Stock trades at a P/E of 10.6x with no change in business profile

Stock trades at a P/E of 10.6x with no change in business profile

Yup Valuations are very cheap I’m doing SOPT valuation I found it reasonably undervalued from all perspective May be it’s just taking rest after huge run Up and it’s also due to huge target given by incred equities…

I have one question do you know what’s are the margins management are guiding for FY23?

For Whole segment and especially for Distillery segment and what’s their current margins for distillery?I just wanted to confirm

Ethanol /ENA is a higher margin biz compared to their oil biz , as capacity expansion is mainly into the former at a rapid pace we can see the OPM rise , management has indicated the current 12 to 13% margins for the distillery segment for the foreseeable future

their margins in distillery depend on government price/ ENA prices + DDGS.

DDGS price depends on soya meal and corn price. So linking margins to commodity…

It takes around 53.5 rs to make 1 litre of fuel grade ethanol (2.5 kg of FCI rice at 20/kg and 3.5 rs coal) and gov buys at 56 giving co op of 2.5 rs /L.

plus 1 L ethanol production yields 250 gm of DDGS which is priced 18/kg (4.5 rs /L of ethanol).

so final realisation is 56+4.5 ~ 61 rs and op is 7 rs/L. opm 13-16%.

commodities play some role here. remember such rice to ethanol cos rejected gov offer of 54/L, then gov revised price to 56/L ! Higher crude prices are also good for ethanol cos

coal ,corn prices have gone up as well in last few days significantly , so as the edible oil prices which they will benefit.

BCL IND Q3-22 PRESENTATION.pdf (3.0 MB)

BCL industries Declares 2 Rs of interim Dividend and promoter group waives it.

This has been done by the company twice.

It appears very kind gesture of promoters to leave off their share of dividend on the back of capex.

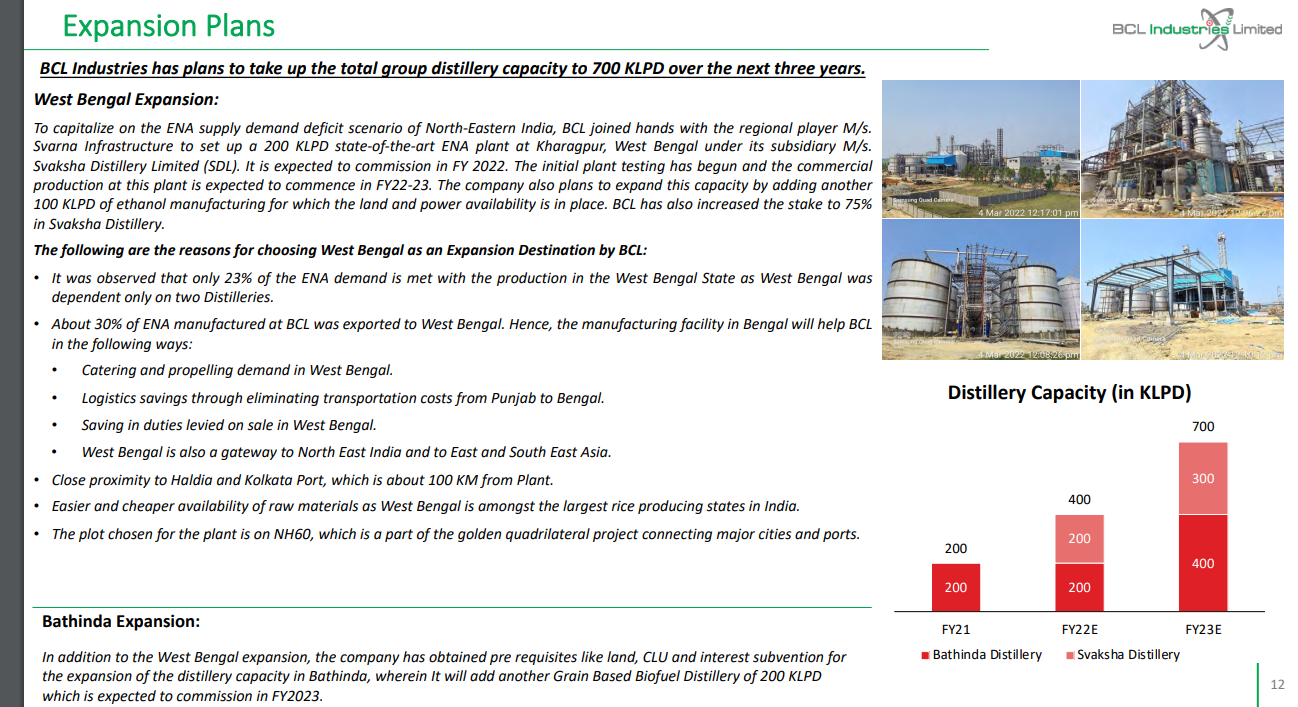

Also in the same board meeting, they confirmed that, their West Bengal unit will start commercial production within this month onwards.

Their Bathinda expansion is also on track.

Octane is a measure of petrol tendency to ignite under pressure. If it’s very low, the petrol/air mixture in an engine’s cylinders will burn too soon, creating damage knocking. The industry standard is 87.

But getting petrol’s octane rating up to that standard costs money. It means more refining of the petroleum, or using high-octane compounds in your petrol formula, such as ethanol. So Petroleum companies aren’t using ethanol for its energy — they’re buying it for its high octane rating. SO ethanol is going to gain only and not loose in the current petroleum powered engines era.

Now , IF EV replaces petrol /diesel vehicles, the whole green concept requires those batteries used by the said EV revolution powered by green power generated in the backend. SO solar, WInd, hydro if we totally avoid fossil fuels and then Ethanol has to come into the backend as power demand would be that huge… so going forward ethanol would be having gaining importance only, and wont loose importance.

Only issue with ethanaol production is we would be loosing food growing acres to produce ethanol rawmaterials… like sugarcane, corn etc…

Takeaways from group call with Kushal Mittal on March 14, 2022.

Is a play on import subsitution of edible oil and crude oil

Edible Oil Business

Grain-based Distillery

Guidance

What is the Consolidated margins company can achieve?

May be due to this?

BCL industries recevied only short term order from OMCS.

Not sure why BCL did not recevied long term order even with capacity expanison in place means from March 2022 they will be adding 200klpd in west bengal.

Gulshan Polyols’ additional capacity is some time away. On the other hand, BCL’s capacity expansion kicks in this quarter. So it has first mover advantage along with Globus Spirits in the grain based ethanol space.

Tweet by Varinder Bansal

NITIN GADKARI JI ON ETHANOL

My confidence on ethanol theme went up by 1000% after hearing Nitin Gadkari Ji

Link

ETHANOL DEMAND INDEFINITE

To sugar cos: Jitna dum hain utna ethanol banao…no dearth of demand

Current ethanol production at 465 cr litre

E20 will need 1500 crore litre of ethanol

In the next 5 years – ethanol demand will be 4000 cr litre post flex engines

Industry should not be bothered about ethanol demand

FLEX FUEL ENGINES & ETHANOL PUMPS SOON

Flex engines by 4-wheelers will be ready in next 6 months

2-wheelers have already developed flex fuel engines

Ethanol pumps will be allowed soon; have told sugar cos to start pumps

PM has inaugurated 3 pumps already

REDUCE SUGAR SURPLUS

Sugar cos need to focus more & more towards diverting sugar to ethanol

Sugar cos should reduce sugar production & increase ethanol production

Corn, rice, wheat, sugar have been in surplus for India & ethanol diversion will help to cut supply

Broken rice to ethanol should also be encouraged (BCL Ind, Globus Spirits makes ethanol from grains/ broken rice)

Sugar cos should use b-heavy molasses medium more, discourage c-heavy molasses route

ETHANOL TO NEXT BIG GREEN ENERGY

Lot of research happening in ethanol usage in future green energy

Ethanol will pave the way for more green energy

Bio-CNG & Hydrogen are next big steps for green energy

Ethanol is used to make bioplastics as well; Brazil is already doing it

Have told cos to reduce dependence on diesel engines

Ethanol can also be used for aviation fuel; Spicejet has done it already

15% ethanol is diesel is also being considered

EV Vs ETHANOL

EVs is not a threat for Ethanol

There is HUGE demand of ethanol for next many many years

ReplyForward

Government sets annual prices and OMCS order based on that for the year. This absence of long term contracts (for all players, not just BCL) is the main reason why companies have been tentative in expanding their capacities (relative to the demand the expansions have been measured). They have been worried on the following counts 1) Yes govt is promoting Ethanol now but what if their policy changes in a couple of years, what we will do with excess capacity. 2) The current prices are remunerative, what if the govt brings down the prices drastically.

Everyone has seen how disastrous past PPP’s in Infra sector has been, so no one wants to spend too much in a Business case where Govt policies can break the use case overnight (this is true for many sectors but especially for Ethanol as all buyers are PSUs).

Now with the Minister assuring the players again and again AND players seeing that govt is pushing Auto industry for flex engines, setting up of pumps, global push for ESG theme etc, they have started feeling more confident about investing in expansion.

Anyone who has done even basic research about BCL knows about this incident. It is indeed an overhang, no one can deny this. I feel thats why its relative valuations have been subdued. I have been invested in BCL since a couple of years and tracking it even longer. In the past few years the company has made concerted efforts to be investor friendly e.g. better disclosures, regular quarterly calls, dividends, hiring professional IR teams to improve the marketability.

I know that still many investors would not like to touch this counter because of 1) The aforementioned issue 2) Company foraying into the unrelated business of Real Estate, which is the easiest way to siphon off money.

I have invested in this stock after considering above issues because 1) I believe that the company though not an Infosys but has been improving in terms of minority shareholder friendliness 2) Bullish on the Ethanol/ENA prospects 3) Cheap(er) valuation, I dont think that the market is pricing in soon to be online Ethanol capacity. 4) Acknowledged that foray into RE wasnt the best decision and wont be done again.

Obviously, I can be spectacularly wrong on my investment thesis.

From whether I have read about EBP.I would like to play this theme through grain based distillery.

For sugar company, a major source of revenue/profitability comes from sugar. India is a sugar surplus country and if exports prices are not above the current level it becomes painful for sugar millers

Prices of sugar in international markets are up because of below average production in Brazil and Thailand in the last sugar season(I’m no expert in sugar market)

Why grain based distillery is better in my opinion, if there is rise in raw material prices- govt can increase the prices of grain based ethanol.

I see edible oil business as an optionality.

I like BCL at current level but due shady past of promoter. I have low confidence.

Thus I will not allocate more than 2% of my capital.

Is there anything that I’m missing out?

I wish management could demerge edible oil+real estate business and ethanol/ ENA business.

Would be value accretive for the shareholders

Company did PAT of Rs85crs in FY22. Market cap is Rs913crs so trades at P/E of 10.7x.

Svaksha 200 klpd comes into action from 1QFY23 and Bathinda from 1QFY24

Ethanol purchase price by oil marketing companies (OMCs) for the green fuel produced from damaged food grains is set to turn costlier by ₹2-3/litre as the government is believed to have agreed to such a hike following an increase in raw material costs.

Disclosure: Invested