Bhansali Engineering is the only Indian promoter led Co. manufacturing ABS & SAN resins in the country. The Co. completed its first phase of expansion in March 2016 augmenting its installed capacity from 51KTPA to 80 KTPA. ABS resins are used mainly in the Consumer Electronics, Appliances & the Automobiles sectors. Almost all refrigerator manufacturers are likely to shift from HIPS to ABS thereby creating further demand for ABS. Talking of demand, domestic production is unable to meet demand & this unmet demand is taken care of through imports. In this backdrop, the Co. is looking to further increase capacity to 200 KTPA at a port based facility.

The Co. has also entered into a JV with Japanese Co., Nippon A&L Inc. The focus of this JV is on the automobile sector and it has already started manufacturing the entire range of value added products from the Nippon stable. This JV should start contributing to the numbers in the current financial year, though how much would only be known when the full year results are declared, though the mgt. sounds quite bullish in the annual report.

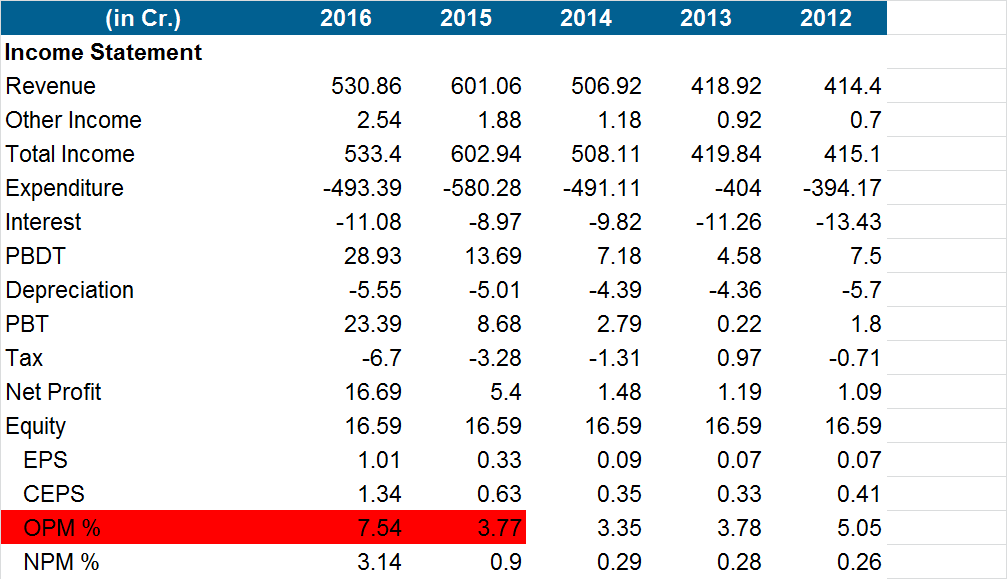

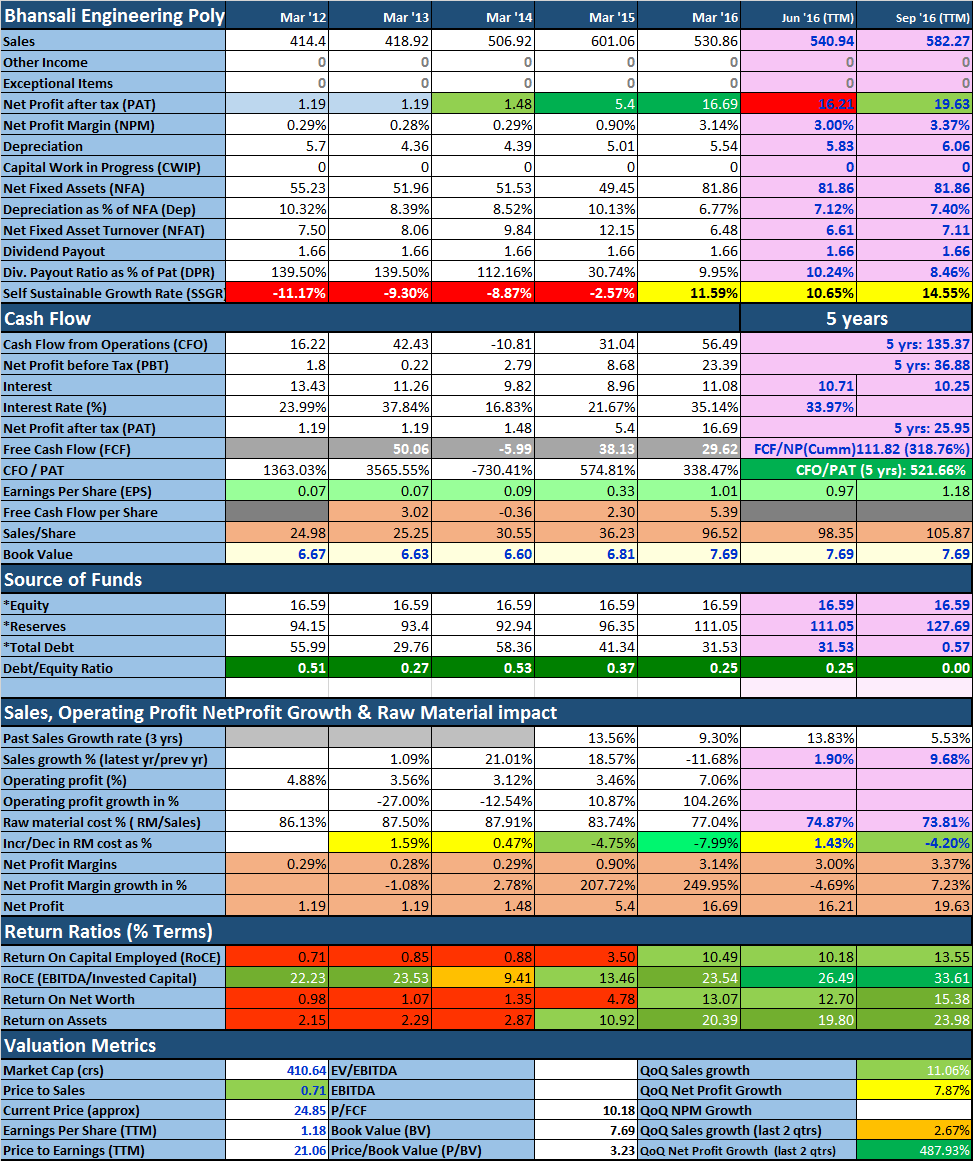

Based on the first half of the year of the current year 16-17, the Co. (Stand Alone) in the normal course should have done SALES, EBIT & PAT of about 700 crs, 55 crs & 33crs, which would have been a profit growth of about 100% over the previous year 15-16 of 16.69 crs, which itself was a jump of over 200% over 14-15 of 5.4 crs, but now one may have to factor in the effects of de-monetization, which is a bit of an unknown.

What I found really impressive is the constant improvement in the operating margins over the last several qtrs., from 3.77% in 14-15, to 7.54% in 15-16 to 8.31% in the first half of the current year. The September quarter saw the Co. become pretty much debt free, having repaid about 31Crs. of short term debt. Debt repayment has also meant that the ROCE for 16-17 could be as high as 35%! These numbers are for the standalone entity & could get a further fillip from the profits of the JV with Nippon. The whole business is available at an enterprise value of about 390 crores and appears to be undervalued.

The domestic demand for ABS resins is growing @ 15% per annum so the opportunity size is huge. In addition to the recent expansion to 80 KTPA, the Co. has also initiated modernization / debottlenecking of its plant to make the most of this demand supply mismatch, but the long term success of the Co. would also be dependent on its ability to further scale up its operations.

A key concern here is the high cost of raw material constituting between 75 to 80% of sales. Volatility in the price of crude could affect the performance of the Co. So would a fall in the value of the rupee affect the imported cost of raw materials & would also be a negative. That said, these concerns are applicable to the industry as a whole & are not limited to the Co. Another concern is about the issue of pledged shares, when the Co. itself is debt free. Perhaps a legacy of its troubled past, but we will need to be mindful of & try to seek clarity on.

Sir I have a few questions

a) Any reason why the OP margins have gone up?

b) Raw mat cost is very high as compared to sales so it looks like a commodity business. Wabco supplies ABS to trucks so I am assuming that they must be their major customers. Pricing power ?

c) I heard that NIppon also have a lot of JV’s in India.Any idea what products Bhansali Engg will make and what is the market size of those products?

The company surely looks interesting but it’s chart makes it look like a typical pump and dump stock.

Waiting for your inputs

Thanks Rajeev for starting this thread. Here is some data collected from various sources

COMPANY :

BEPL is a vertically integrated petrochemical company that Manufacturs ABS which acts as a raw material for leading companies dealing in automobiles, home appliances, telecommunications, luggage, bus body and various other applications.

With Joint Venture (50:50) front with Nippon A & L, Inc, Japan, a Sumitomo Group Company, company has started production of latest grades like ASA, AES, Transparent ABS and alloys like ABS PMMA and ABS PC enabling the company to have entire range of “product basket” for catering the pervasive requirement of clients and actively contribute towards import substitution.

Company has established state of the art research and development center at its Abu Road Plant, Ahmedabad. Nippon A&L Inc is a specialized company focusing on polymerization of styrenics and enjoys high reputation in the field of manufacturing and marketing of ABS, AES, ASA resins and SBR/PBR Latices.

Customers list

Auto:Bajaj Auto , Hero Motocorp,TVS Motor.

Appliances: LG Electronics ,Samsung India ,Whirlpool Of India,

Electrical:Anchor Electricals, Havells India ,Larsen & Toubro etc.

There are handful of manufacturing companies in India which produce ABS and are not able to cater to the whole demand of ABS in India, so the deficit in supply is fulfilled through imports.

Key players:

Some of the key players in market are DSM engineering plastics, BASF India, Bhansali Engineering Polymers, Styrolution India and now Kingfa

Demand and Outlook :

The global carbon fibre reinforced plastic (CFRP) market is expected to reach $ 27.98 billion by 2024 from $ 11.6 billion in 2015, according to a new report by Grand View Research Inc (GVR). Increasing composites demand in the automotive industry is expected to remain a key driving factor for global CFRP market. Automotive is the fastest growing segment of carbon fibre reinforced plastic market with a market share of 19.7 percent of the total volume in 2015.

Government initiatives including ‘Make in India’ to encourage domestic engineering industries including electronics, construction material and automotive is projected to propel the demand for thermoplastic elastomers (TPE) in the country. Asia Pacific thermoplastic elastomers market is estimated to reach over $ 7.82 billion in 2022 from $ 4.63 billion in 2014 due to growing consumption from auto part production. And India is expected to witness the highest growth of over 5.6 percent between 2015-2022.

Market is to witness significant growth over the next seven years owing to increasing automotive production and most automotive OEMs have been replacing metal and alloys with plastics from manufacturing of vehicle components to make vehicles light weight, thus propelling demand for TPE.Demand for ABS market during F.Y 2014-15 was 205000 TPA which increased to 235000 TPA during 2015-16 registering a growth of around 15%.

Future :

To meet ever growing demand in Automative and Home Applicances first phase of expansion has been completed in the month of Mar-16 with the installed capacity of company from 51KTPA to 80 KTPA. Further expansion of 120 KTPA is proposed at some port based location with a view to save a lot on transportational expenses by March 2019 will take total capacity to 200 KTPA.Requisite project work has already commenced

Financial :

Debt/Equity is 0.2, Interest Cover is 3.1 Cash reserve about 11+ Cr, Its operates with handsome ROCE=21%+, ROIC=22%+, MCAP/Sales=0.7.

Its Fixed Asset turn over has constantly on upswing from 1.42 to 2.29 over three years, Another interesting data itself receivable days is about 85 days far less than payables days of about 120 days…shows its operational and cost efficiency combined with superior realisation of its product. It capacity expansion from 51 to 200 KTPA will mostly through internal accruals and small debt show capital management by firm…

Management :

Mr. Babulal M. Bhansali, Promoter and MD of the Company, is a first generation entrepreneur and a visionary leader in the business arena of ABS & SAN Polymers

Rational:

• One of the leading producer of ABS and SAN in India and with tie up Nippon completes entire spectrum of product offering in Thermoplatic elastomers

• With capacity expansion on 60% i.e. 80KTPA and further 250% expansion of 200 KTPA by March 19, would enable to give impressive growth for next few years

• Company has also to maintain its current status of being a long term debt free company

• It claim to be one of the lowest cost ABS manufacturers as its per KG power consumption manpower cost and overhead expenses are one of the lowest globally

• In 2015-2016, Promoters enhance stake by 1.33% with total stake 51.5% in SEP 2017 promoters further scooped by about 9 lac shares from open market

• Zero Debt company.MCAP/SALES of just 0.7 (FY17) with expected revenue growth of 18%, Profit growth of 48%…A bet not to be miss Included 30% expansion in FY17 and full expansion of 60% in FY18 revenue. NPM is expected to be range of 5.5 to 6%. Mega expansion of 120 KTPA will take company in next orbit from FY19.

In FY 16/17/18 company is likely to post a revenue of 530/700/870 Cr (18% CAGR) and register Net profit of 16.69, 38.50 and 52 Cr (48% CAGR), giving EPS for Rs. 1.00 for FY16, Rs. 2.30 for FY17 and Rs. 3.15 for FY18.

Included 30% expansion in FY17 and full expansion of 60% in FY18 revenue. NPM expected to be in the range of 5.5% to 6%.

Mega expansion of 120 KTPA will take company in next orbit from FY19.

Is the order book always full Yes. As soon as the plant is operational they get the orders

New expansion of 120 KTPA near a port. Has this been finalized? Still look out for ports is ongoing

Capex cost and how is it funded? The CS didn’t know the amount but expected it to be around 800 cr

Any debt raising plans? Plan to use internal Accruals only. (I can’t see so much accruals to fund this expansion)

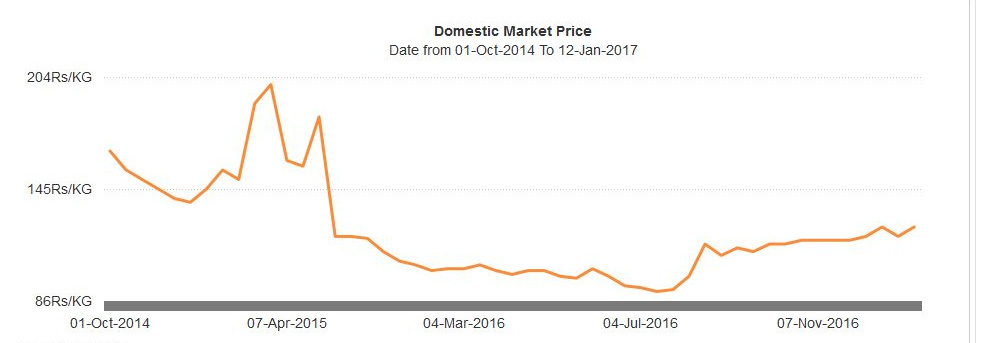

Earnings in Q1 Fy16 were high while other quarters were bad. Why? Is there any seasonality to demand? Profit is subject to Crude price and Rupee per dollar. The provision for tax for the whole year is done only in Q4. So Q4 will always have lower profits (Now it seems that they are paying Taxes every quarter. So this year must see good Q3 and Q4)

Notes: Butadiene price is linked to crude price. Will add more details on this soon.

Margins are low at around 10% ebidta! could this increase? Company is in the process to improve this by Automation of packaging. Currently transport cost of imported goods is very high. He mentioned 7 rupees per Kg as transport cost. Once they have a plant near the port, expect margins to go up.(Even though transport cost amounts to very less when compared to raw material cost!)

Transcript from AR 16.

Styrolutions, Kingfa are big competitors. How do you fare against them? They consider Stryolution to be the only Active competitor in this space

Key Risks:

• Dollar strengthening

• Cost of Raw material is around 80% of the revenues.(Acrylonitrile and Butadiene are imported) It is a low margin commodity business.

Given that demonitization, has affected consumer discretionary the most and looking at the low car sales December numbers - wouldnt it be fair to assume that this company should continue to be affected for the next 2 quarters and utilisation rates should remain low and we should see inventory build up?

In that case, on a forward basis, the company trades at 16-20x earnings depending on varying estimates and for its size becomes expensive at current levels?

Interesting to see that the interest rate where on the higher side. Since company has repaid its debts so it is not an issue going forward. Secondly the interest paid previously which was as high as 11 crs will flow in to Net Profits from Q3 onward.

sir the promoters have found this a new gimmick to pump prices of shares…an example is waterbase where the promoters are continuously increasing stake…

This is only one parameter out of other “n” important parameters that should be considered before zeroing in on a particular stock

Fundamentals definitely are the single most important criteria; especially in turnaround cases ; Promoter buying from the open market give us retail investors a sense of confidence

I am not following waterbase;

In case of Bhansali , its financials have started improving and in 2016 ; Promoter buying of BEPL shares is “Market buying” and no off market deals; If at all their aim was to “Pump” up the share price they have not succeeded much since the price has gone from 15 levels at the beginning of 2016 to 24 now

I am assuming that the company doesn’t have any pricing power.

Disclaimer

This is definitely not a steady compounder kind of company. It appears to be undervalued at the moment. Thats probably the case we are making