Hi , learning

Though your query is addressed to Hitesh Sir but sharing my views ! Tried to answer few things. May or may not be useful to you.

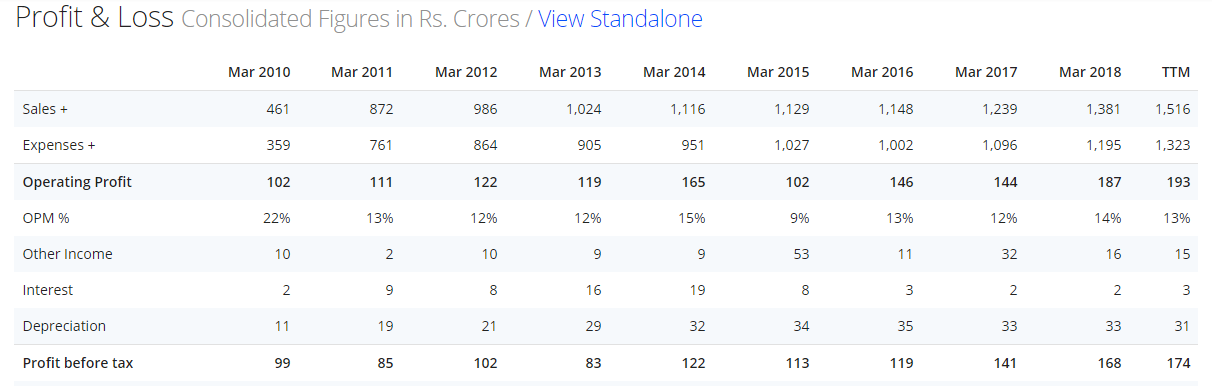

It is more a Value Buy then a Growth Buy at present. The company accelerated product development initiatives and has added new products for OEM, Replacement and Exports markets during last 2 years which in my opinion has aided growth.

The company deals in Aluminium Radiators and Copper Brass Radiators.

Aluminium radiators finds application in the CV and the tractor segments and are preferable to copper-brass radiators due to their economical weight and cooling properties. The growth in aluminium radiator sales has been supported by the healthy demand prospects from the CV segment as well as tractor division. This contributes around 80% of the Revenue. Major Clients are : Commercial Vehicle : Mahindra & Mahindra , TATA Motors , Ashok Leyland

Tractors Vehicles : TAFE, John Deere, International Tractor , M&M , Escorts

Copper-brass radiators are employed by the railways and for industrial applications where heat dissipation requirements are higher.

Clients : Cummins, JCB , Kirloskar , Indian Railways

The copper-brass radiator segment had been facing headwinds till FY 2015 due to a dried up order book and the inability of the company to maintain competitive selling rates but it resurged in FY 2016 with the company receiving a healthy inflow of orders from the Indian Railways starting FY 2016. This may well be the another reason for growth in Sales in Last few Years. Though it forms just around 20% of Revenues.

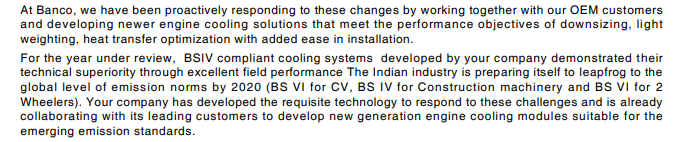

The Indian industry is preparing itself to abide to the global level of emission norms by 2020 (BS VI for CV, BS IV for Construction machinery and BS VI for 2 Wheelers). Good prospects for the company to tap the opportunity and develop new generation engine cooling modules suitable for the emerging emission standards. I believe they have the required technology and it may well benefit in the Medium Term.

Also with growing government spend on infrastructure , demand of products in industrial sectors such as earth moving and construction machinery , power generation equipment , Railways is also looking Good.

Banco’s end user base is well diversified which makes it less prone to being dependent on a single industry. While the major demand comes from the auto industry (CV segment), It also caters to industrial and earth moving equipment, rail locomotives along with agricultural equipment industry.

No doubt , any downward trend in Industrial activity or Automotive Sector will directly affects the performance of the company.

High bargaining power of OEMs restrict margin expansion. Though it maintains OPM Margins around 12-14% Level except one Years when Raw Material (Metals) Prices have risen significantly. Currently the Metal Prices have cooled off significantly and I believe company wouldbe able to maintain OPM Margins around 14-15%.

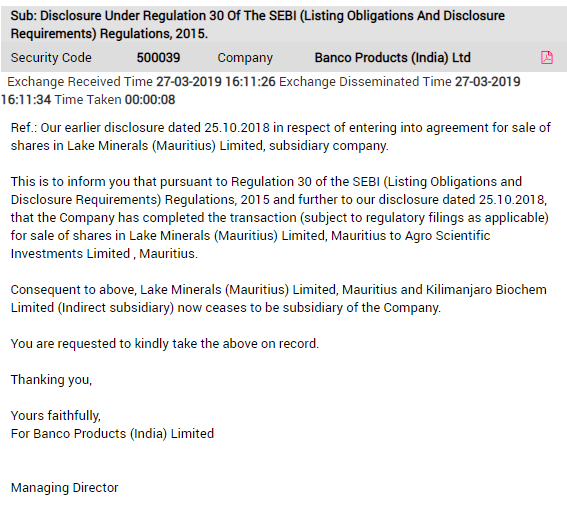

That was a issue but sorted now. Company is going to divest that business and it will help in more concentration on the main business.

I do not know about the declines of exports but if it is , I find it very good. The Standalone numbers which are mostly for Domestic business are pretty good on Margins front. The Netherland Subsidiary has suffered some headwinds due to uncertainty in Europe and has overall impacted the Margins on a Consolidated Basis.

Overall it looks a good buy at Current prices both on Value term as well as Growth prospects. Threats from EV looks far away and company is looking to find suitable products for EV Segment. Need to get more details from Management about Current Order Books.

Disc: Invested