Given that we are both invested in RACL, i think we will appreciate that not all cos point out R&D expense in a line item separately for R&D. See notes from July Concall

See FY22 AR snippet

I vaguely remember seeing this in Gufic too. In fact most indian cos ive seen are not very fussy about where to put true R&D expenses most just seem to fill it with “nil”. Now that Co is doing concalls, interested investors can always ask in Concall about level of R&D spends & headers where these occur.

Freight accounting is quite diverse from what I have seen. Many cos dont account since freight is borne by distributor or customer or retailer. Definitely an important question we can ask management in concall.

Definitely yes. Also see the purchase of stock in trade for BAL which is quite high.

This clearly shows that a large part of their revenue is based on purchases of off the shelf products (i assume at least AIs and potentially formulations as well). Another key question to ask management.

I think this one is relatively easier to answer. I have seen several instances where co does expenses for sub from parent P&L & vice versa. This is definitely not clean accounting but as long as Sub & parent are working towards same goals, id just analyse consol P&L and not break it down too much (unless i am confident of accounting hygiene)

Question to ask is whether and how much of these negatives are discounted by valuations.

To me personally, the biggest red flag is the cashflows which are non existent. Given their large push to B2C, the receivables specially are quite concerning. I do remember that BR had similar cashflow concerns and once cashflows came in, stock did quite well as investors confidence improved. A key monitorable IMO.

In short, im afraid investors cannot. Only management can. I encourage you & every other investor to join the public concall & ask these questions, i think that is best way to proceed.

On the positives side, one can definitely checkout http://ppqs.gov.in/ to confirm that indeed, co’s products are being approved by Govt. Eg: Consider http://ppqs.gov.in/sites/default/files/minutes_62nd_cib.pdf

MINUTES OF THE 62

nd MEETING OF THE CENTRAL INSECTICIDES BOARD

(CIB) HELD ON 09.05.2022 AT 1400 HRS THROUGH VIDEO CONFERENCING.

^ see last row, this is a triple combination formulation approved on 09.05.2022

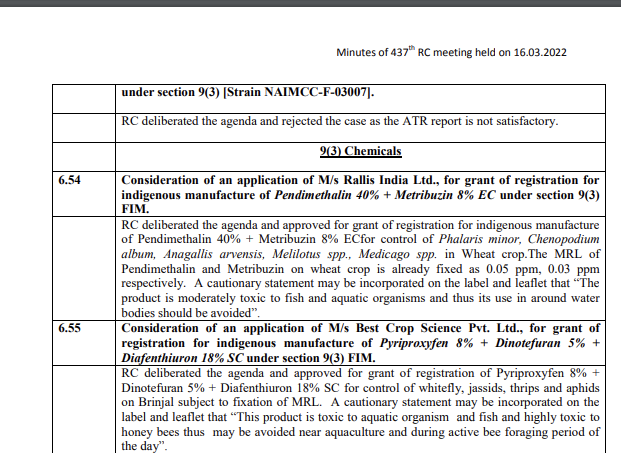

Also consider MINUTES OF THE 437th REGISTRATION COMMITTEE MEETING HELD ON 16.03.2022.

http://ppqs.gov.in/sites/default/files/437_rc_minutes.pdf

^ Approval of registration of Ronfen.

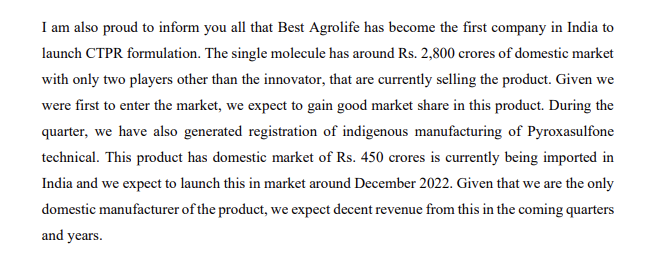

I think harsh’s notes while quite gooddo miss out on a few critical aspects of the investment one can derive from the concall. Most important is that co has a pipeline of 20 odd products which are similar in size & scope to Ronfen.

For clarity, this is 20% share of a 2800cr market. Thats 560cr just from CTPR. No domestic competition. 25% discount.

https://www.business-standard.com/content/press-releases-ani/best-agrolife-ltd-becomes-first-indian-company-to-launch-indigenously-manufactured-ctpr-122090300005_1.html

I think the accounting concerns are quite genuine, dont give much confidence. The risk of capital loss is high (what if co is outright fraud & all numbers are cooked up). This is why valuations are also quite poor. I do think it is worth diving deeper, because the upside is also asymmetric (if one can simply establish some confidence in co not being outright fraud).

I will try to visit their factory when i can (the one in Noida). Will try to attend their next concall too.

Disc: Small position of 2-3% only to be scaled up if higher confidence in accounting & cashflows can be established. To be exited if co seems to be indulging in outright fraud.