What is the expected sales value for Indian market?

As of January 2025, the market size of Magnesium L-Threonate (Magtein®) in India is estimated to be approximately ₹150 crore (₹1.5 billion).

This estimation aligns with the addressable market size reported by Bajaj Healthcare Limited when they launched Magnesium L-Threonate in the nutraceutical segment in February 2022.

In January 2025, Bajaj Healthcare secured exclusive rights from Threotech LLC to manufacture, distribute, and sell the finished formulation of Magnesium L-Threonate (Magtein®) in India.

This strategic collaboration is expected to enhance the availability and market penetration of Magtein® in the Indian market.

Globally, the Magnesium L-Threonate market was valued at approximately $110 million in 2023 and is projected to grow to around $220 million by 2032, exhibiting a compound annual growth rate (CAGR) of 8.2%.

This growth is driven by increasing awareness of cognitive health and the rising prevalence of neurodegenerative diseases.

Disc: tracking

1 Like

What is the market size of Pimavanserin ( NUPLAZID®) in India?

1 Like

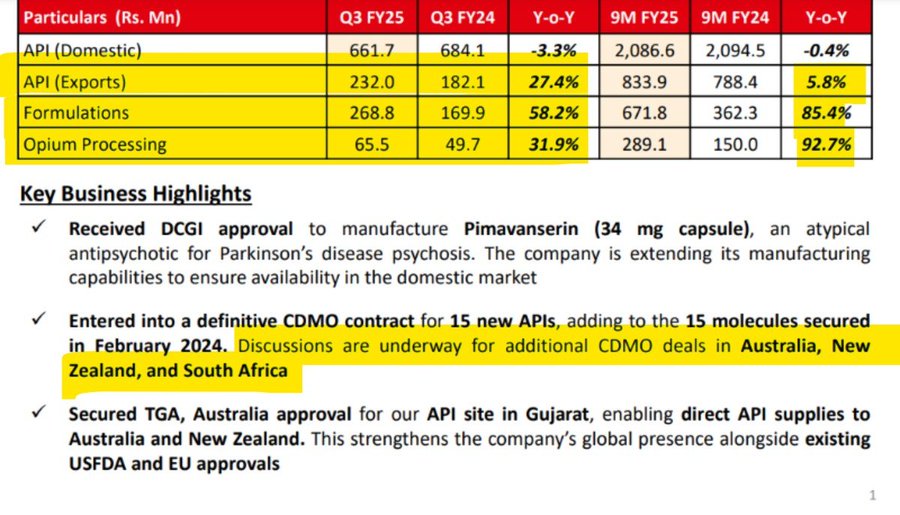

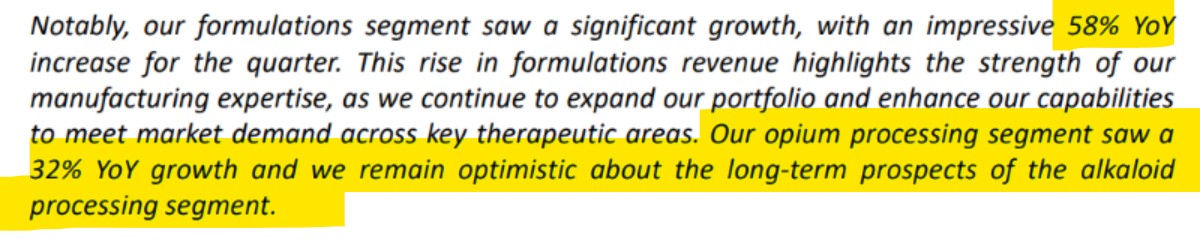

Alkaloid Business is looking good with more headroom for growth, the formulation segment saw good growth, the API domestic market saw a negative growth, though the Alkaloid business remains a negative working capital business (raw material being provided by the government, it’s a niche business and highly regulated), the commentary was positive from the Investors presentation. I think the second point was crucial as they mentioned additional deals discussions are underway. Positive overall.

Disc:- Invested

1 Like

biggest most of this company is its CTO Amit who is one of most sought name in pharma industry compliance. More than company , I am betting on Mr Amit .

2 Likes

3 Likes

Just sharing the results of Bajaj Healthcare

https://www.bseindia.com/xml-data/corpfiling/AttachLive/25ae5074-07b5-40af-8a03-118c29616065.pdf

Looks like good results

Invested and Biased

dr.vikas

3 Likes

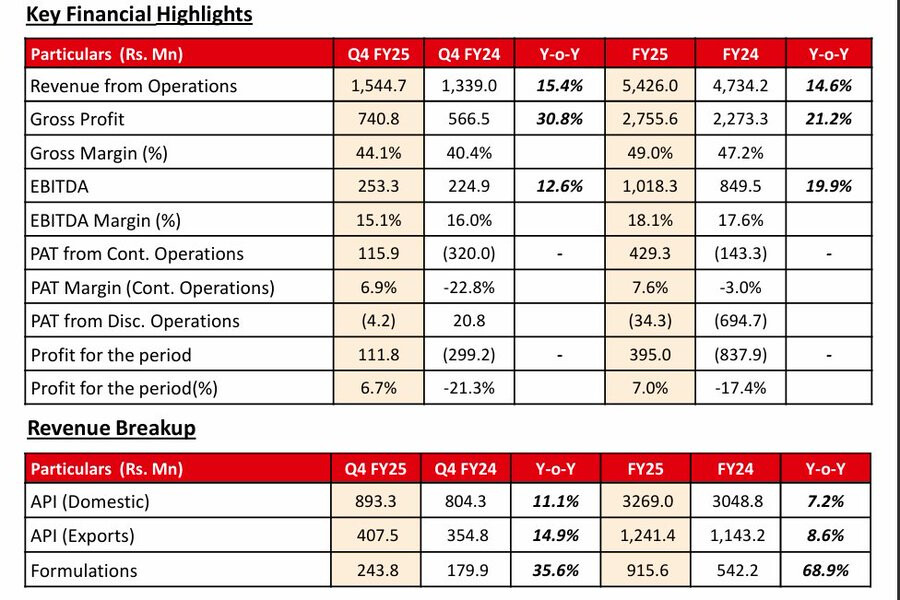

Q4FY25 BAJAJ HEALTHCARE (Bajajhcare) Results analysis :-

-

Bajajhcare (Bajaj Healthcare) continues to scale up, and it’s a perfect turnaround story that I have seen. Disposing of the unprofitable operations while continuing to scale up the API, Formulation and opium processing business.

-

Revenue increased by 15% Y-o-Y for the quarter, while operating profit saw a 25 % decrease Y-o-Y. Net profit also saw a decrease, while the discontinued operations (the ones due to COVID and low demand). Keeps running on losses and adding to the book.

-

PAT from continued operations is profitable, while the Gross margins have improved.

-

Revenue breakup = API (domestic) saw a healthy growth of 11% YoY, API (exports) saw a growth of 15% YoY, while the Formulations segment saw an increase of 36% YoY. The other business it is in is the opium business (making poppy straws from alkaloids). Overall, API biz grew by 8% Y-o-Y.

Key points in the Presentation : -

-

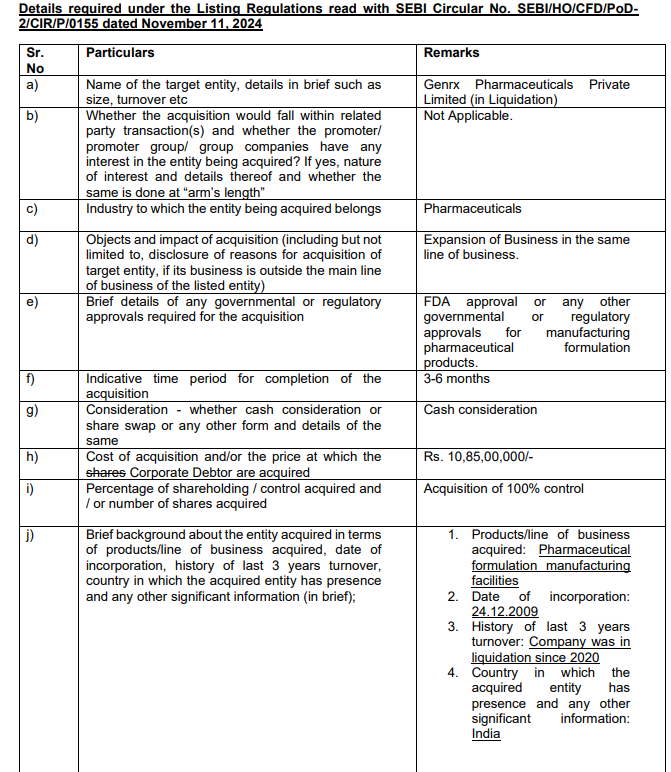

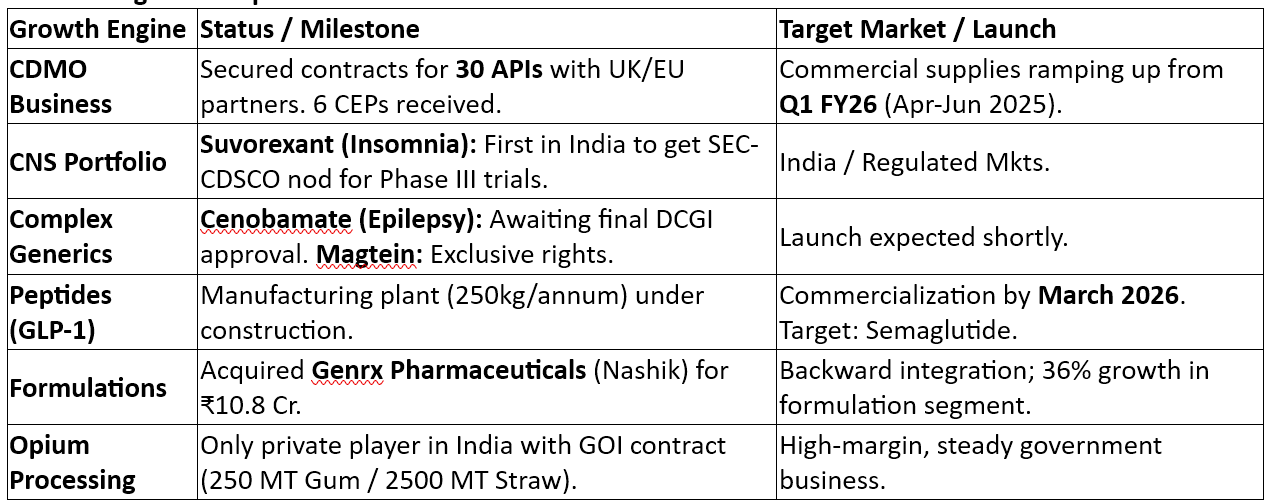

Acquired Genrx Pharmaceuticals Pvt. Ltd. (for 10.8 crores) to enhance in-house formulations manufacturing across allopathic, nutraceutical, and natural products — strengthening backwards integration, product portfolio, and operational control.

-

The Company has secured CDMO contracts for 30 APIs with UK/EU partners. During FY25, it received 6 Certificates of Suitability (CEPs), enabling commercial supplies to begin from Q1 FY26 in regulated markets. This shows the scale up in the topline and bottomline both, while it remains in a sweet spot for the tariffs, as they are growing by securing contracts for Europe and the UK and not the USA.

-

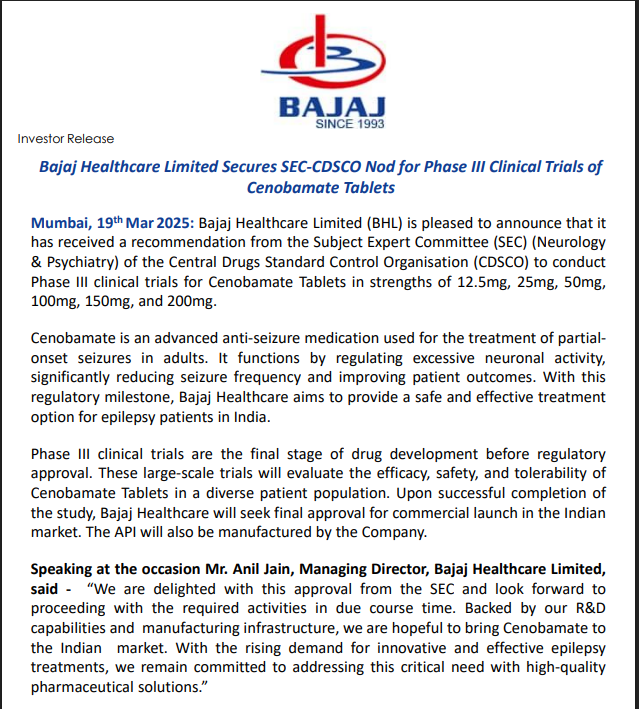

Centobamate has received a favourable SEC recommendation and is now awaiting final approval from the DCGI, which is expected any time soon, marking a key step toward market introduction of this complex generic. Showing the capabilities of how it is evolving as a company is creating new and innovative drugs.

-

Magtein to be launched next Quarter, which will be another trigger to bottomline and topline expansion, while it has the exclusive rights to sell and distribute the product. The market for the product has a good TAM.

-

It has also successfully launched Pimavanserin in India through collaborations with a few pharmaceutical companies, becoming one of the early movers in India for this differentiated CNS molecule.

Commenting on the results, Anil Jain (MD) said in the Investor PPT:-

He talked about the turnaround while swinging back to profits and long-term creation. Talked about the operating leverage and the efficiencies (As it continues to scale up operation, we will see more operating leverage coming into play), One of the key developments he mentioned is the acquisition of Genrx for scaling up the business which will lead to expansion in manufacturing facilites while the company continues to build innovative products in CNS (Central Nervous System). Pimavanserin and the progress of Cenobamate show how Bajajhcare is evolving. After securing partnerships, they aim to become a trusted global pharma outsourcing partner.

Disc:- Invested so my views can be Biased, i remain a long term holder of the same. I am not SEBI REGISTERED these are my personal views.

7 Likes

Where their Opium Processing revenue breakup?

Any information about exodus of directors from the board?

1 Like

Bajaj Healthcare June exports up 174% YoY and 88% MoM

Source :- Arihant Capital

3 Likes

- Bajaj healthcare continues to show growth (YoY) at 12.5% while it saw a degrowth QoQ.

- The EBITDA margin saw a marginal improvement.

- PAT from the continued operations continue to scale up with showing a growth of 50% YoY and 5% QoQ. PAT margins has also improved from 6% to 8.1%.

- PAT from the discontinued operation continues to go down showing disposing the business and contiue to focus on core business which are generating good returns.

- Overall Profit saw a increase of 65% YoY and 6% QoQ. The Net Profit margin also improved from 5.4% to 7.9% showing a improvement of 250 bps.

- The domestic business continue to show degrowth as the management has emphasised to focus on exports as a avenue of growth due to better margin and price realisation. The API exports business grew by 68% YoY and 28% QoQ (as the magnesium manufacturing ramps up). Exports business now accounts for 53% of total revenue up from 23% a year ago.

- The formulation business is also showing a good growth Engine leading to 41% YoY increase while there is a decline of 1% QoQ.

- About the Opim business (from other source)

Expecting opium business at Rs 30 cr in FY26 vs Rs 40 cr in FY25 (conservative estimate for FY26)

The opium business works at 60% gross margins and negative working capital.

Commenting on the Results the management said :-

Segment-wise, our API export business delivered standout growth of 68.4% YoY, supported by growing demand in regulated markets and the ramp-up of commercial CDMO supplies. Formulations saw 41.1% year-on-year growth, led by deeper market penetration and new strategic partnerships. Due to pricing headwinds in the domestic API segment, the company has strategically realigned its portfolio towards value-added exports and differentiated molecules to reinforce growth and profitability.

On the new approvals :-

Management is also pleased to report that during the quarter, we received three new CEP approvals and

one ASMF approval from European regulatory authority, further strengthening our position in

regulated EU/UK markets. Following product approvals, validation batch supplies have

commenced for a few molecules under CDMO agreements. In parallel, five DMFs were filed

with the UK MHRA to enable future commercial supply and regulatory compliance. To date,

we have filed a total of nine CEPs, out of which seven have been approved. Furthermore, four

additional CEP filings are in process.

Validation batch supplies have commenced for a few molecule under CDMO agreements which is a keu thing to note here.

The company is awaiting DCGI approval to initiate phase 3 trails (another good point).

The company also has send magtein validation batches so from Q3 they target a commercial laucnh which is another earning growth trigger.

At the end the company is exporting to EU so it remains averse to the tarrif risk.

1 Like

Q2FY26 result was good, still market is reacting negatively, Any reason?

Basis 9M nos: U-Shaped recovery from the post-Covid slump

Not sure why not getting re-rated!! - is there Mgmt. concerns? Learned investors inputs will help

Operating Cash Flow Trend

“What Went Wrong vs. What Right Now”

Growth Engines & Pipeline Tracker

3 Likes

Excellent analysis. Keep accumulate at lower price. BHC ka time ayega.

2 Likes

For long term investing, i ike new plans of BHL but have few questions

1-Why trade receivables of older than 2-3 years & More than 3 year are very high? (note no. 8.1)

2-Why Assets Classified as held for sale amount is high? (note no. 3.1)

3-Any details on Other Receivables? (note no. 10)

4-Any details on Balance with Statutory Authority? (note no. 11)

5-Anyone have interview / visit experience of next gen of BHL managment?

6-Anyone have guidance / projection of launch of CNS, onco and GLP1 products in EU or USA?

If someone have ideas or predictions or understanding of these issues, please help me to decide.

Thanks

Very critical points but since there is no interaction with Co, don’t have clear answers to these. Below are what I could gather:

On Receivable:

- The above 1yr surge of debtors happened in FY24, primarily driven by a single major defaulting debtor. This debtor procured materials to supply to a US-based MNC, but the supplies were deferred due to pending KYC and sample approvals. Because they couldn’t complete their sale, they failed to pay Bajaj Healthcare, causing a massive chunk of receivables to age past 12 months.

- Above 1yr debtors was 73 Crs in FY24, which has come down to 66 Crs in FY25 (my calculation).

Excerpt from FITCH rating rational

- Co has been providing for these as a small expected credit loss YOY, as on H1FY26, this amount stands at 8.59 Crs.

- Though there is no clarity on ageing wise data for H1FY26, there is a ~20 Crs receivable reduction as on H1FY26.

- Also note that with recent successful conversion of warrants issued, cumulative fresh equity raised by the company since FY24 stands at 205 Crs. So liquidity shouldn’t be a concern

Assets held for Sale:

In FY24, co decided to sell four discontinued units located in Tarapur (Maharashtra) and a vacant industrial land parcel in Dahej (Gujarat), still pending execution, i think

Balance with Statutory Authority

Seems to be under litigation refund of Input Tax Credit, still pending

3 Likes