While the di-worse-sification of BAL into hotel business is definitely bad…

In the bigger picture, BAL has excellent PAT growth and amazing future prospects with the huge CAPEX lined up.I don’t exactly get the reason behind such meagre valuations.

2 Likes

I think there could be a few reasons:

1.Underperformance of the pharma sector and high dependence of aliphatic amines on pharma could be one of the reasons.

2. Demerger of BSCL from BAL is an overhang, where a better business with higher margins and lesser concentration on a particular sector is getting separately listed.

3. DMF dumping from Saudi Arabia will create a problem for Balaji.

4. Revival in Auto cycle can cause lower realization for acetonitrile.

We have to see if they can sustain these margins, in case any of the pointers play out at a big scale.

Disc: Invested from lower levels

7 Likes

Further to point

Acetonitrile prices are down to 180rs per KG

And EDA prices are in a downtrend

Finally,

Between 2014-17. Amines industry had a similar soft cycle with low vol growth

Reading Navin’s and Neogens concall, Pharma intermediates are significantly impacted. Revival can take some time

Disc: tracking

9 Likes

Any idea how many share of BSCL will shareholder of Balaji Amines get post demerger?

After listing, BSCL will definitely look to have valuations in the premium range due to its better fundamentals. Do you think if BSCL gets better valuations, market will rerate BAL too?

Re-rating will only happen if the uncertainty in core business i.e. aliphatic amines of BAL goes away, but even after that, market may not give similar valuations to both the businesses. When a better business gets de-merged, even if that business does well, the parent business will not get the same valuations.

Market will sort of see BAL as a holding company, but it will not be a case similar to Kama Holdings and SRF, or Bajaj Holdings and Bajaj Finance, because BAL will not be a pure play holding business, so my understanding is we may see valuations range somewhere in the middle of the spectrum. It could be similar to BSE and CDSL.

At then end of the day, market is supreme, so I will respect that, just my two cents.

Disc: Invested in Balaji Amines since May 2020.

7 Likes

Excellent question, and I wish I knew this back in Oct’ 21, when it touched 5000 odd levels. Fortunately, booked partial profits when it became more than 10 bagger for me, but unfortunately, I didn’t see any reasons to book full profits and completely get out of my position. This is something most of the investors struggle with, and I am no exception.

As they say, everybody is a genius in hindsight. ![]()

6 Likes

Hiii

Any one can share reason Balaji amines is Falling and not alkyl amines and other chemicals companies.all must be affected by the slow down

1 Like

Prices are falling because other chemical companies came out with weak earnings even though Balaji Amines may not be affected that much. But valuation wise if I check with historical PE, this would be a good time to accumulate.

Experts here can you please advise if my thesis is correct or not?

1 Like

balaji amines is in a business where it competes with alkyl amines and directly with mammoth sized chinese companies. do you think this business is sustainable in the long term ? If china again changes its policy, which nobody can predict. then all the business of these 2 companies will go down…for 2 years china maintaines zero covid policy and overnight they opened all borders and removed all restriction. so, if china starts the business again, chinese companies will catch up with all capex within 6 months to reach production levels.

I am invested in alkyl amine, a small position.

4 Likes

Alkyl Amines have obscenely high valuations compared to Balaji Amines, with BA having better financials. Even if 10% business flows out of China and India get 5% share of it, this means huge in terms of volume.

At least this is my thesis, lets see how the results hold up.

2 Likes

Results are out and they are disappointing. However, they are on course of achieving Rs. 2500 cr topline guidance given during year start.

I won’t talk about results as everyone can just read through the PDF. They didn’t have investor call this time. However, MD of the company did came on new channels.

He is guiding for Rs. 4000 cr topline by FY25 based on upcoming capex which will fully be operational by FY24 end. EBIDTA Margin guidance is of ~22% ± 2%. Thats the normalized margin which shoot upto 30% in recent past.

Currently, business is trading at 13.5x Q3 EBIDTA annualized. (Alkyl is trading at 45x)

If Balaji achieve Rs. 4000 cr topline (which seems doable), at 22%, EBIDTA would be Rs. 880 cr. Assuming an EBIDTA multiple of 15x, we are looking at ~37% CAGR growth over next 2 yrs. If the sentiments improve, multiple can also move towards Alkyl’s levels.

I am not factoring in debottlenecking which helps is operational leveraging. I am also not factoring in increased capacity utilization. Neither am I factoring in holding company discount. (I feel impact should not be large on BAL valuations).

PS: I am using Mcap / EBIDTA multiple instead of EV as they are debt free.

Disc: I am invested, hence totally biased ![]()

9 Likes

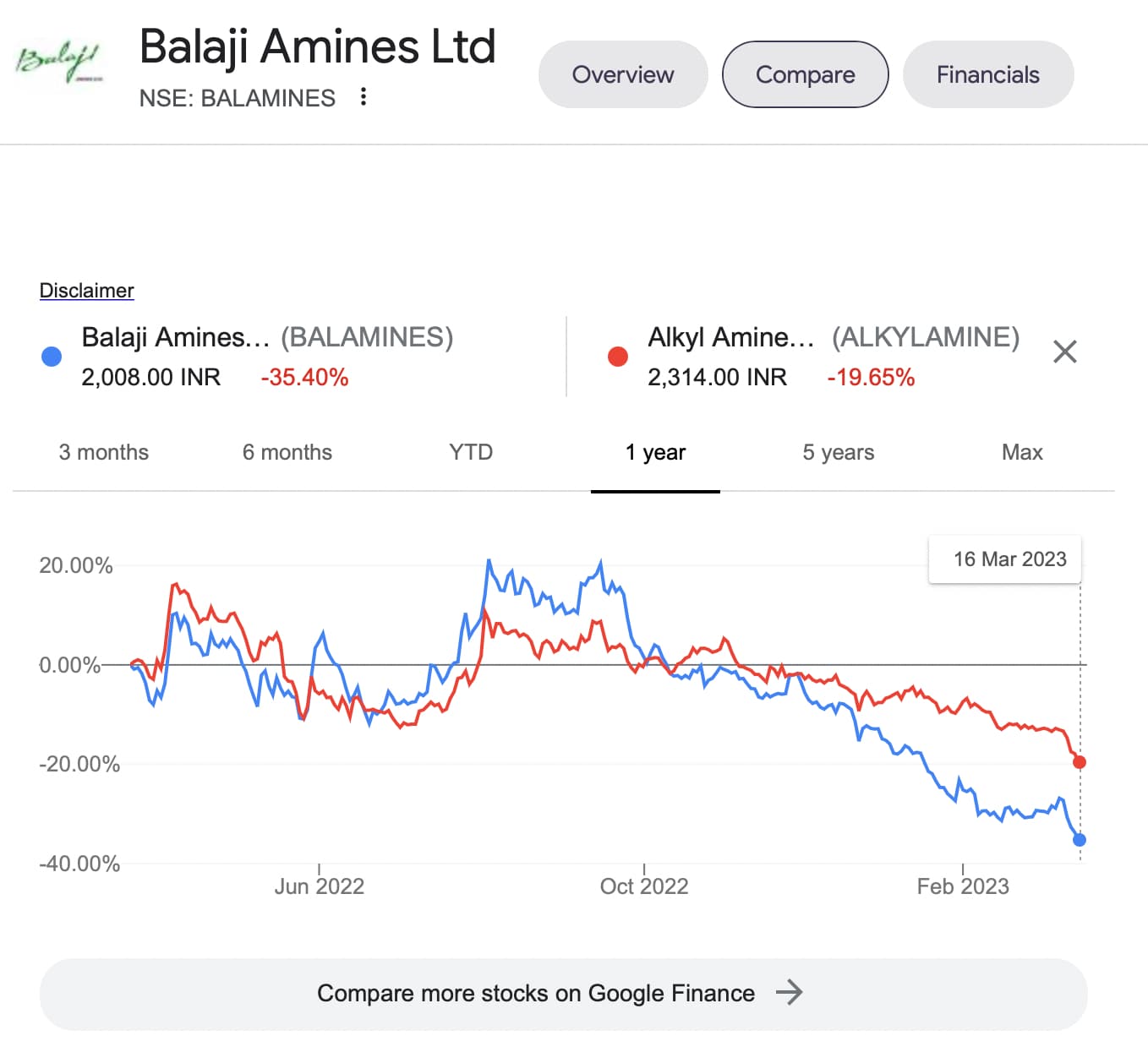

Balaji vs Alkyl:

Balaji is a bigger business (in terms of sales) compared to Alkyl. Margins are largely in same range. Yet the valuations given are starkly different.

There is certain degree of overlap in products sold and then there are certain products which only 1 of them manufacture in India. But thats part of the business.

1 difference that I notice is CFO / EBIDTA a.k.a. cash conversation. Alkyl is more efficient in managing working capital. But this cannot be the sole reason for such a huge difference in valuation.

Another reason why Balaji is valued low can be due to overhang of subsidiary listing. But they are not selling stake. PE wants an exit, which is also normal in any PE funded entity.

Capital allocation can be questioned (reference: Hotel) but thats past. That hotel is very miniscule part of overall business and its profit generating too.

There is a dumping of DMF from Saudi. But thats just 1 product. Even Alkyl manufacture this product.

Both the companies have reasonable amount of upcoming capex / growth drivers. (in case anyone think that market discount future growth and one company might be having better prospects then another).

Both have decent free float, although Balaji has higher free float. But Alkyl doesn’t seem to be case of float cornering.

I would request forum members to highlight if I have missed any point.

Disc: I am invested in BAL.

16 Likes

One reason for the valuation difference could be that Alkyl Amines promoters are family of Hemendra Kothari, well known investment banker and founder of DSP fund.

8 Likes

the company is able to pass on raw material prices after a lag of a few quarters. however, margins depend on global competition since most of Balaji Amines’ products are commodities.

disc: invested

shiv kumar

6 Likes

Time and again Balaji keeps coming up in my screeners. I am already invested but looking at lucrative valuation and upcoming capex, I am tempted to invested more but I am trying to figure out what am I missing? Every company goes through ups and downs. I agree last couple of quarters were not the best but they were not worst either.

Even on standalone basis without specialty business, if company maintains standard 15% margin then that is good. Hope to see last margins catching up this.

At times I really wonder the way market treat companies.

5 Likes

Probably missing factors:-

Soft demand from end customer reminding me of 2014-17 cycle

Dmf dumping happening due to which prices collapsing of end products

Acetonitrile prices correcting heavily to 170 per kg from 250+.

Screener screens on past metrics not on future.

This business will have its cycles and currently we have entered a weaker demand phase for next several quarters as per my thinking of amines cycle.

Disc:- invested in Alkyl in 2019s and was out in early 2021. Track the space closely

18 Likes

Yes, thanks for your inputs.

Yes, hence my reason to mention the upcoming capex.

Wanted perspective from Amines experts, what percentage of Alkyl and Balaji products are overlapping? If Balaji is having weaker demand, prices correcting, etc. then Alkyl too will have same problems… no? If that is the case then how come Alkyl is having huge difference in valuation?

4 Likes

Alkyl doesnt have a hotel, cfl business, separate listed subsidiary which is into chemicals, and cash conversion is much superior+ Public float is much lesser vs Balaji

That being said, even that is expensive and has never traded at these multiples in the past ![]()

Nothing against Balaji, like the entire industry structure. Both Alkyl and Balaji have corrected by 40%+ from peak

7 Likes

Stock price speak truth , management may lie. we read in this thread that promoter of Balaji amines were claiming that they are only one producer of EDA PIP and DETA chemicals but these are the main products of Diamine chemicals limited .so company with dishonest promoters won’t get higher multiples of PE . because there is no single cockroach in the kitchen. it means there may be cooked books of account also. so investors are not ready to assign higher PE multiple.

Do you remember that in housing finance stocks the DHFL was always trading with low PE as compared to peers.

3 Likes