yes that’s what looks like - they have already provisioned for the 10% of book, which looks good enough given the SMA 1, 2, 3 numbers and the way partial payments have been made by the customers looks like much of these provisions will probably get written back.

I think high chance 3-4000 cr out of 9000 crs will be written back if no 3rd wave / lock down etc.

The fact that public sector banks still hold ~70% of West Bengal’s deposits provides huge opportunity for Bandhan Bank to gain further market share, which currently stands at 3%, especially given that the bank is offering higher deposit rates than most of the frontline large banks. The higher-rate strategy, even if it continues for longer, is not concerning given that the high-margins on the asset side shall be able to accommodate it.

I listened to the concall as well and the management does seem very confident but as a few people in the concall pointed out the provisioning was out of the blue and seemed excessive.

The slide regarding the stressed portion of the book seems realistic. I think they’ll provide a little but more unless there are some write backs to end the year at sub 1% net NPA

One thing that is a little odd that one brought up was the CoF is still a little high (few bps) even compared to smaller banks like RBL. Is there some legacy borrowings that are doing this ?

how will bank respond, if and when, interest rates are increased and at greater levels. They will have to increase saving rates to compete with legacy banks. While legacy banks have room to increase lending rates, can same be said for Bandhan Bank? Do they have room in their EEB book? In the worst case scenario where interest rates see drastic increase, what will be given priority growth or NIMs?

The RBI will raise rates only to curb inflation. In the scenario of high inflation, I don’t see why all banks, including Bandhan, cannot raise rates. Though it may take some time to pass on the increment. You can’t lower rates below 0, but there is no upside limit theoretically. No matter how absurd such a rate sounds now, in a high inflation period, it may seem reasonable.

The first priority for a bank is to ensure that the money is lent to people who are able to pay it back. Growth or NIM are secondary. As long as the bank management has its priority right, it does not matter much whether they give preference to growth or NIM.

thank you for the reply and pointing to me to the things which I was missing.

I do agree asset quality has to be 1st priority, was just wondering whether we will see low growth or low NIM environment (not taking interest rate hike for granted; just a hypothesis).

Also, RBI can experience forced hand if there is a interest rate hike from US fed, there has to be some parity maintained to attract foreign investors towards weaker economy/country and weaker currency. Again a hypothesis. open for discussion. not to sound pessimistic/but has to calculate probable negative scenarios also.

Disclaimer : i am invested in bandhan bank,

this is not investment advice, I am not a sebi registered investment advisor

please do your due diligence before investing

evergreening or no evergreening(I really don’t know) the bet is on the jockey (Mr ghosh) who I feel will deliver in the future.

ofcourse i am also dissappointed that bandhan mgmt failed to anticipate what happened in assam and should have been less aggressive in lending.

I feel this will be a great lesson for bandhan mgmt

lessons being - diversify across multiple states so that election waivers have minimal impact

secondly - there’s no need to just stick to the lower end of the pyramid in terms of lending and instead derisk by lending to middle nd higher end (more resilient during pandemics)

it’s a bit like kotak bank during the toxic deriavitive days a decade ago and ultimately kotak triumphed (kotak mgmt had great learnings nd ended up being a lot more prudent in the next decade)

I am getting bandhan + gruh at around 25% lesser price than the price during bandhan ipo with hdfc as a big minority shareholder.

both bengal and assam elections are over.

Also rbi has removed restrictions on max interest rate to be charged and theres a certain percentage of microfinance lending guaranteed by the central govt.

Also the stock price action after result shows that market detects atleast a little improvement in coming quarters

the price to book will start looking a lot better once the npa write backs kick in

and market does pay high price to book if it likes the lender for eg au finance at p/b of 6 ( as per moneycontrol)

so feels like the risk reward is favorable. I am invested but keeping a close watch for 2 more quarters and will sell if there is no improvement

other than the assam episode, most of the npa of bandhan is due to external factors like covid rather than a intentional default by its borrowers

Disclaimer : i am invested in bandhan bank,

this is not investment advice, I am not a sebi registered investment advisor

please do your due diligence before investing

Disclaimer : i am invested in bandhan bank, this is not investment advice, I am not a sebi registered investment advisor, please do your due diligence before investing

Growth looks good but the collection efficiency is still on the lower side.

But the fact that the book is growing indicates there are no major write offs

This is good observation. Since it has been downgraded to Midcap by AMFI, there would be some outflow of funds as NIFTY Next 50 Index and/or NIFTY 100 index funds will move out from it. At the same time, some Midcap / Multicap funds may consider it if not invested earlier, but that probability looks less as some of those may already hold it as largecap.

Though I generally believe that, eventually share price will move up/down inline with its EPS, there could be some temperory impact which may or may not be visible.

Disc : Under watch list.

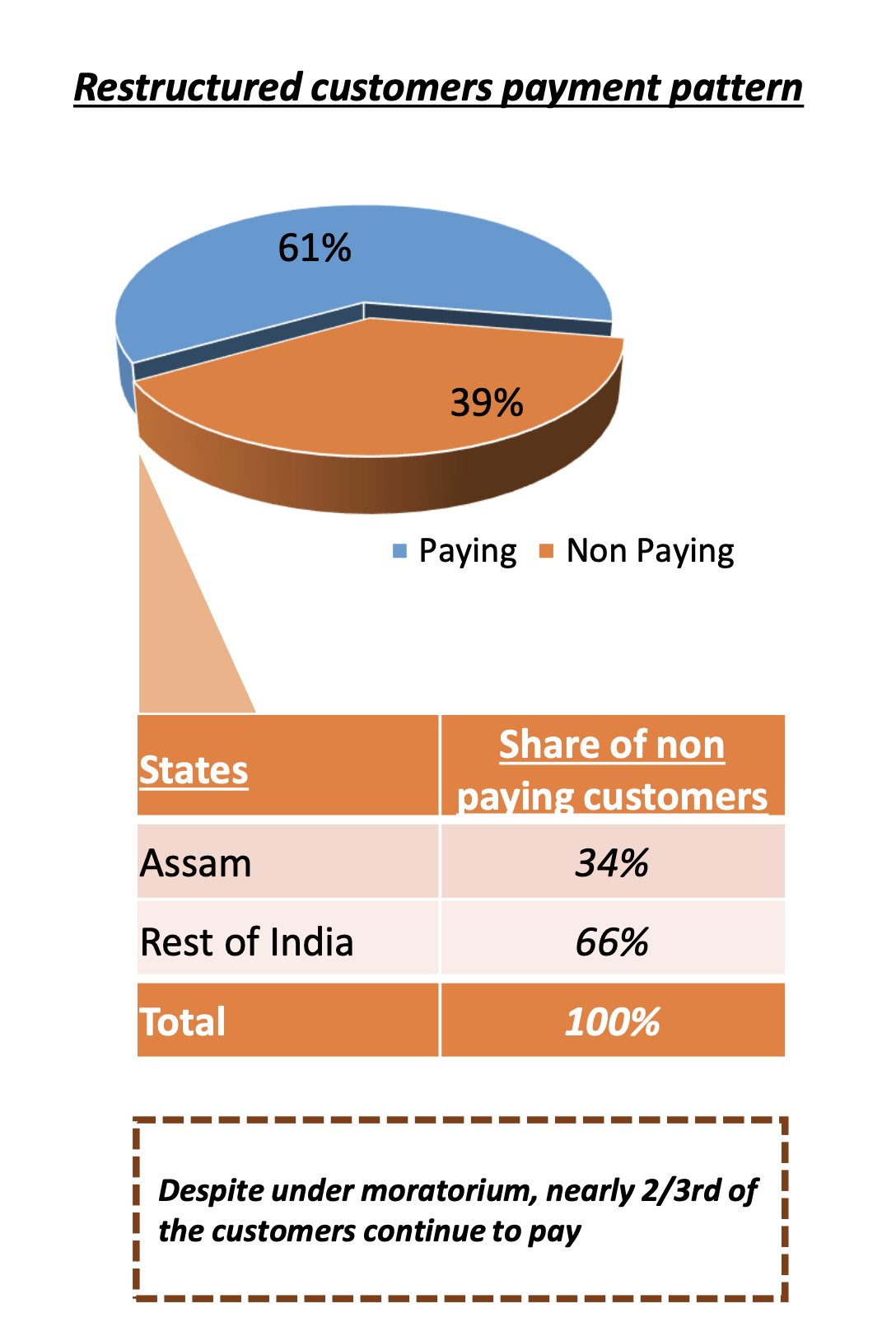

The restructured borrowers who don’t have to pay are paying and that is encouraging, but the 40% not paying are a worry, they don’t have to pay but if they can’t pay after a such a long period i am a little doubtful that they’ll pay when they have to

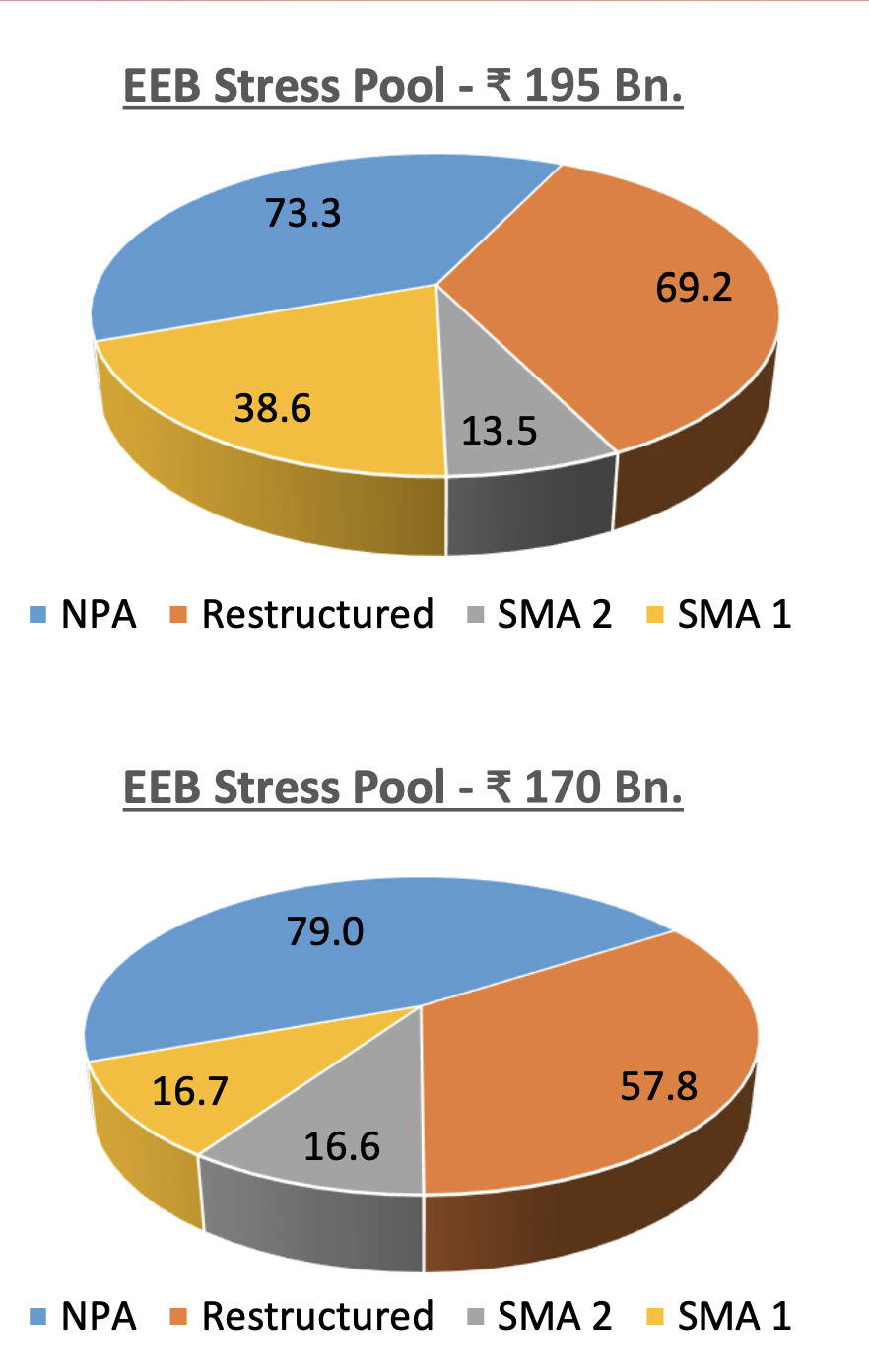

The stressed book is down but i suspect that is mostly SMA 1 borrowers turning regular, the core stress (NPA’s) have increased by 570 cr

Over all looks like a good set of numbers, even with an abnormally high credit cost of 3.4% bandhan is maintaining good return ratios.

Have one question:

Write offs of 1200cr have happened in Q3, provisions of 800cr from the P&L and utilisation of 400cr from the Q2 provisions explains that.

But the overall GNPA’s have increased by 680cr and the PCR has is still the same at 74%. Ideally this would have required additional provisions AFAIF, can someone explain to me what i am missing.

Answered in the conference call:

Std asset provisioning is not considered in PCR calculation, NPA provisions remain the same and since the restructed book is down some of those provisions were used in the writeoff.

NPA movements:

slippages 3400

recoveries 1548

write-off 1200 Not sure why they dont add it to the presentation

CGFMU guarantee can be applied after 31st march expect funds will flow at the end of Q1

Assam scheme:

Started getting money for standard customers, 25k or outstanding, Got 86 cr so far

Expects overdue payments around Q4

ECLGS

Total dispersed: 1905cr

Current outstanding 1045cr

Moratorium end for restructured book

50% by end of march

50% by end of june So these customers will slip (if at all) upto Q3

Overall great numbers, stress is reducing, the have moved away from pure MFI into SME banking and a small retail book

I am worried about the individual EEB book, the average ticket size is 1.3 lakhs and interest is 19.45%, that is a lot

Personal opinion

I think things will normalize in Q4 next year, by then the last bit of covid stress will be out

Even at the current run rate of 900cr per quarter bandhan can compound its book by 20-25%, this should be a good enough buffer for future shocks and this is a battle tested bank.