To be able to understand what a company like Bharat Electronics Ltd. (BEL) does, we need to understand how wars are fought . Modern day warfare is almost entirely different from how some of the most destructive wars like WW2 were fought. Traditional warfare is considered to be platform-centric while modern day warfare is considered to be network-centric . The key difference between the two is the role technology plays in the linkage between decision-makers, sensors and shooters . Information about the current status of war used to get relayed to the command centre thousands of miles away from the battlefield remarkably slowly. This drawback of the platform-centric warfare caused what is known as “fog of war” for key decision makers as situational awareness considerably deteriorated when the battle was underway.

But in the 90s communication technology significantly improved and a new method called network-centric warfare came about in the US. The Indian army is rapidly adopting this now. Today, an entire group of people working for the Indian army called Signals corps handle military communications. What do they do? They work to achieve information superiority over the enemy so that the forces can function effectively . Within 45 minutes, they can set up an entire private communication network at any location in order to facilitate information transfer between the radars, sensors, shooters and command centre. There’s more! They can interject and jam the enemy’s communication network. The electronic warfare unit of the Signals corps can also use this network to generate killer microwaves at specific frequencies to disable electronics on the enemy’s electronic weapons & monitoring devices – like drones! And the best part of it all - None of this is science fiction!

More and more technology, software and electronic systems are being deployed in modern day wars. And Bharat Electronics Ltd., is at the forefront of developing and manufacturing such systems for the Indian armed forces and friends of India . They work together with the Defence research and development organisation (DRDO) and the others in this field like Hindustan Aeronautics Ltd. (HAL), to develop state of the art weaponry. Over 82% of their revenue came from the ministry of defence in FY2020.

But thanks to their expertise in electronics, they are called in to help with some other stuff too like helping out ISRO with their space gadgets, smart cities with their command & control centres, the police service to modernise their kit, metro train operators with automatic payment tills, election commission with the voting machines and best of all, by ministry of health to make ventilators! All of this put together however was only 18% of their revenue in the last FY.

What is their total addressable market size? Is it going to grow?

Warfare is expensive. Consider this for a moment – A staggering sum of Rs.4.7 Lakhs Crore (About $63B) was allocated to the ministry of defence in the FY21 budget. To put that into perspective, the ministry of housing and urban poverty alleviation received LESS than 10% of that amount. This infographic below shows you a back-of-the-envelop calculation on how big this business is today in 2020 and how big it can really be in 10 years from now.

Now that we know what they do, how well do they do it?

Turns out, they do it quite well! BEL has consistently ranked as one of the top 100 defence companies worldwide. The only other defence company from India which finds mention in this list is Hindustan Aeronautics Ltd. (HAL).

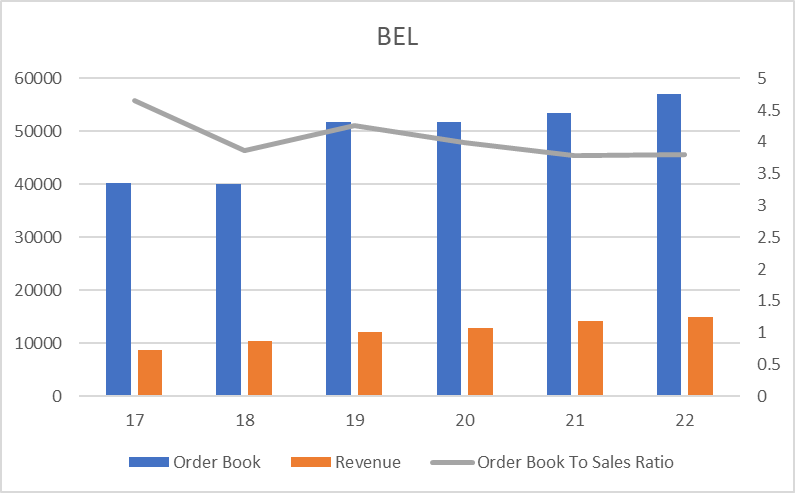

Here is how their revenue and net profits grew over the last 10 years.

They have ZERO debt in their books , and they have consistently paid dividends. Look at their dividend yield over the last 10 years.

The issue with most PSUs is that they are generally less well-run, and less efficient compared to the private sector. So, I calculated a few efficiency indicators from their financial statements for FY20 and compared it with Escorts Ltd., another business I was looking at last week

All of the efficiency metrics are indicating that BEL is an extremely well-run business in today’s context. But why does the stock sell at a much lower PE in the stock market compared to the others? What are we missing?

Before we answer that, let’s answer another question. Who owns BEL?

BEL is one of the 14 Navratna public sector enterprises and is a public sector undertaking (PSU). The government of India owns 51% of the business while mutual funds and retail investors hold the rest of the 49%. But it wasn’t always like this. Only 10 years ago, the government owned a meaty 76% of the company while the public owned the rest. Over the years since then, the government kept selling stocks in the company to outside investors to raise money. Now, why would the government dump stocks of a business that is both strategically important and quite profitable?

Why would they kill the goose that lays golden eggs?

The answer to that question lies in this chart below.

Each year the ministry of defence signs a number of contracts for delivery of weapons over the next years. When the deliveries are made, payments become due. These are called committed liabilities . Any other contracts they sign for weapons delivery are called new schemes. The finance ministry over the last 4 years has not even allocated enough money to meet the committed liabilities of the defence ministry. The standing committee of Defence in 2019 wrote in their report that there is a very real risk that the ministry might end up defaulting on their payment obligations to the vendors.

The finance ministry is like a parent to a number of children (ministries). It has only finite amount of money and all the children want more than what they can have.

But the defence ministry has already committed to its suppliers to buy these weapons. When it is time to pay, what could the defence ministry do without actually defaulting on its payment? – Really simple, ask the vendors to come back after some time. And that’s what has been happening.

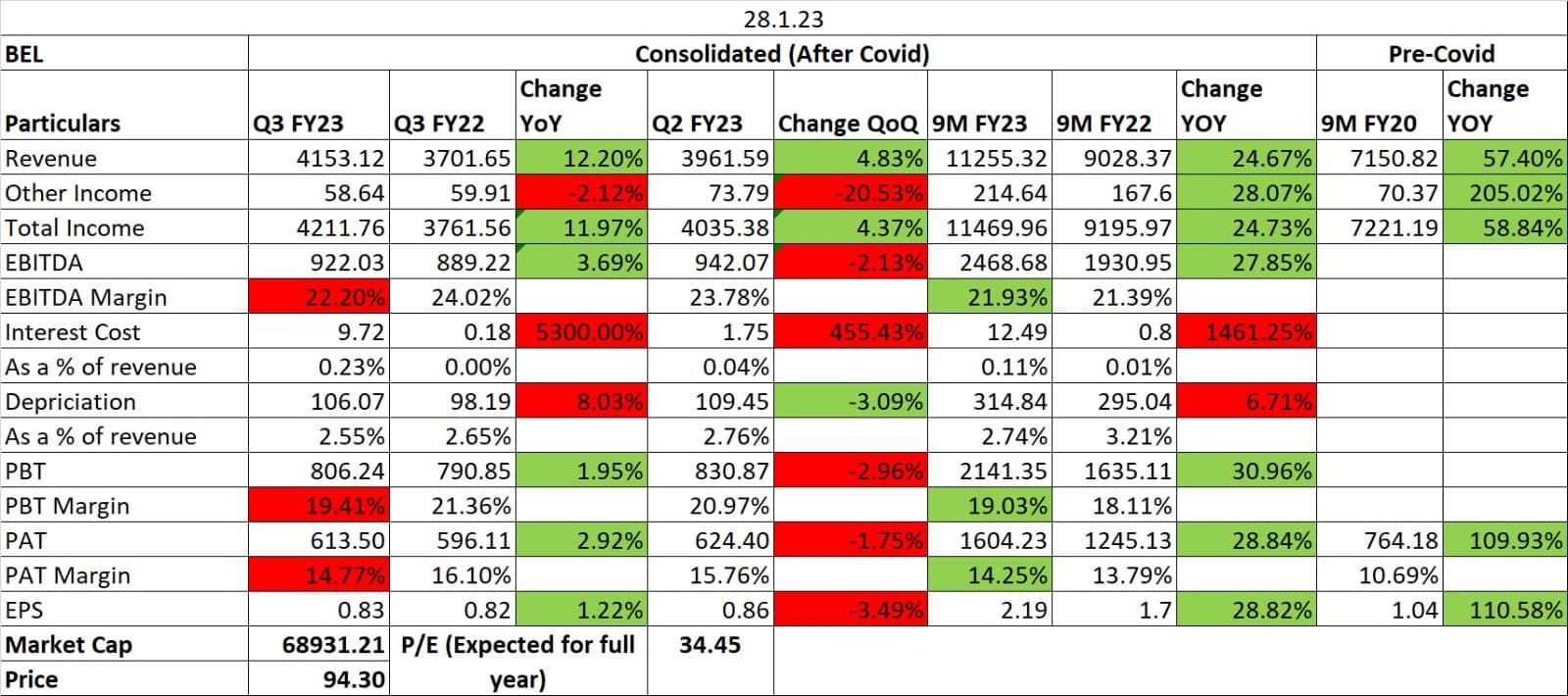

In the case of BEL, receivables from the ministry went up from Rs.3800 crores in 2015 to Rs.11,000 crores in 2020! (This includes something called ‘contract assets’ on their balance sheet, which is also payment due from the customers - possibly performance-linked, but it’s not clear from the AR) An increase of 190% in a period when revenues only went up 80%. Is it just with BEL? Nope! Take the case of HAL – Receivables from the government went up from Rs.5,000 crores in March 2016 to an astonishing Rs.19,000 crores in March 2020(this figure also includes contract assets). But the government anyway owns these companies. The left pocket owes money to the right pocket. What is the big deal with it? – That argument is only partially true. Mutual funds, LIC and the public own 49% of BEL and 10% of HAL. In effect, the money that would otherwise have been distributed to the shareholders as dividends is now being used to extend credit.

Here is my reading of the situation

The government is hitting the exit button on these defence stocks to raise the cash it desperately needs (Mazagon dock, another defence company went out public earlier this month). The downside of this is that any dividend paid in the future by these companies has to be shared with the new minority shareholders. But the government needs this dividend from its best performing PSUs. So how does it come around it? By extending massive amounts of credit to itself from these PSUs! In a roundabout way, shareholders in these companies are funding a portion of the excess spending of the ministry of defence.

Conclusion

The defence industry in India is going to do quite well over the next decade. Make-in-India push is going to positively influence the development of this industry. There is no denying that. Save for some small corruption cases here & there and the RTI activists giving it a hard time now & again, BEL is a well-managed business at the leading edge of its industry. It is efficient, profitable and keeps innovating through R&D & industry partnerships. It is a good business to own, on any day. For someone looking to build a portfolio of value stocks, with stable names that offer reasonable dividends, capital protection and maybe even some upside from growth, this could be considered a good addition at current prices.

But for someone like me who is twitchy about the idea of indirectly funding the government of India or is looking to build a portfolio of the next FANG (Facebook/Amazon/Netflix/Google) stocks of India, or perhaps even against weapon manufacturing, there are other opportunities.

Disclaimer - I do not hold any position in BEL’s stocks. I am not a SEBI registered advisor and this is not a buy or sell recommendation for the stock. Please consult with your financial advisor before investing.