markets like Brazil. Looking at two year sales CAGR seems a bit harsh to me. Last year they had 30% growth in volume terms but because of fall in prices of crude, the same was not reflected in value terms. The way the management has scaled up operations of the company post the commencement of operations of Dahej plant is commendable.

Coming to higher interest cost, given its just an increase of around a crore (although looks much more in ℅ terms) and a backdrop of demonetisation which would have affected its domestic customers in recovery of dues from their end customers, I would like to see few more quarters before drawing any conclusions. The company has been issueing Commercial Papers to reduce their overall interest cost and repaying their long term loan.

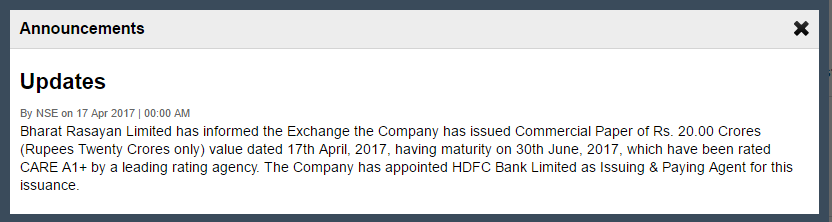

Commercial Paper (CP) is a short term money market instrument (maturity of less than one year) issued by companies to fund their working capital requirements. CP investors include banks, mutual funds, insurance companies etc. Bharat Rasayan Ltd is able to issue CP as it has highest short term rating of ‘A1+’. Most of the times, the interest rates of CPs are much lower compared to cash credit facility (used for funding working capital requirements) of banks. For eg, the current CP rates for an A1+ rated company should be below 8% while the interest rate for CP will be around 10%. High rated companies issue CP to reduce their cost of borrowing.

CP issue does not affect/dilute equity. In fact, it reduces interest cost which is good for majority as well as minority shareholders.

Thanks for the clarification

is annual result announced? if not when is it?

Fantastic result

EPS @ Rs 128.13 against Rs 79.74 for previous year

http://www.moneycontrol.com/stocks/reports/bharat-rasayan-limited-7505741.html

Good set of numbers, specially look better on a sudued Q4FY16

The cash flow is constrained with a 36% jump in YoY receivables, no large debt payments and poor dividend payouts. Working capital can be a dampner in an otherwise good story.

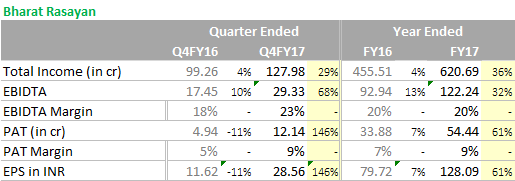

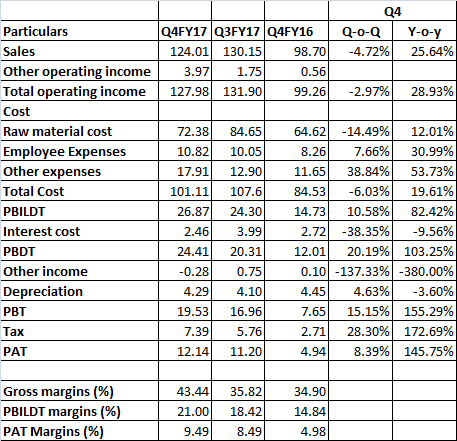

Good results by the company. Some pretty good indicators during the Q4 results as highlighted in the table below:

Apart from healthy growth in the topline, there has been a huge jump in gross and PBILDT margins on a y-o-y as well as q-o-q basis. The gross margins have crossed 40% for the first time in company’s history while its PBILDT margins crossed 20% and that too in a seasonally weak quarter for the company (Q3 and Q4 have always been weaker quarters for the company compared to Q1 and Q2). What is the reason for the such a huge jump in revenues for the full year as well as improvement in the margins is something we will have to understand from the management (that’s possible only in the AGM as that is the only time management speaks). Has the company bagged few contract manufacturing orders for innovator molecules of global agrochem companies? - That is something which only management can tell us!

Agree with @Prdnt_investor on the point of working capital. But they haven’t taken much debt for funding the same and it has been majorly funded through internal accruals. The trajectory of the working capital has to be watched in the coming quarters.

Guys… I went through their last 1 years announcements on NSE and found their fundraising pattern. Last year they raised one shot 25 Cr in May upto Nov… this has increased to 50 cr this year… sicne these are short term funds … safe to assume they are working capital loans… now when working cpaital increased so significantly there may be one reason which is higher production happening. Please look at the attached image. Value is the amount of fund raised in Crore. From and To date are the duration of fund raised. In fact for the june month second half… working capital fund raised increased to 60 cr.

Other way to look at it is that they have reduced debt significantly in FY17, now that the debt is under control they are not looking to aggrevively reduce it further but instead take the required capital from equity.

Can a company restructure debt midway to pay lesser principle per month going forward without adding more debt?

The company has been raising short term funds through commercial papers with maturity of around 3 - 6 months. These are mostly used to reduce the interest rate as CP has lower interest rate compared to working capital bank borrowings. All these funds raised through CP should also be adjusted for the amount repaid as mentioned in their announcements. Furthermore, these are also reflected in the short term borrowings on the balance sheet.