its a illiquid stock, broader market condition will play a major role in the stock performance. in last month, the largest of 2 gain days had volumes driven by HFT.

need to dig in more to find information as management doesn’t do concalls.

its a illiquid stock, broader market condition will play a major role in the stock performance. in last month, the largest of 2 gain days had volumes driven by HFT.

need to dig in more to find information as management doesn’t do concalls.

Banco Products India Ltd has historically been viewed as a conservative player in the auto ancillary sector, primarily known for its radiator business. This perception has been characterized by:

1) Modest growth trajectory in a mature industry

2) Limited product diversification, with a focus on radiators only

3) Perceived weak negotiating position with Original Equipment Manufacturers (OEMs)

4) Past investments in seemingly unrelated sectors like chemicals and cement, raising questions about capital allocation strategies

However, this characterization may not fully capture the company’s evolving business model and recent strategic initiatives. Banco has been actively expanding its product portfolio, investing in research and development, and exploring new market opportunities, particularly in the electric vehicle and alternative energy sectors. These efforts suggest a more dynamic and forward-looking approach to business growth and diversification leading to Banco Products India which has moved beyond radiator only company and serving non-auto industries too.

I would request everyone to read the entire thread. By reading posts from 2013 till today – one will truly appreciate how far the businesses has evolved and how market treated Banco perceived with no growth potential and EV migration threat to kill radiator as an auto product. @hitesh2710 bhai has covered Banco’s business description very well in his Feb, Mar 2014 posts.

Banco Products’ strategic acquisition (for 17.7mn Euro against net current assets of 24.8 million Euro) of Nederlandse Radiateuren Fabriek (NRF) in 2010 has emerged as a transformative move, positioning the company as a significant player in the European automotive components market, cooling solutions and heat exchanger manufacturer. Key highlights include:

Strategic European Footprint

• Three manufacturing units across Europe

• 11 warehousing and distribution locations

• Presence in over 80 countries

• Extensive product portfolio with 10,000+ Stock Keeping Units (SKUs)

Market Expansion & After-market EV Products Offerings

• NRF has become a leading manufacturer of automotive, industrial, railway, and marine cooling systems

• Provides Banco with a technological edge and faster market entry in European markets

• Contributes significantly to the company’s export-driven growth strategy

• As a leading manufacturer and supplier of automotive aftermarket parts, NRF offers a wide range of cooling products and solutions that are compatible with various vehicle brands, including Tesla. https://nrfinnovationrange.eu/

Performance Metrics

• Contributed to Banco’s revenue growth of 21.43% CAGR over five years

• Helped improve the company’s operating margins to 15% in fiscal 2024 from 10% in fiscal 2019.

• Enables Banco to diversify beyond its traditional Indian market

• The NRF acquisition has effectively transformed Banco from a regional auto-ancillary player to a global cooling systems and heat exchanger manufacturer with a robust international presence.

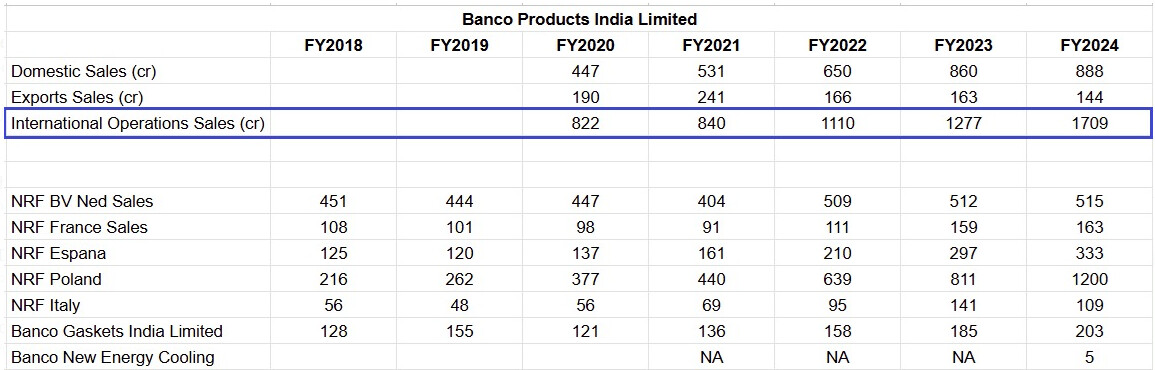

Let’s zoom-in and look at how the European Subsidiaries are performing and are playing a crucial role in this transformative consolidated numbers for the parent company Banco Products India:

Banco’s true transformation begun after selling off Lake Minerals Mauritius Limited (LMML) and Kilimanjaro Biochem Limited (KBL). The company planned to exit from these unrelated businesses by selling its stake to Agro Scientific Investments Limited (ASIL), Mauritius. The transaction was expected to be completed on or before April 2019.

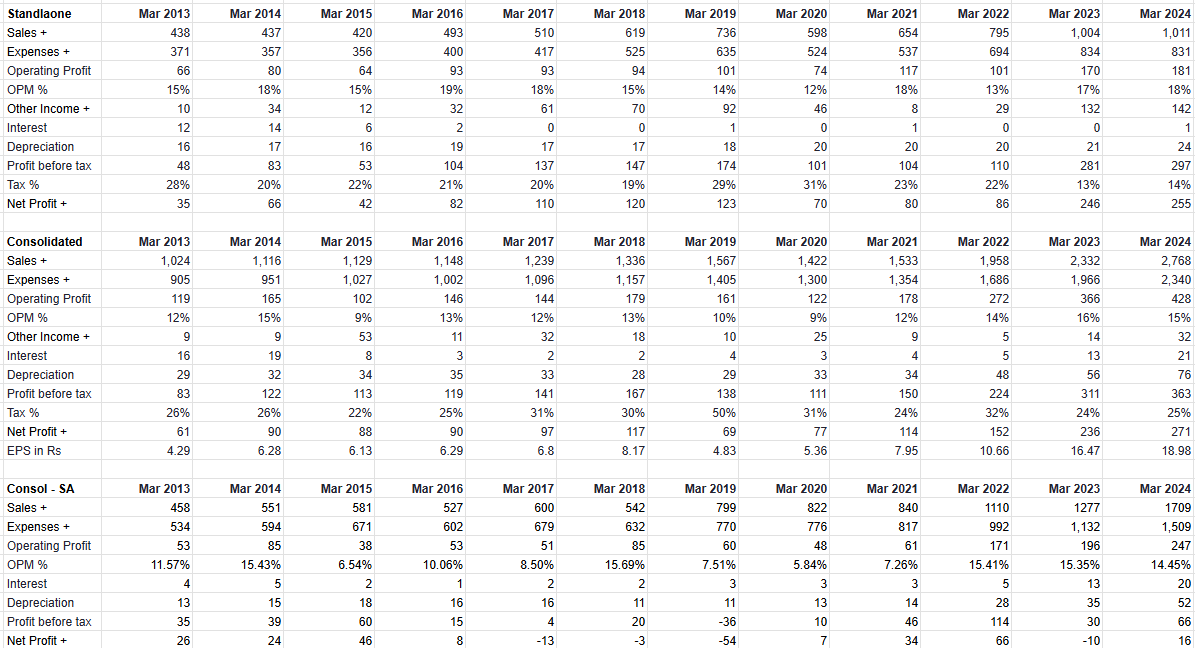

Both Standalone and Subsidiaries (mainly European NRF subsidiaries) were doing topline of about Rs. 450cr in 2013. Standalone grew to Rs. 1011cr and Subsidiaries to Rs. 1709cr by FY2024.

Domestic Standalone business has grown exceptionally from FY2022 while European business has flourished from FY2019 till 2024.

Both India and European businesses are clocking about 18% very impressive EBITDA margin.

Europe business is operating at a very healthy >25% ROCE while maintaining strong operational growth.

Below links will help better understand the European business:

The “Innovation Range” by NRF, their latest series designed to meet the growing demands of the e-Mobility market in Europe. This range focuses on innovative aftermarket components for Tesla models, offering 25 new product categories for suspension, exterior body, filters, brakes, sensors, etc. https://nrfinnovationrange.eu/ https://nrfinnovationrange.eu/wp-content/uploads/2024/09/NRF_InnovationRange_Catalog_2024.pdf

Offers comprehensive eLearning platform designed for e-Mobility skills tailored for mechanics in the EV industry. Given the shortage of EV technicians in Europe – NRF sensed this as in opportunity and offered ICE technicians to up skill their service and make them ready to fix EV cars as EV car sales increases. With this offering they are able to push their after-market car parts through these trained EV mechanics.

Offer thousands of after-market SKU parts for car brands like Tesla, Polestar, Volvo, Ford, Toyota, VW, etc. https://webshop.nrf.eu/

NRF Europe provides cooling solution for Auto, Industrial, and Marine. https://www.nrf.eu/

Guided by Emmanuel Voguet, Andrea Pisanello and Julie Fontaine from NEXUS, the video highlights all new product categories, including A/C hoses, camshaft sensors, throttle bodies and SCR heated hoses. Special highlight is the unique Innovation Range, with more than 200 new aftermarket parts for all Tesla models. https://www.youtube.com/watch?v=cooSFmUoYvE&list=WL&index=3

Training on EV car maintenance to the technicians https://www.youtube.com/watch?v=-d6hGAwFNgU

NRF recently build their own sensor laboratory at their location in Granada, Spain. The laboratory includes an ISO certified cleanroom where NRF can test, validate and develop all kinds of products. The main focus will be on sensors. It will help NRF to even further expand the sensor offer in the future. https://www.youtube.com/watch?v=RhVmTS1tknc&list=WL&index=2

Watch this video and discover NRF Poland. NRF is the leading manufacturer and supplier of engine cooling and air conditioning parts, and more! Gdańsk facility includes NRF offices, TECHcenter, and distribution center, which supplies all our warehouses in Europe. NRF also have technical trainers driving around in Poland to provide training courses to distributors and workshops. https://www.youtube.com/watch?v=hNlm3WbY2v4&list=WL&index=3&t=329s

What is NRF? https://www.youtube.com/watch?v=EUQqQX5t01g

Preparing electric car Tesla model S to service https://www.youtube.com/watch?v=XxtU3dsZpDk

Reveal of NRF Tesla Model 3 show car https://www.youtube.com/watch?v=3XoW8witb98

Summarizing the Bullish Viewpoints:

It seems like NRF has transformed from a single radiator company to dynamic and innovative auto solutions company post getting acquired by Banco in 2010. 2010-2018 were years of toil and the positive results are beginning to be seen post Covid.

By being early movers to directly train the technicians on EV cars – it is able to create a win-win relationship and being able to push their after-market EV parts especially for a car like Tesla and Polestar.

It has significant presence in Europe with 3 manufacturing units and 11 distribution locations expanded to over 80 countries with 10,000+ SKUs

Absolutely no dilution done by the management to achieve the growth and diversification through European operations and successfully creating a niche business.

Domestic business is a debt free, efficiently run business. Its currently on a growth path helping management grow its topline from 650cr in 2021 to 1037 TTM as of 10th Jan 2025.

Banco and NRF’s main product; radiator and condenser is not going anywhere because of EV. EVs need radiators as much as ICE cars. Below links will help understand why radiators are must for an EV car:

o https://www.youtube.com/watch?v=rEK5euR8eeM&list=WL&index=2

o https://www.youtube.com/watch?v=gjNuZ0ZM4PI&list=WL&index=3

o https://www.youtube.com/watch?v=DxEnBunySj4&list=WL&index=4

Valuation seems to be comfortable along with 2.11% dividend yield.

Summarizing the Bearish Viewpoints & Risks:

It’s been a slow moving ship and has caught some speed after a very long period of time. Any slowdown in auto sector or EV demand can derail the current growth ride.

Management doesn’t openly communicate and share business insights through con-call or presentations.

Banco was found part of ugly IT Panama papers controversy in 2019-2020 casting red flags towards the management I-T settlement panel can resolve foreign black money matters: Gujarat HC | Ahmedabad News - Times of India

Disc: invested and biased

PS: In next post I will share why Poland’s automotive aftermarket is a possible game-changer for NRF, and how NRF is strategically positioning itself to capitalize on this dynamic landscape. Also why NRF’s EV training studios are helping them to be “at the right place at right time”.