While we wait for the final annual report to get the full forensic breakdown of FY26, the published data throws some picture of what’s happening under the hood.

Here is my immediate take basis Q4 results:

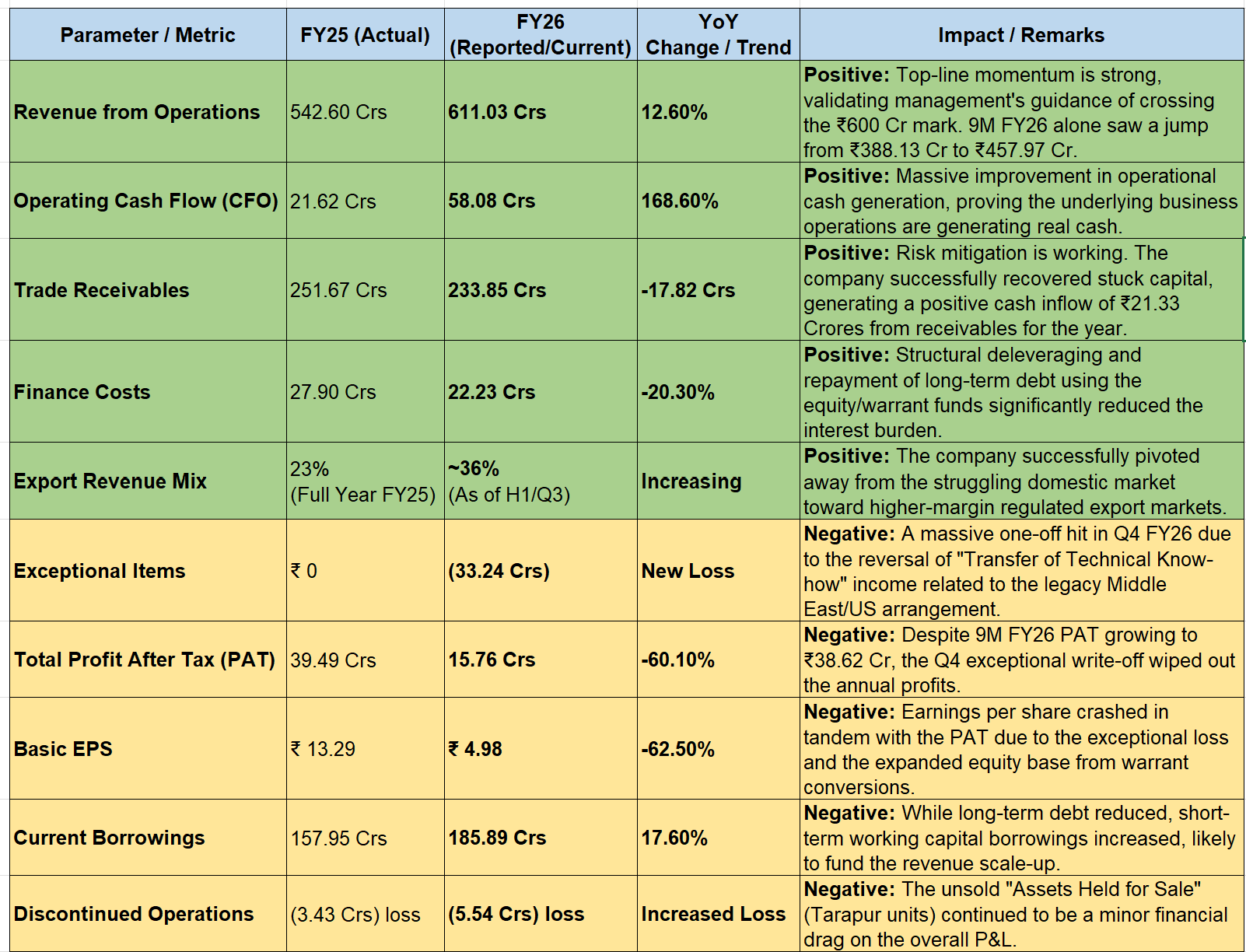

- Positives: The operational engine is looking good. Co. sold more goods, collected pending cash , reduced its long-term debt, and generated its highest operating cash flow (₹58.08 Cr) in recent years.

- Negatives: The accounting profit was sacrificed to clean up the balance sheet. By booking the ₹33.24 Crore exceptional loss to reverse uncollected service revenue from FY23, which as per me they could’ve done much earlier.

Key Deliverables for FY27

- The Peptide (GLP-1) : The peptide manufacturing plant was scheduled for commercialization by March 2026 (no update yet). FY27 will be the first full year of revenue generation for high-demand molecules like Semaglutide (GLP-1)

- CDMO Contract Execution: Commercial supplies for the 30 APIs under the UK/EU CDMO agreement supposed to begin from Q1 FY26.

- Formulations & Genrx Integration: The progress on integration with Genrx Pharmaceuticals.

- Other new launches like Magtein and Centobamate (awaiting DCGI approval), formulations will drive margin expansion