My question is on the valuation of Banco Products

Current Market cap (493Cr) is lower than the Reserves and Surplus (710 Cr)

Growth could be a concern however i dont think company has any cash flow concerns since Current Assets(excluding inventories) is arnd 400Cr while the current liabilities is 318Cr

So even if the company is going to shut down, the current stock price appears to be cheap.

Kindly guide if i maybe making a mistake here…

How is a company like Banco able to give ₹20 dividend per share when March results were nothing spectacular? Is it a desperate attempt of management to draw in investors ?

Request fellow VPers who are studying this stock to give their views

Many Indian companies had brought forward large dividend payouts after the budget had removed DDT.

That dividend payout was done so that promoters could get the payout before the dividend distribution taxes increased from 22% + extra surcharge of 10% to as high as an effective tax rate of 43% after April 1 ,2020 as DDT was abolished and taxes were passed onto the individuals.

Anyone still tracking this company ? June quarter results have shown good topline growth with 500+ crs of revenue and EBITDA is around 14% which is back to its 2018 levels. Is there any structural change in the company and is this growth sustainable in the coming quarters while maintaing the margins. With acute shortage of semiconductors, Auto industry seems to be under the pump for next year or two and the auto anciliaries could follow suit.

Annual revenue is around 1750 crs and market cap of around 1300 crs. The risk reward ratio seems to be favourable here unless I am missing something.

This is a curious case. Did not know about this Panama Files angle when I researched this company 2 years ago and I am invested in it for the same reasons you have mentioned for your interest and also due to decent positive cash flows they have been showing.

But here’s the thing - since the time I invested, they have already distributed away almost half of my invested price in the form of dividend (Rs 23 interim + final in last FY and Rs 22 interim + announced final in the current one). As such there is nothing much to lose if I think margin of safety.

Yes, the results announced yesterday look too good in Cons. P&L Statement but not impressive on Cash Flow basis (lot of inventory piled up) but that’s a one-off if you compare against the past - can be attributable to the adverse business conditions for Auto Ancilliaries.

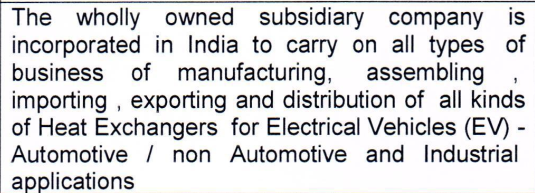

Another thing I observe is the wide difference between standalone and consolidated. A major chunk of its profits are coming from a subsidiary…haven’t yet checked which one. I do know that they have created a subsidiary for catering to EV businesses but I doubt it would become profitable so immediately.

Now that you have brought up this old black money case and Panama Papers angle, makes me wonder if this subsidiary needs some digging.

Usually I would not stay invested with this kind of red flag you have put above but then I don’t even see much to lose. Dilemma!

Banco’s numbers for the year ended March 2022 have been nothing short of phenomenal with all time high Sales at 1958 crs & Profits at 152 crs.Even the operating margins have come in at around all time highs at 14%. With its current market cap at 1217 crs, the stock is available at only about 8 times its trailing earnings.

The Dividend of Rs 20 per share means the payout ratio is 94%. This high payout ratio is not a one off with the Co. passing out in excess of 80% in three of the last four years. The last twelve months have seen a marked improvement in growth rates & accounting ratios.

Looks like a value stock with all the characteristics of a growth stock!!

Company has done well in the last 5 years, growing sales at 12%+ CAGR; and profitability has also improved from Operating Profit Margins at 9% to 16%; however if I view auto industry as cyclical, last time it peaked was in 2014 at 15% OPM… Also a few things I find concerning and request views are:

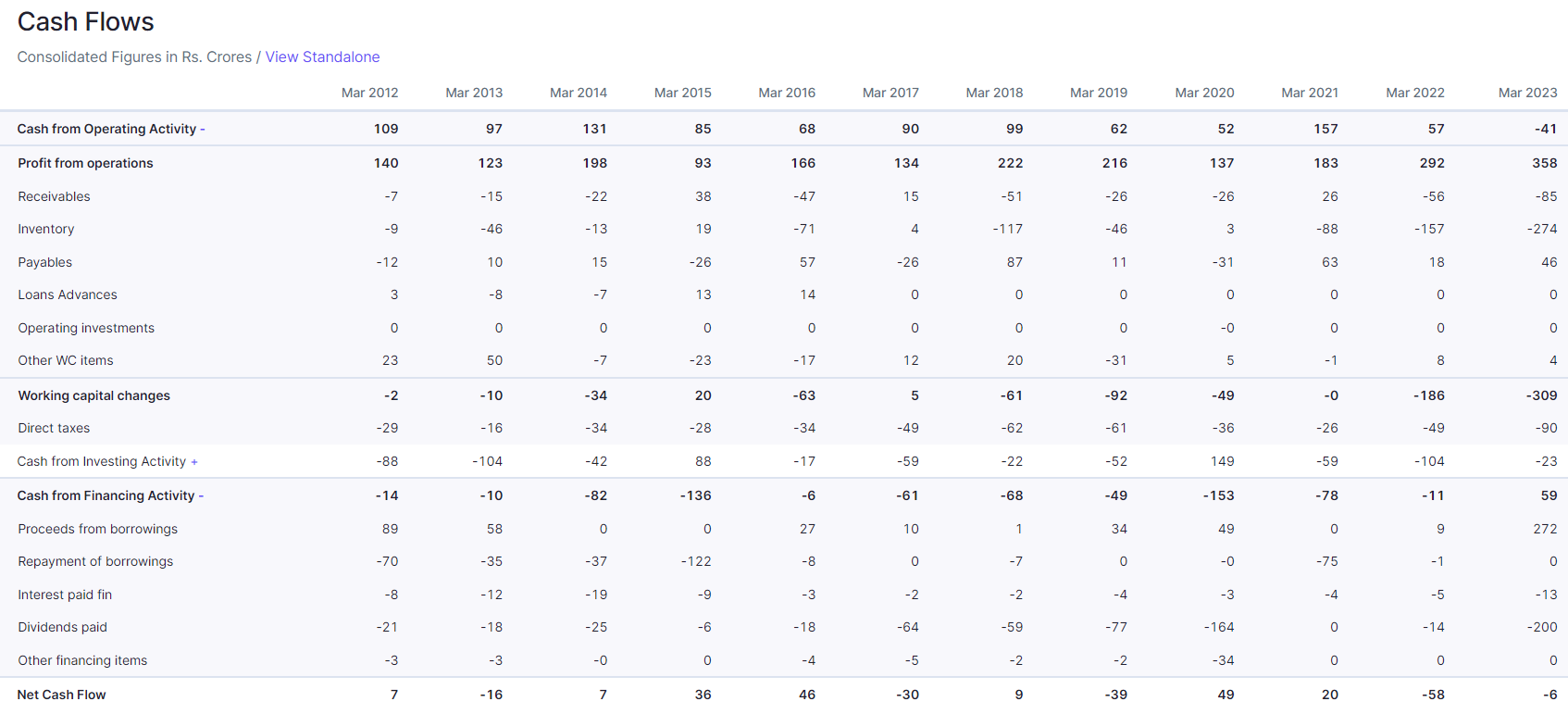

what to make of the rise in inventories (almost 1/3rd of quarterly sales is inventory); to the extent that the operating cash flow has turned negative for the 1st time in last 10+ yrs

To maintain dividend, company borrowed which does not seem a good practice

pls have a look at the cash flow statement at Screener produced below

Banco has become almost 10X since that price!

I frankly did not anticipate this big a rise, otherwise would have invested more

Current OPMs at 18% is 50% higher than the 10 year average; not sure if this is sustainable plus the inventory levels being high are reasons i did some partial profit booking

Yes Harmeet, you seem to be correct, inventories have actually gone down as compared to last year

Change in inventory under COGS in P&L with -ve sign means inventory has built up and hence the same is getting subtracted from COGS. Infact looking at the consolidated data the fall in inventories is even more sharp! Thanks for correcting.

Looking at the cashflow data on screener i got the opposite impression

I’m very bullish on Banco Products. Company is in the manufacturing of cooling system of windmills, transformers, passenger vehicles, off-roaders , dumpers etc etc. Plus also manufactures heat exchangers for industrial machineries, gears, gen sets.

Q2 was the 1st quarter in which company showed 23% revenue growth with more than 100% EPS growth and huge margin expansion. After a huge slowdown of 1 year. Hence FY 24 base is low.

Q2 was very soft for the capex heavy themes but still the company did well. I guess it can post stellar results in H2.

It serves all the marque clients such as Harley , Mahindra, Kirloskar, Cummins, Swaraj, eicher, escorts, intersol, Tata etc etc.

Currently in stage 2 n available at 22 pe.

Heat exchangers is required in almost everything which is capex heavy. Go through the commentary of KRN heat exchangers.

Owing to the current valuations and the growth coming back, I feel it is still undiscovered. On 18th n 19th November the volume spike is due to Graviton, I don’t think this company is in the radar of any institutions as of now. Discovery hasn’t happened.

Plus cash rich. Very good CFO to ebitda conversion. Additionally management gave huge dividends in the past to the shareholders.

Plz read.

Thats true , it is one of the well performed stocks in my portfolio . So what’s happening in the company , announcement of 1:1 and sudden fall in share prices , how do I understand what’s happening in the org ?

its a illiquid stock, broader market condition will play a major role in the stock performance. in last month, the largest of 2 gain days had volumes driven by HFT.

need to dig in more to find information as management doesn’t do concalls.