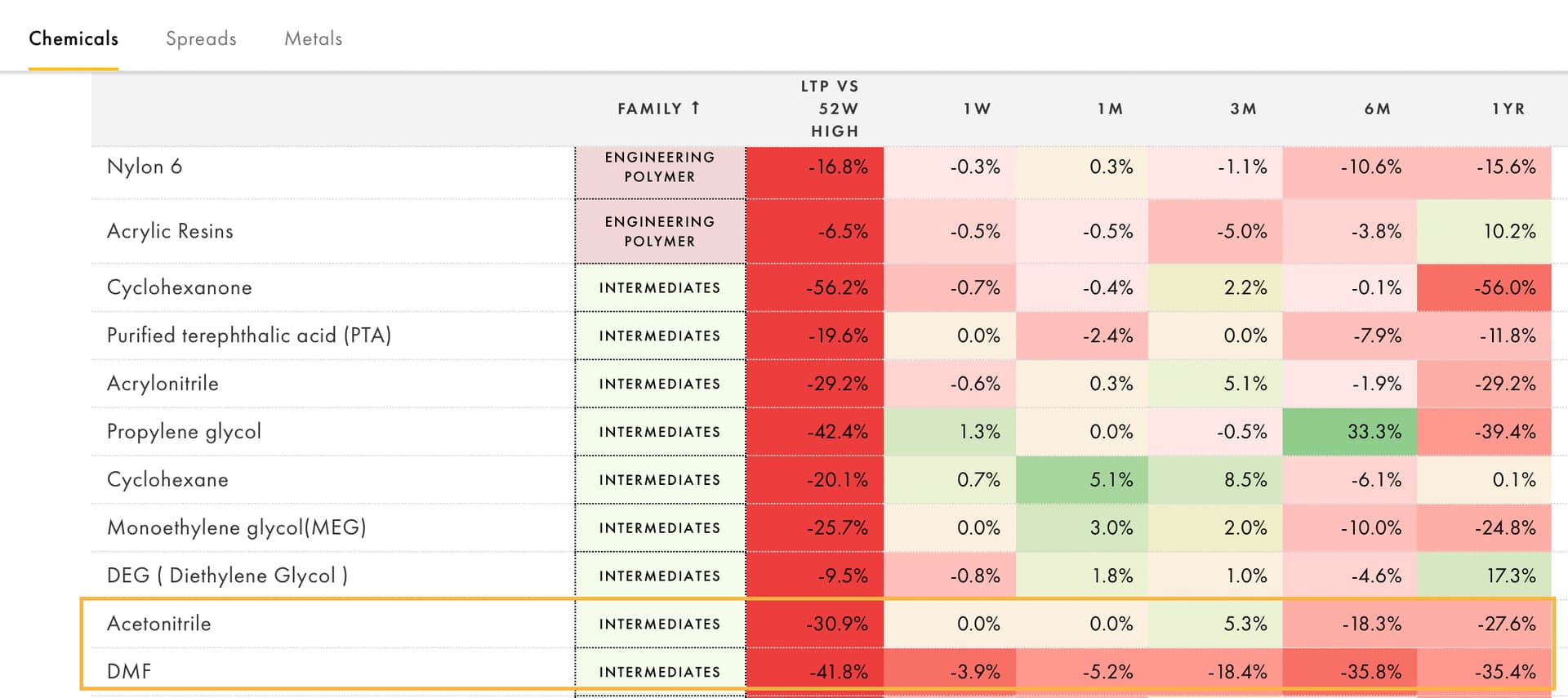

To back up the claims, just check DMF and Acetonitrile pricing

That E is inflated, and 75-85 crore might be the normalised Quarterly PAT going forward

Source: @Sidhegde

To back up the claims, just check DMF and Acetonitrile pricing

That E is inflated, and 75-85 crore might be the normalised Quarterly PAT going forward

Source: @Sidhegde

Hi ishimohit, even if we consider at a runrate of 80 crore per quarter going forward…considering 20 PE , at current market cap of 6400 crore is it not all the negatives are priced in? Even the average PE for last five years also around 22

Lets see, previous down cycles PE was less than 15

320*15= still some cut to be seen as per the guesstimate

Hi Ishmohit, on the free float of Balaji, most of the public > 1% shareholders are all previous partners of the promoters and got their shareholding reclassified as public shareholders, so their shareholding may strictly not be free float.

Hi Ish, wanted your two cents on this. I am new to the markets, so still trying to figure things out. Is the Stock in Stage 1 now after the recent increase in price from 1900 levels to 2500 odd level or is this a short term phenomenon as we know that there might be another quarter of downtrend in Pharma owing to overstocking.

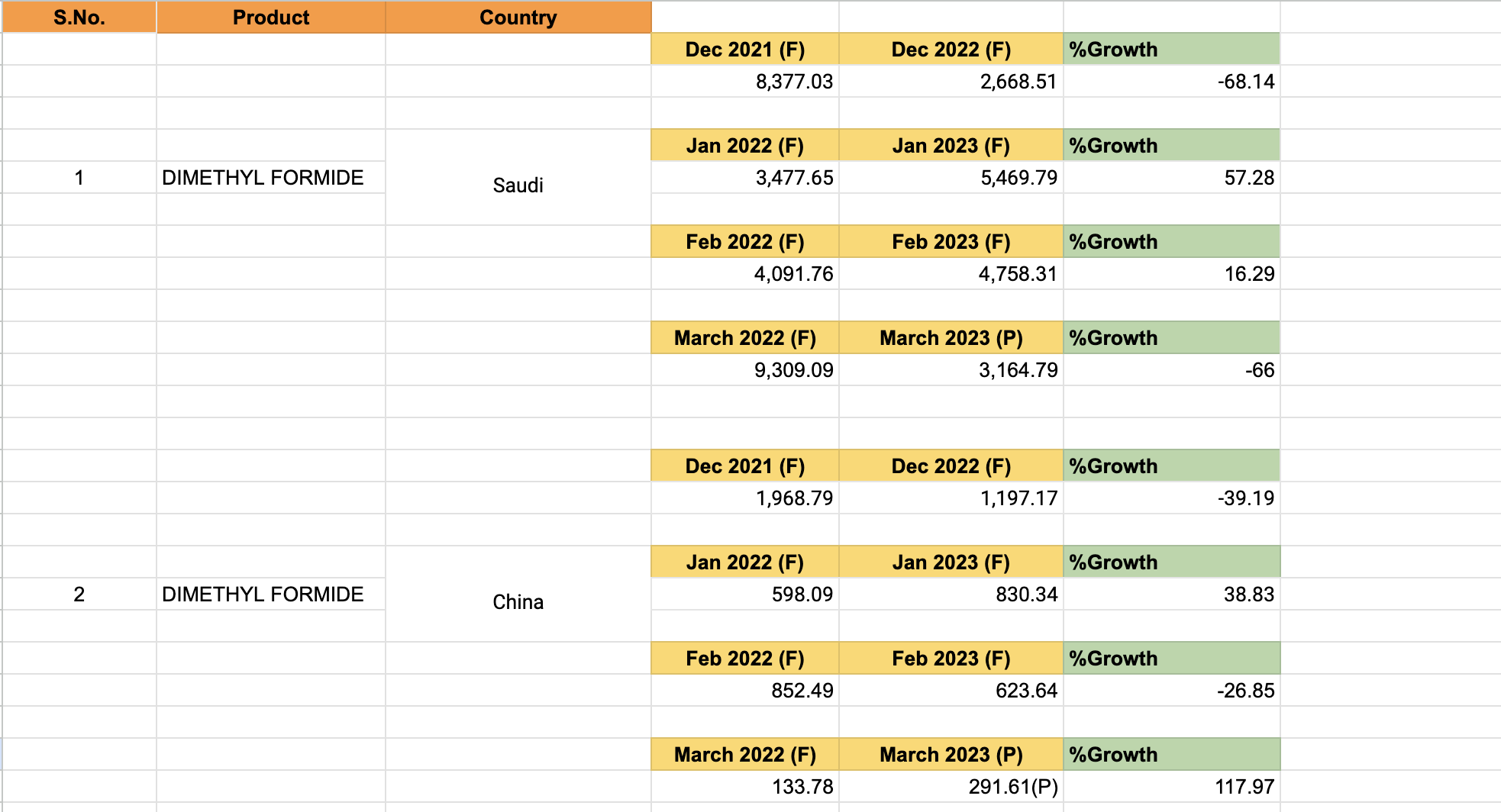

Some cool off is visible in the Feb’23 & March’23 import numbers of DMF.

Note: March numbers are only provisional ones. Took from trade commerce site.

Mass resignations of directors in Balaji Amines. A red flag, does anyone has detailed information?

I think it would have been better to cite this instead of mentioning “personal reasons” as reason for resigning for all of the directors.

Q4FY23 Balaji notes

-Margins fell due to de-growth of Pharma, API & Agro sector.

-In past years experienced exceptionally high realisations led by Covid. Need to adjust expectations accordingly.

-Currently a zero debt company on stand-alone basis.

-Inducted 4 new board members. Each of them come from Diverse backgrounds.

-Changed management roles:- CFO is now focusing on Balaji Speciality.

-Revenues from DMC, PG, Ethyl Amines- Will start contributing from Q1FY24. This can improve the margin potential of the company.

-Have initiated capex for: N Butylamines (15ktp)| During H2FY24

MethylAmines: March 2024

DME: 1,00,000 MTPA: can replace LPG.

AcetonItrile plant: 15,000 MTPA with new tech. New tech will provide cost advantage. This will result in healthy operating margins.

DMAHCL: 12,000 MTPA

DMF: 15,000 MTPA.

-In last few weeks, have seen some improvement in end users. It may take 1-2 Quarters to fully normalise. Our capacity utilisation has started improving.

-All 3: Acetic Acid, Ammonia and Methanol have corrected. This will help the API industry to recover. Prices will come down to pre-covid level.

-Our high cost inventory has been exhausted. Next month there will be no high cost inventory.

-DME: Going for Aerosol market and commercial market like using it for heating for industrial usages. Have the EC, and equipment ordering has also started. Will give exact commencement next Quarter.

-DMC & PG: have seen good off take of these products in last 1 month. In next few months will see these products go full swing.

-In DMC and PG by end of the year should reach 70-80% utilisation.

-In import substitute products, takes 9-12 months to get them approved and only then they see full utilisation & traction.

-ButylAmines: September it will commission. Only producer in the country.

Second plant is Methyl Amines: by March 2024. 40,000 MTPA.

Third plant: DME will be the one.

ACN Plant will come parallel with DME

DMAHCL & DMF will come parallely

-By FY26 should expect 1,80,000 MTPA utilisation. Doubling of volumes on stand-alone basis.

-In Subsidiary, have applied for new land for new expansions. In 2-3 weeks time, they are looking for new products for the first time in the country. Acquired Sodium Cynide technology. Several new products will be launched in the subsidiary.

-5 TO 7% margin improvement should be there from here on wards for the entire industry.

-Only compete in one or two products with China. DMF has started improving from this Quarter.

-Due to RM shortage, could utilise subsidiary plant at 70-73%. Earlier we thought we will do 80%.

-Consolidated expect 26-27% margins and standalone 22% margins.

-From last 2-3 weeks we have seen customers increasing the off take. (Pharma customers).

-Sales was lower, we were able to recover trade receivables faster. As industry took precautions, we tightened the receivables as the entire industry was cautious.

-As per SEBI guidelines, no independent director can be on the board for more than 10 years. Majority of directors are finishing 10 years as they were appointed together. One director also attained 75 year age.

-500 companies nearly applied for PLI schemes. If any molecule comes from PLI, all our products will anyways go into full swing.

-Capex for FY24 will be 250-300 crores and same in FY25 as well. All capex will be done using internal accruals.

-For FY24 looking at minimum 10% volume growth and margins will increase 5-7% from the current level.

-In Subsidiary:-

Can double capacity. As 50% products are still imported, we may take a call to double capacities in 2-3 months.

Sodium Cyanide technology: will announce new products in 1-2 months.

De-bottlenecking:- part of debottlenecking has taken place. It will take another 3-4 months.

-Waiting for Lithium battery manufacturers to start their projects. Only then will announce other carbonates and additional 50,000 MTPA plant for DMC. No major usage of DMC apart from this.

-Only 1-2 people are using the ACN technology which we will be using.

Seems it’s corporate rejig as board of both companies was common and now separate entities and boards will be there. This point was mentioned several times in the call @BeatTheStreet10

Disc:- not invested. Tracking

https://twitter.com/BeatTheStreet10/status/1660626890300747778?s=20

Hey Ishmohit,can you please read this and give your opinion. It says that their tenure was going to complete next year July, i.e. 2024 and also they mentioned in the filling that it is because of personal reasons.

Looking forard to hearing from you !

They clarified in the concall as per my view

That two separate companies have been created and current Md has resigned from Speciality board. It’s a non event in my view.

Real issue is this holding company structure as speciality isn’t a wholly owned subsidiary.

Disc:- tracking Balaji speciality as BA will have a hold co discount or one will have to keep doing SOTP. Don’t own

Balaji Amines is one of the largest producers of aliphatic amines in India. Making a start with Methyl Amines, the Company went on to manufacture Ethyl Amines and other derivatives of Methyl and Ethyl Amines, leveraging in-house developed technology and processes. The company has over 30+ products in its basket and has a global presence in about 51 countries. Presently, there are 5 manufacturing plants all working between 50% - 80% of their capacity and have over 830 customers worldwide.

Key Clientele includes but is not limited to Sun Pharmaceuticals, Dr Reddy’s, Aurobindo Pharma, Jubilant Lifesciences, Teva API, Hetero Drugs, Kores India Limited, Venky’s (VH Group), Wanbury, Zydus Cadila, Indian Oil, Hindustan Petroleum.

Constitutes 47% of the Revenue – alongside the derivatives

Products: Mono Methyl Amine, Di-Methyl Amine, Mono-Ethyl Amine, Di-Ethyl Amino Ethanol and related sister compounds are a few of the products produced under the Amines division.

Application: Pharma, Argo, Photographic chemicals, Rocket fuel, Dyestuff intermediaries, Rubber chemicals etc.

Aliphatic Amines find increasing consumption and applications in chemically mature industries such as India, Europe, US, China & Japan

The Aliphatic Amines industry is expected to grow at a CAGR of 5%-7%

The company is among the two major manufacturers of Aliphatic amines and its derivatives in India with a market share of ~50%.

Products: Mono-Methyl Amine Hydrochloride, Mono-Ethyl Amine Hydrochloride, Choline Chloride and Di-Methyl Acetamide are a few examples of the products offered in the Amine derivatives section.

Application: Pharma, Pesticides, Performance chemicals, Specialty Chemicals, Animal/Poultry feed additives.

Amine Derivatives are used to make further salts and other complex chemical intermediates and APIs

In derivatives, Di-Methyl Amine Hydrochloride (DMA HCL) is one of BAL’s key product offerings

Specialty & Other Chemicals

Constitutes 52% of the revenue

Products: Morpholine, Acetonitrile, Dimethylformamide, Gamma Butyrolactone, Pharmapure Povidone, N-Methyl-Pyrrolidone, 2-Pyrrolidone, N-Ethyl-2-Pyrrolidone are the products offered under the specialty chemical division

Application: Production of Water Treatment chemicals and pesticide formulations, Solvents across industries like pharmaceuticals, petrochemicals, dyes, Agro and paint industries.

Albeit a small and fastest growing segment – The single largest produced product within the specialty chemicals division.

Balaji Amines is the sole producer of most of the chemicals listed in the specialty chemicals space. Examples include N-Methyl-Pyrrolidone, Gamma Butyrolactone, 2- P etc.

Constitutes 1% of the revenue

The company owns Balaji Sarovar Premier, a 5-star hotel in Solapur. It has over 129 rooms with a recorded occupation rate of around 69%.

Amines are a large class of nitrogen-containing organic compounds derived from Ammonia. Aliphatic amines find usage in chemical, pharmaceutical, rubber, plastics, dyestuff, textiles, cosmetics and metal industries. These chemicals are used as intermediates, solvents, rubber accelerators, catalysts, emulsifiers, synthetic cutting fluids, corrosion inhibitors, flotation agents, etc.

Globally, China is the largest producer and consumer of Amines accounting for about 60% of the market. The growing anti-pollution norms of the Chinese government to tackle the old manufacturing plants and the growing anti-Chinese sentiment across the world is catalysing demand for these products from close competitors like India. The Indian Aliphatic Amines market is expected to grow at a steady CAGR of 3.7%by 2030.

Specialty chemicals can be a single chemical or formulation of multiple chemicals whose compositions can influence the performance of the products in which they are used. In market terms, specialty chemicals are low-volume, high-value products used in agrochemical, dyes, food & beverages, fragrances sectors and many more.

The Indian specialty chemicals industry has expanded exponentially in recent years. It represents 22% of India’s overall chemicals and petrochemicals market and is valued at US$32 billion. The segment accounts for more than 50% of chemical exports. Sectors such as dyes, pigments, Bulk Drugs, Pharma and Active pharmaceutical ingredients (APIs) remain dominant in driving export potential.

The domestic market reported moderate performance in FY23 growing at about 18% from the previous year. But margins came under pressure due to inflationary headwinds and the rise in input cost, energy prices and logistic rates.

Globally, China is the largest player in the Specialty chemicals division but with the pollution control norms and the China+1 offshoring strategy that the Global manufacturers have started to adopt, the demand for is rising in India.

The Indian specialty chemical market is expected to grow at ~12% CAGR to US$120 billion, which will presumably double its share in the global market from 3-4% to 6% in the next 2-3 years to come. Investments cumulating to Rs. 17,500 crores are reportedly lined up for FY24, indicating Rs. 27,500 crores peak revenue potential.

The firm commissioned the construction of new plants. The plant comprises of production capacity of 15,000 tons of Di-methyl Carbonate (DMC)/ Propylene Carbonate (PC) and 15,000 tons of Propylene Glycol (PG).

Phase 1

The company commissioned Phase 1 of the 90-acre Greenfield Project (Unit IV) comprising the 15,000-tonne Dimethyl Carbonate (DMC)/Propylene Carbonate (PC) plant and the 15,000-tonne Propylene Glycol (PG) plant.

The capacity utilisation in the plants lies between 50% to 70%. Currently, the annual domestic demand for Dimethyl Carbonate (DMC) is about 8,000 to 9,000 tons, with primary usage in Pharma and others; Propylene Glycol (PG) is about 170,000 to 180,000 tons & Propylene Carbonate (PC) is about 3,000 to 4,000 tons which are entirely met by imports.

Phase 2

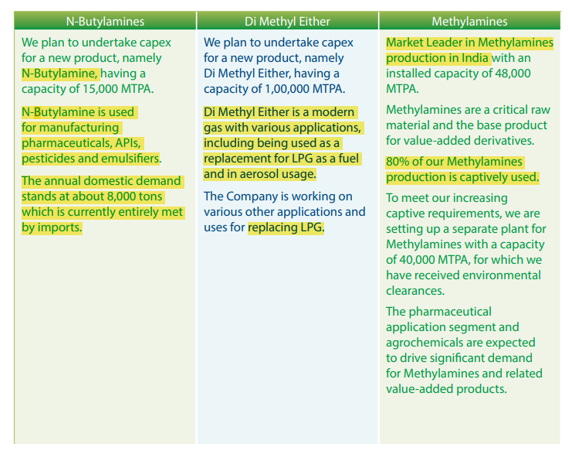

The company outlined our capex plans for the next 2-3 years with an outlay of RS. 4000-5000 million. Out of the above capital expenditures, the Company has also begun construction on the N Butylamines Methyl amines plant, which is anticipated to be commissioned during the second half of FY24.

Methyl Amines : Balaji Amines is the market leader in Methyl Amines products in India with a capacity of 48,000 MTPA; it consumes about 80% of its production for value-added products. To meet the increasing captive demand, the Company has planned to set up a new plant with a capacity of 40,000 MTPA, which is expected to come on stream in the second half of FY24. The Company has received the environmental clearance for this plant.

N-Butylamines : India’s domestic demand for N-Butyl Amines is 8,000 MTPA. It is mainly used in APIs, pesticides and emulsifiers. So far, the domestic demand is met through imports. Balaji Amines is setting up a manufacturing facility for 15,000 MTPA of this product. The production facility of N-Butyl Amines in India will commence operations towards the 3rd Quarter of FY24.

Acetonitrile: The Company has obtained the environmental clearance for the capacity of 16,000 MTPA.

Balaji Amines has a subsidiary , which is a fast-growing specialty chemicals business through its subsidiary BSCL in which it holds 55% stake as of 31st March 2023. BSCL’s product portfolio comprises five niche chemicals catering to a diverse range of end user industries, including specialty chemicals, agrochemicals and pharmaceuticals across multiple applications.

It is the sole manufacturer in India of niche chemicals such as Ethylenediamine, Piperazine (Anhydrous), Diethylenetriamine, Amino Ethyl Ethanol Amines and Amino Ethyl Piperazine, using the Monoethanol Amine (“MEA”) process.

The Company’s Ethylenediamine, and Diethylenetriamine products are REACH certified, which enable it to export these products to the European Union. It has 180+ customers in India and across the globe. A significant portion of its revenue accrues from repeat orders.

Earlier, enmass resignation of independent Directors

now the delay in Quarterly result

Does this signify Governance issue?

Delay by Balaji Amines in declaring its June quarter results following the en masse resignation of 5 independent directors in May! Is it a concern or just a Red Flag? Same is happening in EKI Energy post auditors resignation and FII, DII all have almost sold all holding.

can anyone post the gist of latest conf call? Are they impacted by china dumping?

@basumallick sir pls provide some updates your updates are very knowledgeable.

I have been trying to dig deeper into this but there doesn’t seem to be a lot of information available on this.

The directors who quit cited “Personal Reasons” for leaving the company. However the company management later clarified SEBI rules as the reason - “No independent director can serve on the board of the company for more than 10 Years”.

My issues with this explanation is, if it were true why wouldn’t they announce it at the time? This seems like a cover up reason cooked up later.

Although in the recent weeks, I noticed sudden uptick in the stock price without any relevant news about the company. Does this indicate insider buying? We’ll know only when the public shareholding update is available.

It is noteworthy that recently couple of research reports were released on the Global amine market (eg. insightpartners) according to which the industry is slated to grow at 4-7% CAGR between 2023-2033. Balaji Amines being an oligopoly in India along with difficulty of entering in this space by new players (Amines are dangerous chemicals and need specialised handling, making it difficult for new players to enter, also limits options to import as transport becomes expensive) Balaji Amines should benefit in the long run.

Compared to their competitor Alkyl amines, Balaji amines is trading at a lower valuation right now. Given a possibility of Governance issues, it is probably better to keep a low exposure to this stock.

Disc: I am invested in Balaji Amines

Read the recent concall…Just got confused. The latest capacity of alkyl amines and balaji amines put together is way way more than the total market size. Also Kirit Patel was heard saying that sales as well as margin will take much time coming back to its normal average, let alone the high figures in 2021-22. Does this mean, Alkyl amines will take much time to recover its business performance?