Where is the money going ?

Beside good result, good return ratio ,good FCF, to whom company is giving loan with increasing intensity?

This is from half-yearly result ending 30th Sept 2021, consolidated cash flow statement

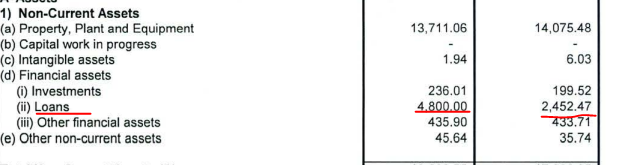

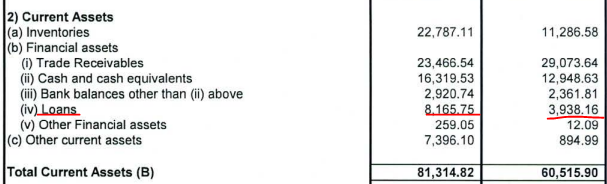

Consolidated Balance sheet

As I don’t know the reason of this ,awestruck by the amount of money flowing out of company…

This is certainly not a Related party transaction ,nothing mentioned on 9th May/latest submission to exchange.

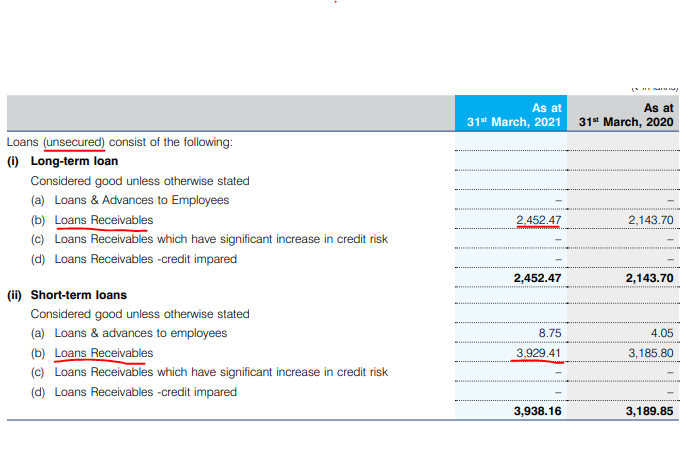

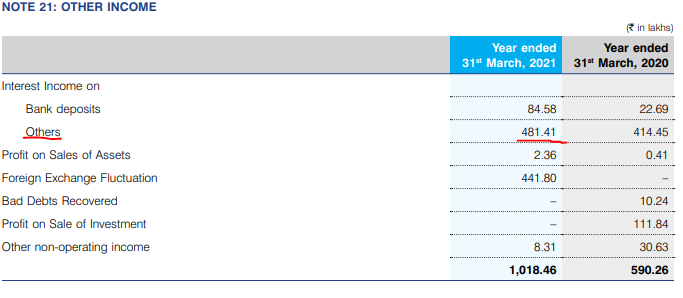

FY21 Annual Report does not disclose anything about the nature of the loan given, credit worthiness of the receiver,% interest yield from loan tendered. Only below disclosure

I have also raised these questions it to the investor relation contact person Mr Ashwin Patel on the email ID given. Let us see whether they respond. I also find it strange why almost Rs 129 crores is being given as loan and to whom it is given and for what purpose. Is it interest bearing or not ?

Ineos Styrolution’s OFS to reduce its stake from 75% to 50% (at 25% discount to yesterday’s price) can be a very good news for BEPL. Ineos first tried to delist the company but when they become unsuccessful, now parent company has decided to reduced their stake. From the discount offered, it seems they are in hurry. This stake reduction seems like part of larger plan (probable exit in years to come?) which also means Ineos would be doing any new investment in India. This will directly benefit BEPL IMHO

Disclosure - taken tracking position post Ineos OFS news

In Board Meeting ,the Board announced that the Overall ABS Manufacturing Capacity of BEPL have expanded from 65000 TPA to 75000 TPA by obtaining all necessary clearances from States and Statutory authorities even without incurring any additional capex. This should result in good sales growth in forthcoming quarters. I foresee solid surge in share price of BEPL.

I was looking at the numbers and other information cursorily. What I noticed was that till March 2020 this business was having EBITDA of 6-12% (quite volatile). The spike came in FY 21 and currently continuing with EBITDA of 30-35%, though normalizing now . Due to this , this seems like a commodity business and they are acting more like converters of SFG to final product being supplied (They import the Acrylonitrile monomers ). Therefore the question is , Is there anything which changed in the last 2 years which should allow them higher margins? Otherwise this margin jump is purely cyclical and opportunistic.

If I take the normalized margin of 10-15% , then assuming topline remaining constant , it is still at 15 times EBITDA which to me is very fair.

Regards

Nikhil

Disc: Not invested; Looked only cursorily. No indepth knowledge of the business so pls take the comments with pinches of salt

I had tracked the company earlier and the management appeared shady to me(personal view). No investor presentation, not many interviews available on the internet regarding future plans and direction and huge fluctuations in results make the company almost unpredictable.

Disc: Had Invested, No Holdings rn.

This was because the rates of ABS shot up considerably. You can read the Concalls of Ineos to understand the sudden burst of revenues due to that and credit to their management for acknowledging that this wont last forever. Tracked, but passed on after reading thier view.

BEPL uses crude oil as their main raw material. The price fluctuation of crude affects the OPM badly last one year. Crude price were 20 year low in FY21 and it helped the margin to shoot up. Now it is at 2014 levels which clearly affects the results of this quarter. I think, this trend is expected to be continued because the current OPM is also way higher than the historical Material cost consumption. Unless, sales does exceptionally well in the future quarters, will not see BEPL to go up.

I am closely observing this company from past one year,

Some times the results and data is not that much accurate. Its always tricky.

Folks, Anyone having any information on this below.

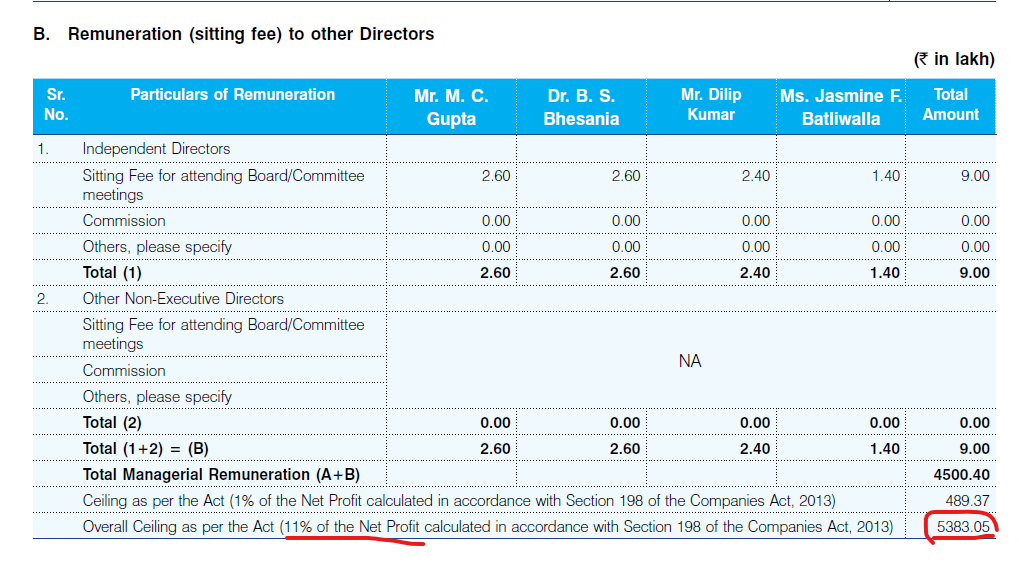

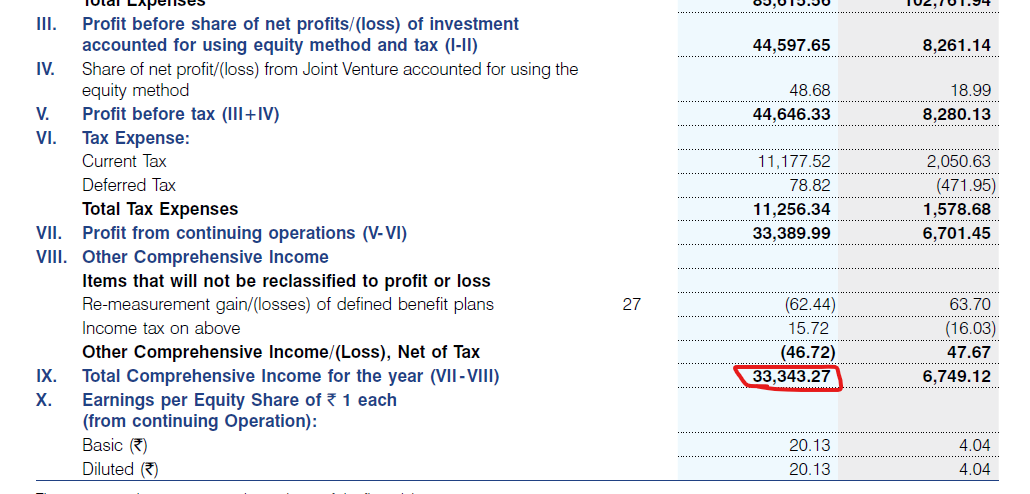

BEPL seemed to be undervalued. But when I looked into its Annual Report FY22, I could not understand its Managerial Remuneration activities. I found that according to the Company Act 2013, the Overall Ceiling of Managerial Remuneration is 11% of the Net Profit which in my calculation = 11% of ₹ 33,343.27 =₹ 3,667.75 lakh. While the reported number is ₹ 5,383.05 lakh. Please reply if my understanding is wrong.