A very good and timely update on the company. Few observations:

-Falling debt levels and reduction in unsecured loans given by the promoters, which is expected to further reduce.

-Few large customers like Syngenta and Sumitomo, contribute to both the domestic and export pie of BRL.

-As per the news article in June 2020, there was a proposed ban on 27 pesticides which are

likely to “involve risk to human beings and animals, however, as it was a draft order, no pesticide mentioned in the order has been banned as of now. As per the management, BRL deals only with Pendimethalin out of the 27 insecticides proposed to be banned by the government which contributed around 2% to the total operating income of BRL during FY18-FY20 (FY18: Rs18.03 crore, FY19: Rs 20 crore, FY20: Rs 24.70 crore).

Generally, a buyback is initiated due to 3 key primary reasons as below:

When a cash rich company lack growth opportunities in the short-term.

When the management believes stock is underrated by the markets - post buyback, reduction in outstanding shares boost the EPS.

Tax effective way to reward shareholders - Unlike dividend income, gains from buybacks are not taxable in the hands of shareholders, encouraging companies to go for buybacks.

Note: During buybacks, it is important to study buybacks details i.e at what price buyback is coming and whether management is participating or not.

When the management exhaust full buyback limit, it does not amount to any impact on promoter shareholding.

I think its going to be 3rd as reason for BR. It is likely that buyback would not be at any premium and would be the value as per SEBI rules (last 30 day average, if I remember correctly).

I do not think it is the rule. Many companies have come out with Buy Back offers (tender route) with much higher price than the average of past 30 days . Recent examples being Cosmo Films @ Rs 576 whereas the 30 days average price is around Rs 420 and Garware Fibre at Rs 2300 whereas the average was around 2100.

Even if the buyback happens for 10% of shares, and promoters did not participate - still, the promoter share increases to 81%, as the total number of shares reduces. I guess buyback size will be much smaller or Promoters share increases and then after some time the of-load it via OFS (Offer for Sale).

I recently started tracking the company. While everything looks great in terms of growth and execution, there are 2 things I could not understand.

What is the source of funds utilized for buyback? The buyback document says that company is returning excess cash to shareholders but where is the excess cash? The balance sheet doesn’t seems have adequate investment/cash to fund it.

Why do a buyback in the first place. The company has approx Rs. 300 cr of capex lined up (200 cr for dahej and 100cr for Nissan JV)

What cud be the Acceptance Ratio at Bharat Rasayan n how is fy 22 performance expected to be? Did anyone attended this year Agm n can post minutes as it was done in virtual mode n many investors missed out.

Good correction from top. BR seems to be coming in buying range as tailwinds for contract manfg with Japanese cos is a huge achievement n opp size multiplies n may lead to hockey stick kind of growth

Looking on the sales data 15% YoY and margin never squeezed. Also looking for clarity on recent buyback & capital structure after that. So far it is good and heading to BUY range.

What is the source of funds utilized for buyback? The buyback document says that company is returning excess cash to shareholders but where is the excess cash? The balance sheet doesn’t seems have adequate investment/cash to fund it.

ANS: as per the buyback letter : funds from internal accruals

Why do a buyback in the first place. The company has approx Rs. 300 cr of capex lined up (200 cr for dahej and 100cr for Nissan JV)

ANS: as per the buyback letter : SECTION 8. NECESSITY OF THE BUYBACK

“the Company to return surplus funds to the Equity Shareholders, which are over and above its ordinary capital requirements and in excess of any current investment plans, in an expedient, effective and cost-efficient manner”

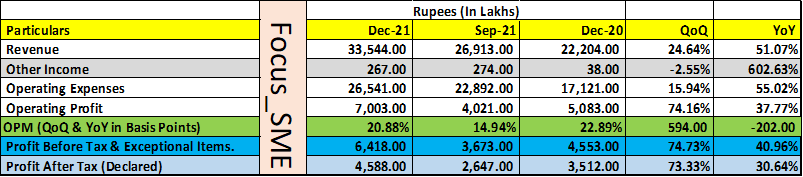

Excellent Results … Best ever quarterly revenue. I am unable to get any details on potential impact on revenues due to fire. Does any one have any info ?

The cashflow situation is worsened with both receivable days and inventory increasing. Inventory increasing is understandable as company might have increased inventory to protect itself from RM inflation and also as I understand cant book revenues if the cargo is in transit for exports (situation worsened due to backlog of cargo ships). But the increase in receivable days is a concern (probably I am reading too much into it) but it has reduced their cash balance. Hopefully it normalizes soon.

Co informed that the unfortunate fire incident impacted only 1 block. Overal 8 blocks are there & capex also on. Co is fully insured including for loss of profits.

Our bet is on mgmt. Sure they will find a way out. Think this was the first fire incident after getting listed in Dec 92. Hopefully good learnings.

Opp size remains huge for contract manufacturing specially for Japanese MNCs. BR well placed to grab it.

Co expanding at other locations reducing the single location risk.

Discl- Invested since last 6-7 years and averaged on upside.