The starting post of this thread (Barbeque Nation | Value Seeker) is very well written and gives pretty good context on BBQ.

Personally, I have been to Barbeque Nation, and I was impressed with the experience and I thought this chain can expand across India. What do you call it? Authority bias / recency bias etc etc , I dont know, But some huge bias towards BBQ

However, when it got listed, I had no interest in looking at the company as valuations were not in my favor . But recently, when the stock got hammered (Feb 2025), I started looking at the company again.

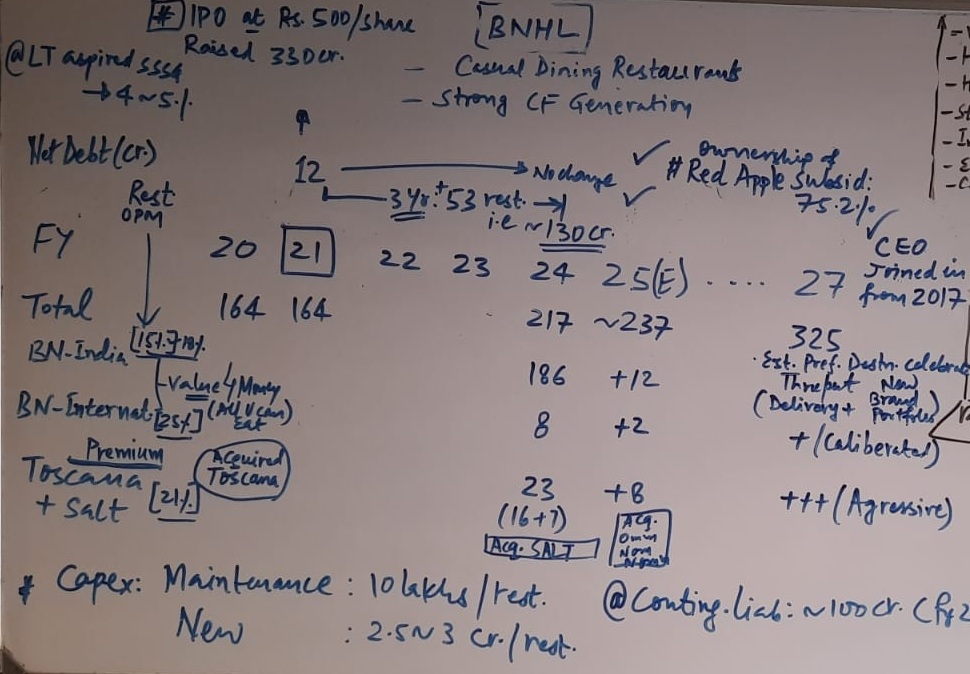

The first apprehension that I had now, is despite taking the restaurant count to 225, why the company still posting losses? Are there many new stores openings, expenses of which (Initial setup cost/ depreciation etc) are front loaded, but revenues back ended? I found its not the case, 80% of the restaurants are in mature category.

Agree that they do generate 70 to 100 Cr cash, and deploy it in new restaurants, and the business funds growth on its own. But saying that depreciation in P&L is not real cost, is not correct , and that you should ignore it, I do not agree to. They are not profitable (for now), even after having 200 restaurant chain.

Looking further, I realized that Same store sales growth (SSSG) for the company is declining since last two years, which is industry wide phenomena, not company specific issue. Currently company does 6 Cr revenue per store , with 200 restaurants , it comes to 1200 Cr annual revenue.

The operating leverage is huge in this business, if sales per outlet can reach 7 Cr, 50% of additional revenues will flow through bottom-line (PAT), which means for 200 outlet, additional 1 Cr sales per outlet, can lead to 200 Cr additional revenue, which may translate to 100 Cr PAT. This is assuming no expansion in terms of new outlets. (These are my numbers, you dont need to agree with me. You can have your own numbers, we can all play the role of investment banker)

Now with above background, and at today’s market cap of 1200 Cr, are valuations reasonable? Well, it depends on your view about BBQ being relevant and able to command its authority in competitive Casual dining space and its ability to grow. This is a qualitative opinion and will vary for each investor.

We also need to also think what can go wrong?

- Casual dining restaurant (CDR) is mortality and fast changing industry, will BBQ be able to keep itself relevant overtime and grow?

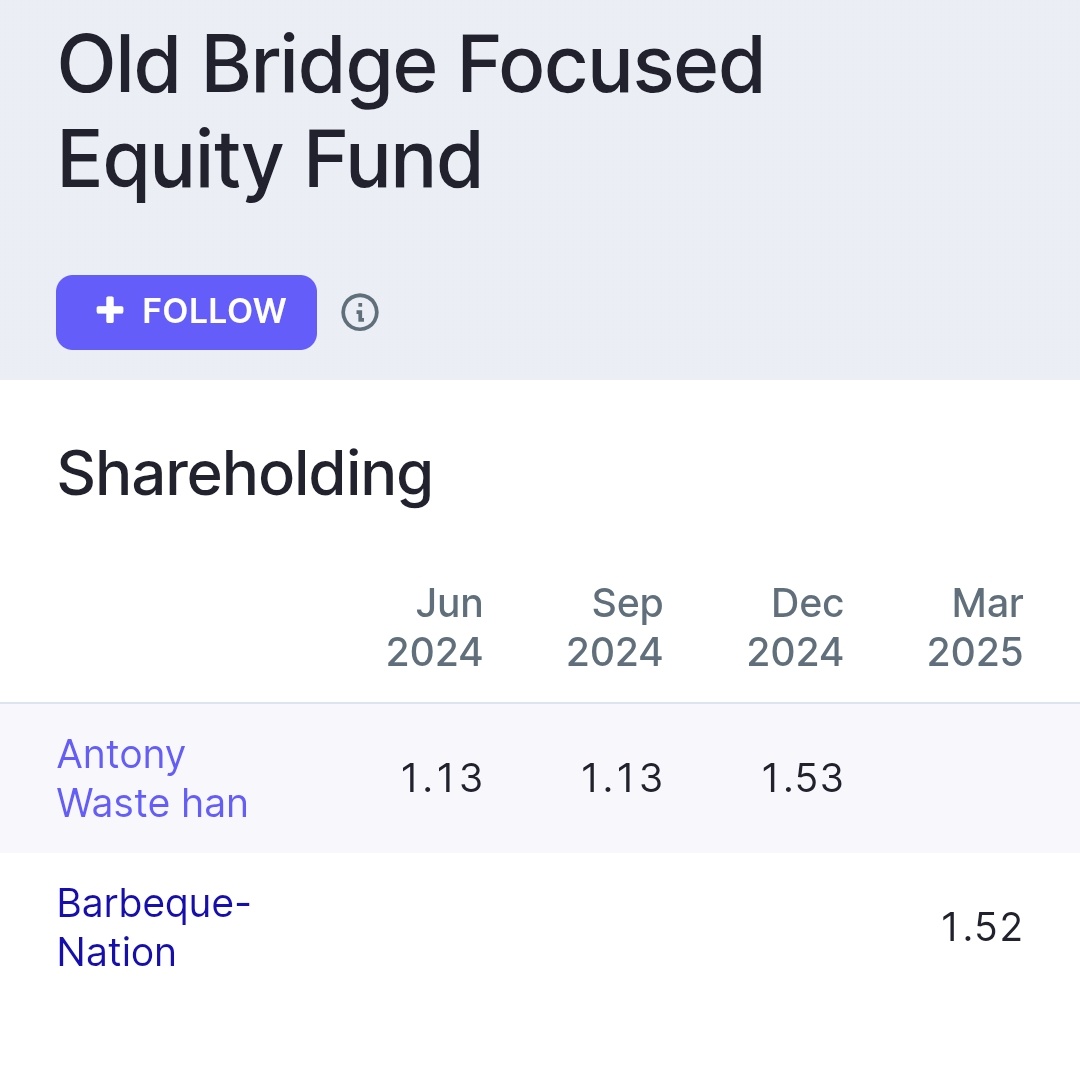

Promoters - I do not have positive view about promoters, about which I have written previously in this post (Barbeque nation Ltd - #22 by Amit2saxena), but presence of Jubliant Foodworks as minority investor holding 10% stake gives some comfort., that minority investors will not be taken for a ride.

Disclosure - Not inivested