I saw there is an existing new thread on Bajaj Healthcare which is closed. The person who started is not updating the same so that it can be opened, I guess. Since I intend to provide more information I am hoping this one remains open. Alternatively I can move this information there if that thread is opened

Would request @vikas_sinha who has been holder of Bajaj Healthcare for a longer time to add anything if I have missed

What does the company do?

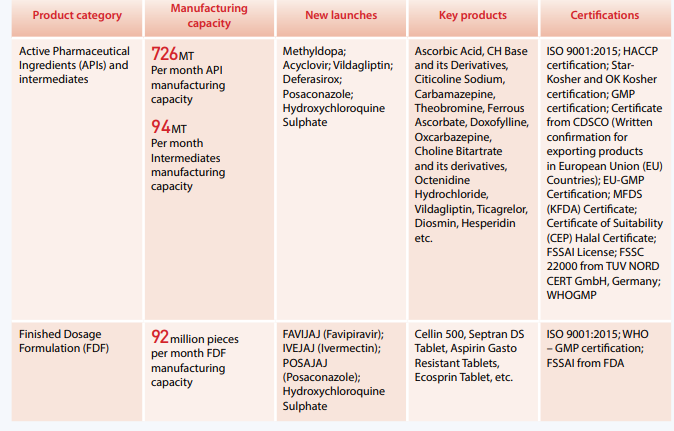

- Incorporated in 1993 Bajaj Healthcare Limited is manufacturer of APIs, intermediates and finished formulations. It is one the emerging global manufacturers of high-volume high-value pharma products. Company has a presence in 51 countries globally

- It got listed on the stock exchange, on BSE- SME Platform in 2016 and migrated to the BSE mainboard in 2019. It is not listed on NSE yet.

- APIs: Ascorbic Acid, CH Base and Its Derivatives, Citicoline Sodium, Carbamazepine, Theobromine, Ferrous Ascorbate, Doxofylline, Oxcarbazepine, Choline Bitartrate and its derivatives Octenidine Hydrochloride, Calcium Phosphoryl Chlorine Cloride

- Finished Dosages: Cellin 500, Septran Ds Tablet, Aspirin Gasto Resistant Tablets and Ecosprin Tablet, among others.

Investor PPT

Thesis

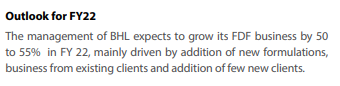

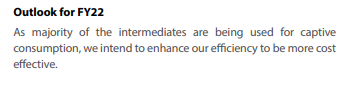

- Company is trying to evolve product mix from APIs to FDFs. FDF sales contributed to 10% of revenues in FY21 v/s 6% in FY20 v/s 2% in FY19. More the contribution from FDFs higher the margins

- Company is to increase presence in the key therapeutic areas such as pain management, anti-malaria and tapeworm infection in the API segment which are high on value and low on volume.

- Focused on regular new product addition to portfolio to support commercial launches on patent expiry

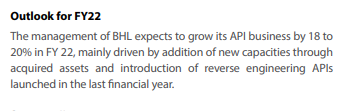

- Guidance for FY22: Management believes it can grow revenues 18 to 22% for FY 22, driven by addition of new capacities through acquired assets, products related to Covid-19, generics. Margins will moderate in some segments.

Market Cap and Valuations

- Company has a market cap of (Rs1272crs)

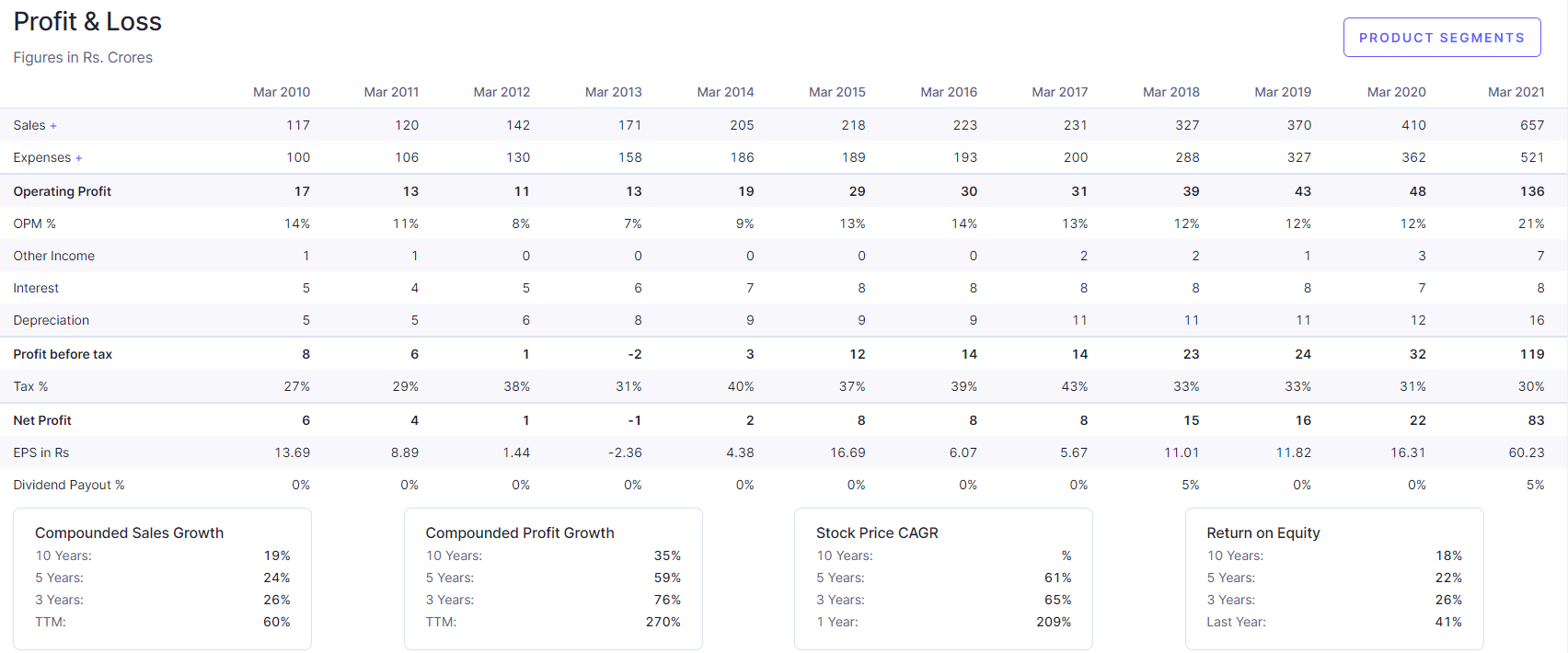

- FY21 profits Rs83crs. Stock trades at a P/E of 15.3x FY21

Key shareholders in the company

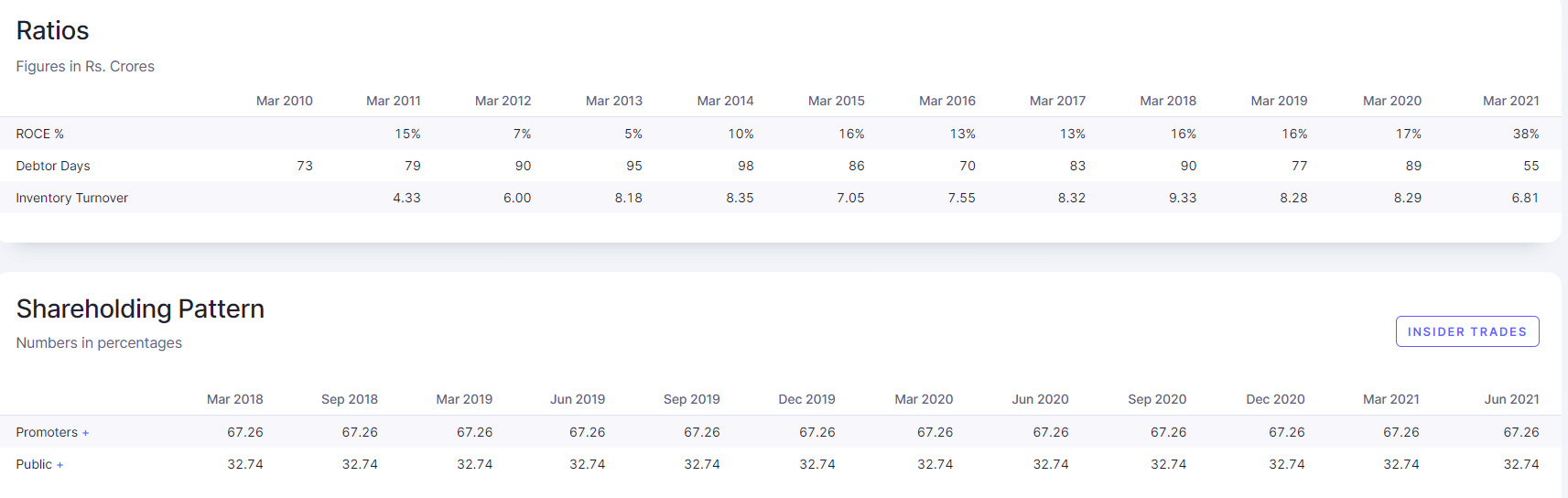

- Promoters hold 67.26% of the company

- No institutional holding in the company. Did not notice any PMS or AIF holding it also

Key Negatives

- Its another API company which is potentially prone to competition

- Not enough information if it has any competitive advantages or just got lucky last year due to Covid related drugs

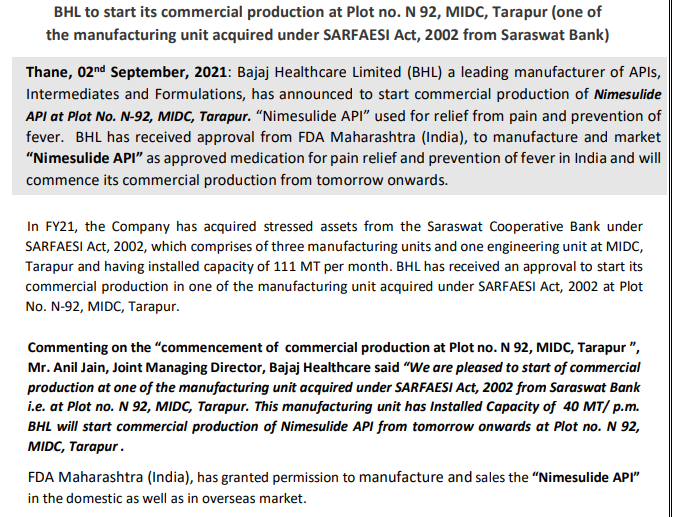

- Recent fire accident This is to inform you that there was a fire accident at one of our unit situated on Plot no. 1717/ 1718, GIDC Panoli, Tal - Ankleshwar, Dist. - Bharuch, Gujarat - 394116 in the first half today, i.e. July 11, 2021. Due to prompt action by alert staff the fire was brought under control and no loss or injury to human life has occurred in the incidence. However, the Company is ascertaining the extent of loss and has already informed to the Insurance Company as the entire factory and goods therein are adequately insured. Company is taking steps to ensure normal operation at the plant at the earliest. Any further material development in this regard will be updated.

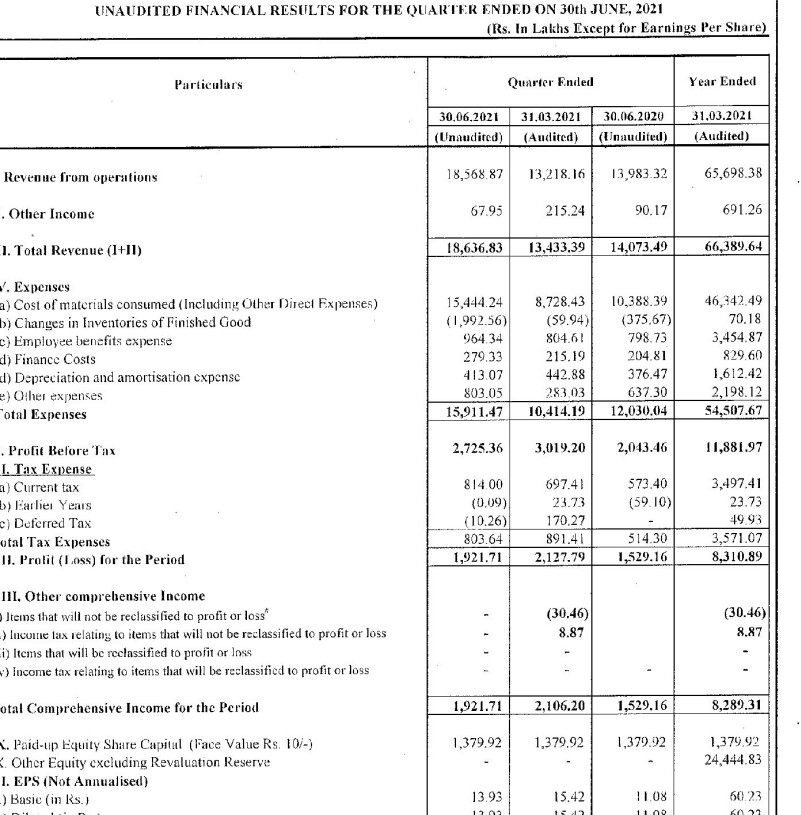

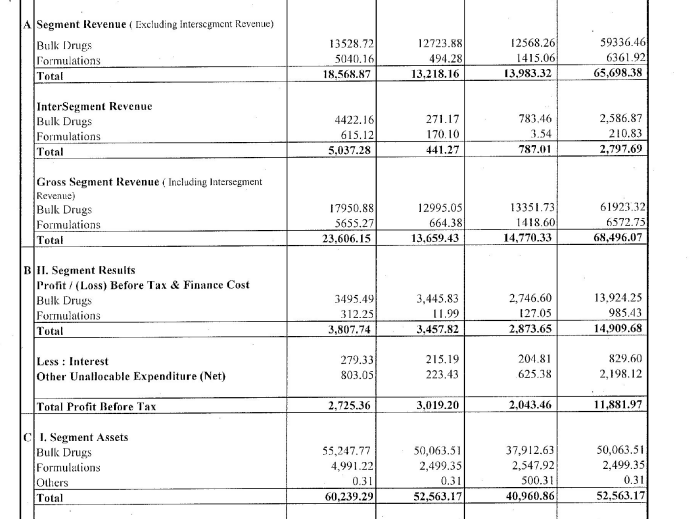

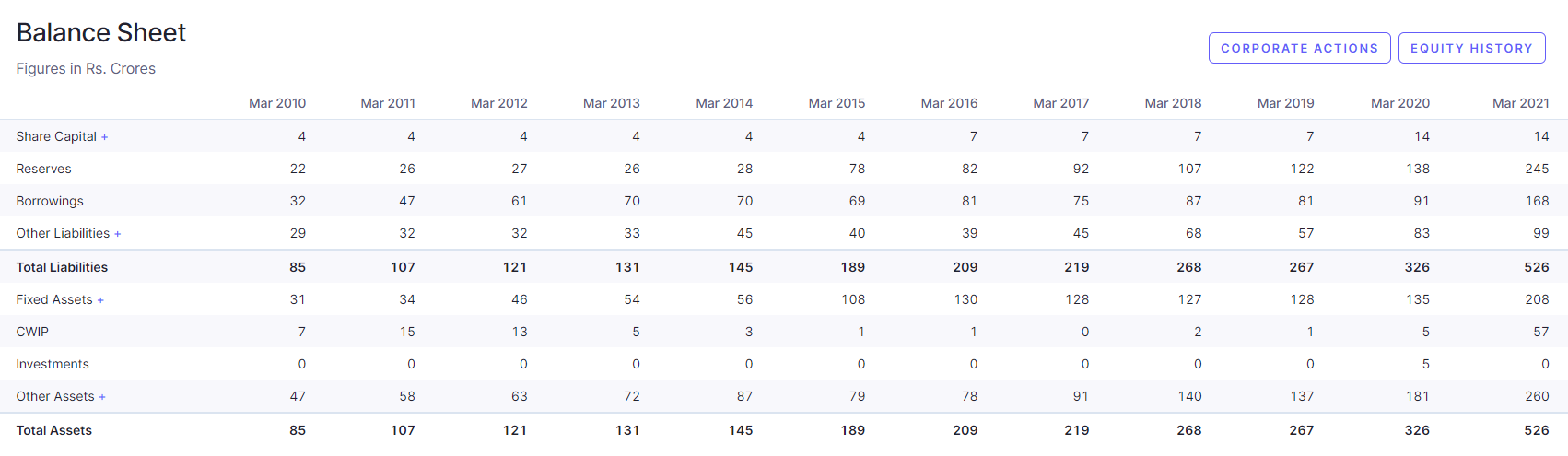

Financials

Other news

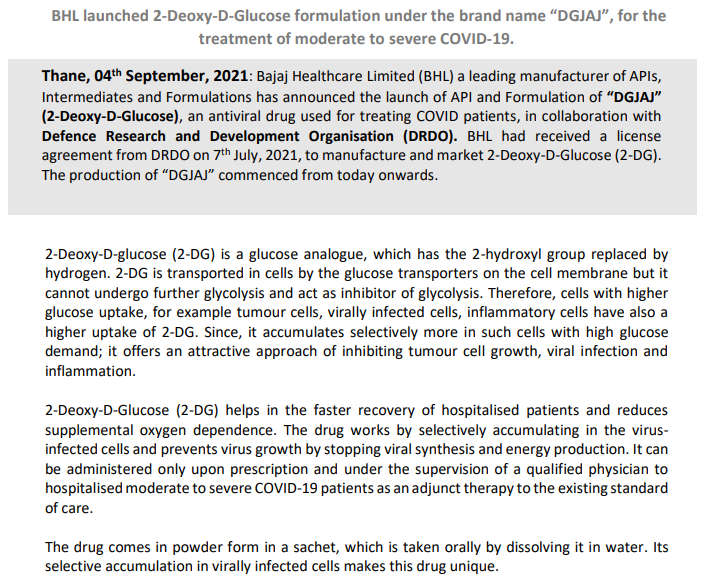

July 7: Bajaj Healthcare Limited (BHL) a leading manufacturer of APIs,

Intermediates and Formulations, has received a licence from DRDO to Manufacture and Market

of “2-Deoxy-D-Glucose” (2-DG) as approved medication for the treatment of COVID-19 patients.

June 28: Bajaj Healthcare Limited (BHL) a leading manufacturer of APIs, Intermediates and

Formulations, are pleased to announce that it has moved the Indian Patent Office requesting to grant a

compulsory license for manufacturing & supply of Covid-19 drug “Baricitinib” (API and Formulation).

Currently, Eli Lilly and company has received Emergency Use Authorization (EUA) from U.S. Food and

Drug Administration (FDA) for the distribution and emergency use of “Baricitinib” to be used in

combination with remdesivir in hospitalized adult and pediatric patients aged more than two years with

suspected or laboratory confirmed COVID-19 requiring supplemental oxygen, invasive mechanical

ventilation, or extracorporeal membrane oxygenation (ECMO).

May 28: Bajaj Healthcare Limited (BHL) a leading manufacturer of APIs,

Intermediates and Formulations, has announced the launch of “Posaconazole API” used in

treating Mucormycosis (Black Fungus) infection in Covid-19 patients. BHL has received approval

from FDA Gandhi Nagar, Gujarat (India), to manufacture and market “Posaconazole API” as

approved medication for treating Mucormycosis in India and it will commence its commercial

production from 1st week of June 2021.

May 6: Bajaj Healthcare Limited (BHL) a leading manufacturer of APIs,

Intermediates and Formulations, has announced the launch of “Ivejaj” (Ivermectin) an AntiParasitic Drug now widely used in control & treatment for Covid-19 patients. BHL has received

approval from India’s drug regulator, to manufacture and market “Ivejaj” the oral Ivermectin

approved medication in India for the treatment of COVID-19 from 6th May 2021

May 4: Bajaj Healthcare Limited (BHL) a leading manufacturer of APIs,

Intermediates and Formulations, has announced the launch of “Favijaj” (Favipiravir) an antiviral

drug used for treating patients suffering from influenza virus and has proved to be effective over

COVID patients. BHL has received approval from India’s drug regulator, to manufacture

and market “Favijaj” the oral Favipiravir approved medication in India for the treatment of

COVID-19 from 4th May 2021.

Disclosure: Invested