Hi Anjesh,

I am not tracking this stock and not expert in financials also. However, just check the subsidiary is wholly owned (100%) or partially owned. In this case, only profit share percentage will be reflected in the consolidated statement.

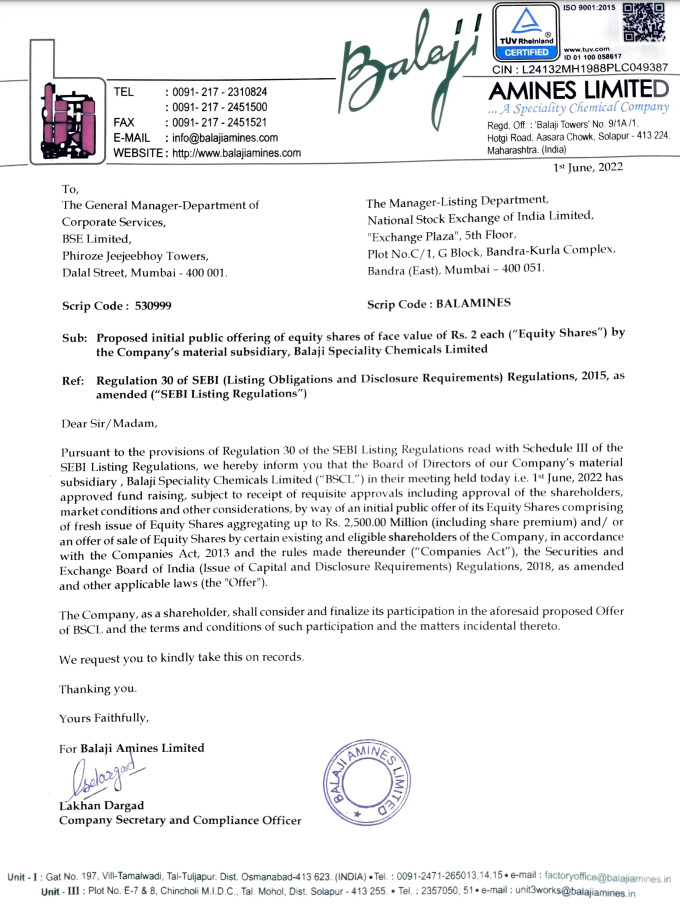

Proposed IPO for BSCL

For past 3 Qtrs. they were talking about merger in their investor presentations, IPO is out of blue.

I have few naïve doubts if anyone can answer them it’ll be very helpful.

- As they are going with IPO route, its a disadvantage for minority shareholders, right ?

- Now, with this news, market will evaluate only on the basis of standalone basis ? Since its no demerger so the current price won’t hold any value of BSCL

3 Likes

The stock price tanked 4% last Thursday. Is this because of quarterly results or filling of DRHP of IPO?

2 Likes

a lot of capex has happened in the standalone business in the past 2 years, two green field projects and a lot of debottlenecking in the current set of products, you will have to read the concalls to understand where the growth in the standalone business will come from. Balaji Speciality will unlock more value coming through the IPO route, they have successfully scaled up the business and the revenue has grown massively. Read the DRHP of balaji speciality, you will understand the value unlock, they have a GST rebate of 9% for sometime on this company( not sure about the tenure) however that’s a 9% straight addition to the bottom line

6 Likes

Good results from BAL yet the stock has corrected today (its been falling for past 40 days). Does anyone know the reason?

results are weak for the valuation market gave them… more pain ahead it seems before we see a stable uptrend.

1 Like

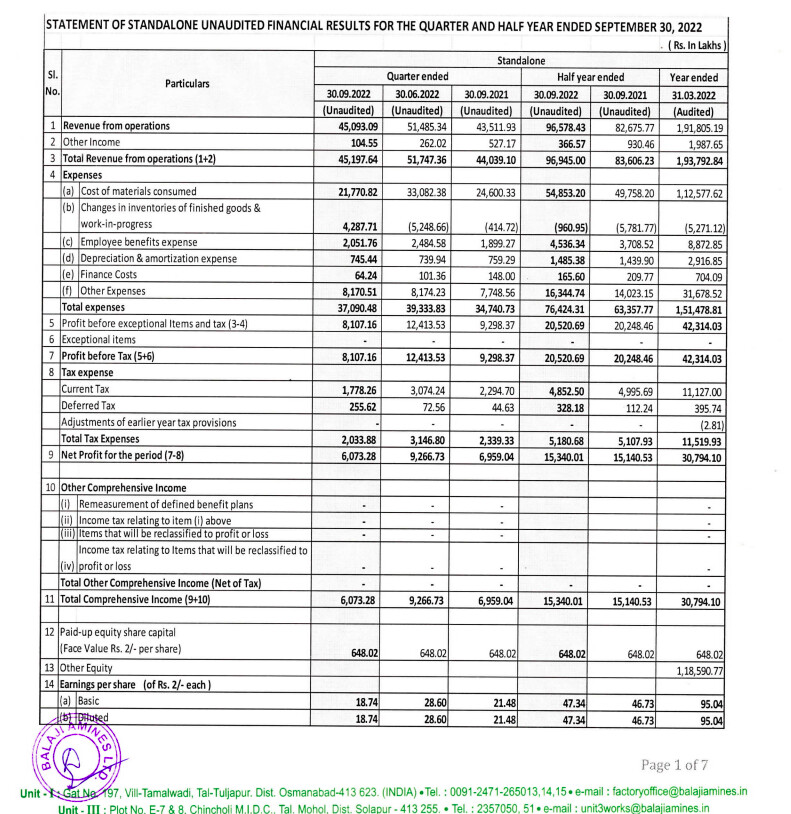

Sales is up by 19%… PBT is up by 36% (so margin has improved)

EBIDTA has improved from 25.5% (Q2 FY22) to 28% (Q3 FY23).

Looking at the cost of material, it seems input cost price have eased.

Management commentary seems fine to meet. They are doing good amount of capex and are on track.

For a company trading at 23 PE / 4x P/S… what more growth is market expecting?

Disc: Invested and bullish on the stock.

3 Likes

IMHO, Balaji amines products do not have seasonal element, lowest sales of Rs. 627.55 crores vs 670,17 and 779.04 in the last 3 quarters. Would love to see opposing views

Disc: Invested

3 Likes

The management is consistently saying that the supply API/Pharma is dragging the topline. It is evident from the results of pharma companies also.

1 Like

Balaji amines standalone number have shown hardly any growth in the topline. Also on standalone basis there is degrowth in net profit.

The company has shown growth only on consolidated basis.

I think the market is worried that once the speciality chemical subsidiary is demerged only the speciality company will show growth and Balaji standalone may not grow.

2 Likes

Management always saying, sustainable margin is 24-26%. In case, it’s more than that, that’ one off

Next guidance is FY25–, they will reach 4000 crs

On Margin, overestimation will disappoint investors

Sales is absolute term may not be relevant in current environment with fluctuating input prices. Compare the volume. Volume has increased in Q2 compared to Q1 (although only 4%). Absolute sales have reducing presumably because of pass-through of reduction in input cost. However, not entire saving in input cost has been passed on, there by helping the margins.

| Q2 FY23 | Q1 FY23 | Q2 FY22 | |

|---|---|---|---|

| Revenue Rs. Cr. | 630.41 | 674.86 | 529.99 |

| Total Volume MT | 28,498 | 27,358 | 23,604 |

| Amines Volume MT | 6,310 | 6,739 | 5,861 |

| Amines Derivative MT | 7,769 | 8,128 | 8,261 |

| Specialty Chemical MT | 14,419 | 12,491 | 9,482 |

@Gaurav_Agarwal your point seems to have played out here. As per MD, there was improvement in product mix, which is true. Specialty chemical sales have increased. However, it is still a wholly owned subsidiary till it gets listed. Also, BAL (parent) will see growth as they are doing capex for multiple products (Methyl Amine, DMAHCL, DMF, Acetonitrile, etc.) increasing the existing capacity by ~50%.

However, I am waiting for investor presentation / concall for better understanding.

Disc: Invested and my views are totally biased ![]()

4 Likes

Notes from CNBC interview Balaji Amines's D Ram Reddy Discusses The Company's Strong Q2FY23 Results | Midcap Radar | CNBC-TV18 - YouTube

- Sustainable margins for the next two years should be around 24-26% :

- Management guiding for 4000-5000 ARR by FY25 taking into consideration the new products from current 2200 Crs.

- DMF plant is at 68% capacity utilization and should reach 75% by next quarter

- Balaji Specility Chemical IPO work is in progress

- Raw material environment has stabilized

PS: Still waiting for concall to release.

2 Likes

Once demerge happens … will that effect the amines business to reach 2025 target

Or 2025 target is not included speciality chemicals

Please throw your light

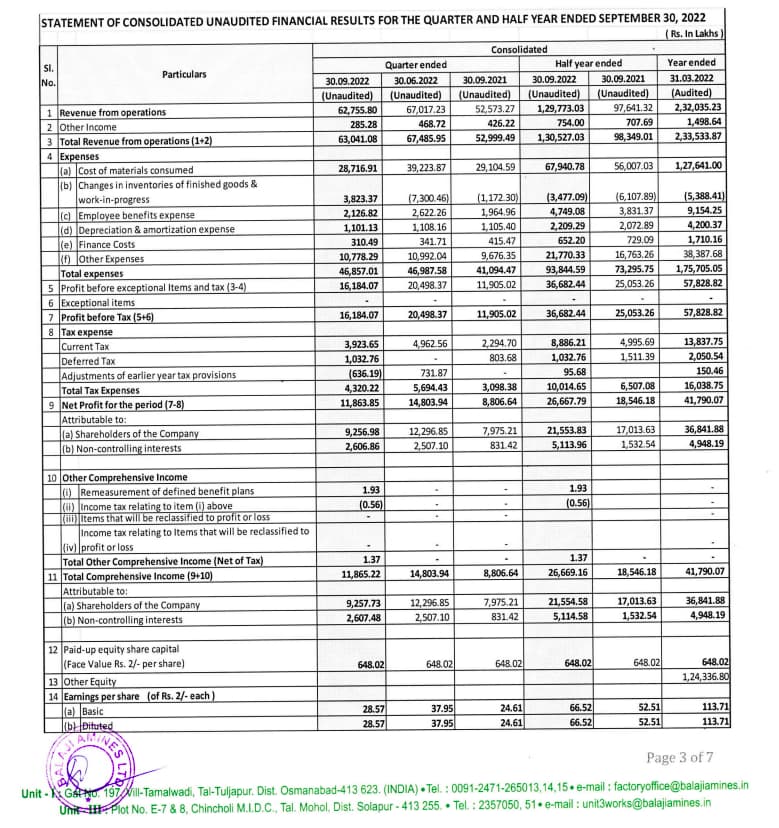

Snapshot of 2nd quarter consol results:

The Company reported a y-o-y growth of 19.4% in revenues during Q2FY23 and improvement in EBITDA margins over the same period. During the last investor call company had given a guidance of margins to be upwards of 20-25%; the same has been achieved.

Sequentially, revenues have declined by 6.4% despite the overall volumes being higher than the previous quarter. The volume expansion of 15.3% in speciality chemicals more than made up for the decline of 5.3% in volumes of amines and amine derivatives over this period. In fact, volumes in Q2FY23 are only 0.5% higher than those seen in Q2FY22 though the revenues are up by 19.4%.

Company’s inventory days have almost doubled during H1. This can impact their costs and will need to be watched for the second half.

During this quarter, the Company commissioned new capacity of 15,000 tonnes of Di-methyl Carbonate, Propylene Carbonate and 15,000 tonnes of Propylene Glycol. Given the H1 sales of close to 1300 crores, the Company is on track to achieve the full year guidance of 2500 crores, especially with the commissioning of new capacity.

Speciality Chem business is not a wholly owned subsidiary; promoters hold direct stake as well. And Balaji Amines is not offering any shares in the IPO. So no immediate benefit from its listing unless the listing multiple is more than what Balaji is getting now.

Disc: Invested.

9 Likes

Hi Guys,

I’ve a question to the senior folks who are tracking the Amines Industry. I have recently started tracking these businesses.

When I look at the metrics I see Balaji is doing very well over Alkyl in terms of margins. However, in last couple of years Balaji has depressed CFO/EBITDA conversion and poor Working Capital management due to high inventory and receivables. But, overall Balaji performing way better than Alkyl.

Do we know the reason why Alkyl commands higher premium over Balaji? Because I see all the Metrics Mcap/Sales, EV/EBITDA, MCap/CFO. It is trading at higher valuation?

Any thoughts please.

Thanks.

4 Likes

I believe its bcoz Alkyl’s free float (30%) is lower than Balaji’s (46%)…I bought into Balaji in Oct’2017 and then bought Alkyl in Jan’20…as amines is a duopoly play in India, hence better to have investments in both of these and not worry about which one does better ![]()

4 Likes

Notes from last week’s cnbc interview. Still can’t find latest concall.

- Seeing pressure in pharma and api industry. 58% revenue is derived from there. The situation should become better by next quarter depending on gas prices/raw material price normalisation(russian/ukraine war and china slowdown)

- Margins might stay around 22%

- Still targeting 2400Cr revenues this year. This might indicate 1 more quarter of muted growth.

- Agro industry revenue share is around 20-25% and is doing well

- Balaji Specialty Chemical IPO work is still in progress

- New methylamine plant will be functional by Q1FY24 and butylamine plant is pending government clearance.

- Not slowing down on setting up new plants as they expect pharma industry to bounce back.

5 Likes

Another Key update was that DMF dumping has started via Saudi Arabia. Majority of growth for Balaji was led by value and not volumes.

Can be painful when cycle reverses for the time being.

Disc: tracking

10 Likes