A comprehensive coverage on BEL by ICICI Securities - Report dated 21st June 2023

https://alphadefense.in/bel-on-roll/

https://alphadefense.in/bel-on-roll/

https://cashlo24.com/bharat-electronics-bel-share-got-1701-crore-huge-order/

I just listened earnings con call … surprised to see interest from all major DII / MF fund managers…lot of them participated ![]()

![]() Management and execution power of PSU now a days are really surprising…it will be gross mistake for not investing by having old days image of PSU.

Management and execution power of PSU now a days are really surprising…it will be gross mistake for not investing by having old days image of PSU.

PSU having excellent assets and talent and now they have progressive and decisive government backup…many already multi baggers

Invested in BEL @ avg buy 41 rupees and BDL @ 350 level

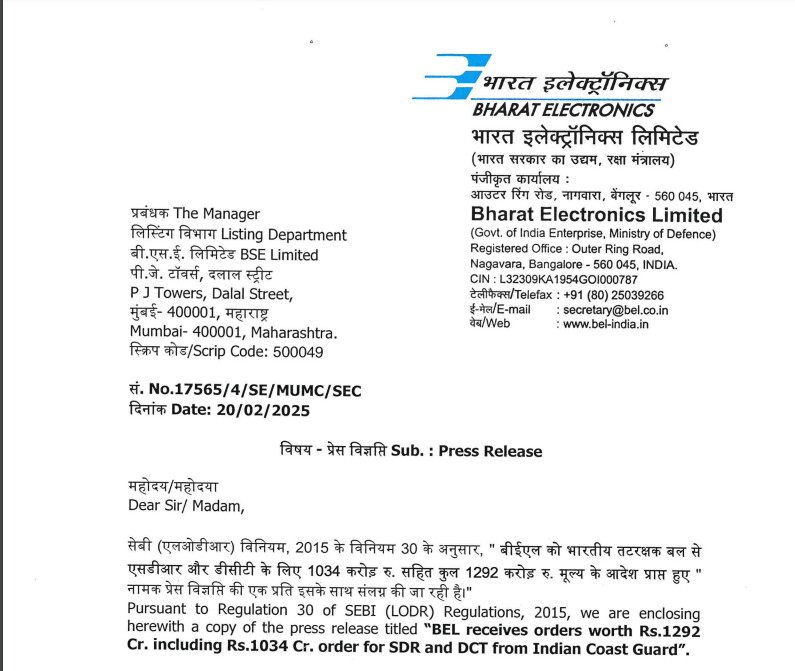

https://www.bseindia.com/xml-data/corpfiling/AttachLive/228ac18e-d7d5-4f3e-9ae3-740d4a74707f.pdf

good set of results from Bharat electronics, Rs 0.80 final dividend.

Disc. Invested

Summary of confcall from mgmt in closing comments:

healthy orderbook pipeline including some big ticket items (QRSAM Fy25-26 etc), focus on high value products to help in margin expansion.

Disc: Invested

Company profile: BEL is a leading aerospace and defense electronics company and primarily manufactures advanced electronic products such as radar missile systems, electronic warfare and avionics, anti-submarine warfare, etc.

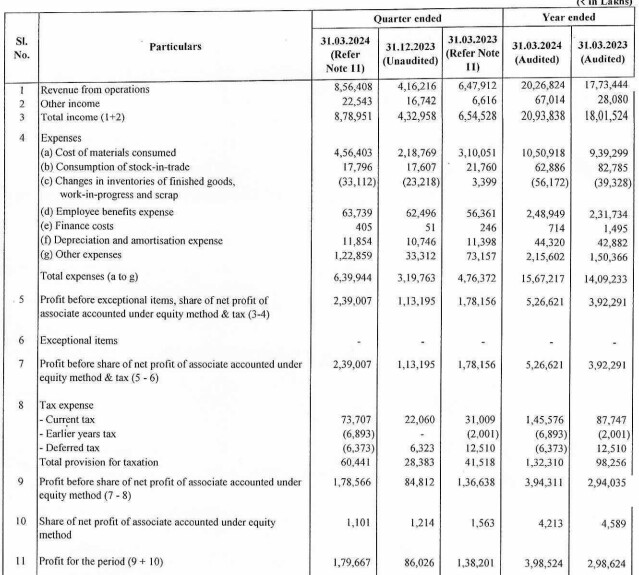

Q1 FY25 results: The company’s revenues stood at Rs 4,105 crores, up 19.10% YoY. EBITDA stood at Rs 948 crores, up 40% YoY. EBITDA margins stood at 22% versus 19% YoY. PAT stood at Rs 776 crores, up 46.2% YoY aided by higher other income. Revenues were aided by the pick-up in execution of the LRSAM order as supply chain disruption to the ongoing conflict in Israel eased in the current quarter. On a QoQ basis, revenue declined 50.4% and EBITDA margin contracted 400 bps as Q4 is the strongest quarter.

Order book: The company’s order book stood at Rs 76,705 crores versus 75,934 crores QoQ. The company received orders worth Rs 5,000 crores in Q1 FY25, down 39% YoY due to the elections. Ordering activity however picked up in July’24. Around 10% of the company’s current order book depends on supply of raw materials from Israel.

Management commentary: Here is the management commentary post Q1 FY25 results:

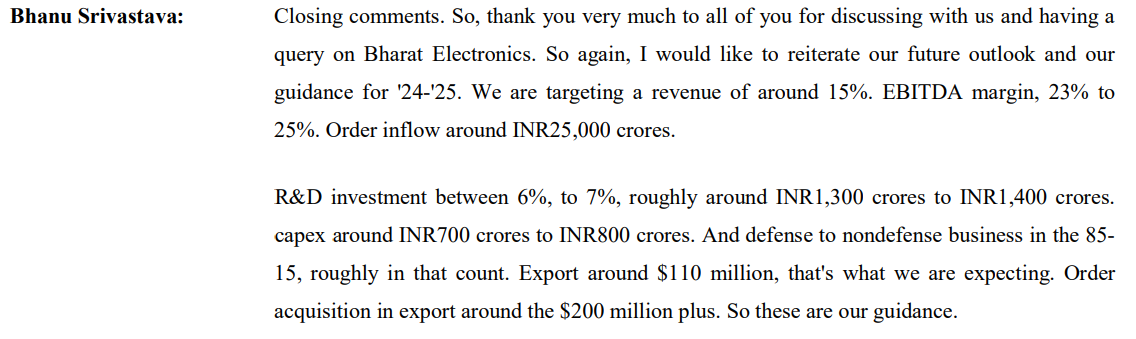

The management has retained its earlier guidance of 15% revenue growth along with an EBITDA margin guidance of 23-25% along with order inflows of Rs 25,000 crores. This indicates a pickup in margins and execution in the coming quarters.

Currently, 80% of the company’s order book are nomination contracts. Margins on these contracts are 7.5% and BEL enjoys a 12.5% spread over these margins due to cost control and operating efficiencies.

The company has indicated five programs each worth Rs 1000 crores which will be the key to order inflows in FY25.

In FY26, the company expects Rs 50,000 crore of order inflows led by the Rs 25,000 crore QRSAM order and multiple base orders, which includes MRSAM and HAL’s planned Sukhoi fleet upgrade. The QRSAM order is expected to be placed by Q1 FY26.

Non-defense contribution stood at 16% in Q1 FY25 versus 19% in FY24 due to the contribution of EVM and VVPAT machines.

The company has planned an annual capex of Rs 700-800 crores for the next 3-4 years for modernizing its facilities and capacity expansion.

Other expenses increased by 30% YoY on account of higher liquidated damage provisions.

In the non-defense segment, the KAVACH system is also expected to be a big opportunity for the company.

The share of defense electronics spending on the total electronics spending is on a rise and BEL will be the beneficiary of the government’s indigenization focus.

BEL or BHEL?

Disc: Holding since 2008. Makes good part of portfolio.

Sorry, it’s BEL. Edited

bel updates.pdf (828.5 KB)

BEL | Q3 CONCALL

a. Achieved 11,000 Cr Orders Vs Guidance Of 25,000 Cr

b. Confident Of Achieving ₹25,000 Cr For This Financial Year