Business and ones circle of competence on that is more important than financial metrics or valuation. Price moves up in accordance with that. A person who understands business buys as he knows the price will follow . Market is a slave of earnings but with a lag or lead. A person who has got conviction will load up. But we retail dont have that advantage fully unlike big investors.

My circle of competence was not higher (than in Bajaj Healthcare) in Indiamart or Affle when I invested in them/ started a thread on them in valuepickr.

Every once in a while one of these leaps of faith don’t work out. The problem of not leaping till you have 100% circle of competence is then you miss out on the 2 out of 3 ideas that worked.

2 Likes

Increased sale of Favipriavir, Hydroxychloroquine and Ivermectin are Covid related I suppose which may decrease in the coming quarters.

At least you started the thread Venkatesh. We all are benefitting from it. I also did not know about the Rice Mill and Condom until i read here. Thanks

2 Likes

Any news…for stock underperformance …market knows more than US…please advise if there is any news that we should know…

2QFY22 results are very poor!

But as per their annual report, by fy 23… company crosses 1000cr revenue

So 50 % growth on top line planned in next 1 yr

Will that be a trigger for any good performance in next 1 yrs or so

1 Like

Any idea what is the meant by - Opiate Processing Business . its market size , peers etc .

The news is dope!

For the profit, is there hope?

- How certain are we that this opium processing will really result in profit?

- Having Govt. as a customer has its problems

- It is good to notice that management is exploring new avenues

- They certainly overestimated its business guidance for FY22 surfing on the COVID wave…and that shows their unreliability

Disc: Tracking

1 Like

The q1 result seems to be very poor. I do this company conduct concall? I couldn’t find anything and anyone has any idea what is the guidance?

Bajaj Healthcare’s news report of receipt of EIR with No Action Initiated and zero 483

1 Like

Hi, I did some work on the name as there were quite a few developments over last 12 months using various Articles by Moneycontrol, Mint, Government sources and TV interviews by management.

Developments over last 12 Months:

-

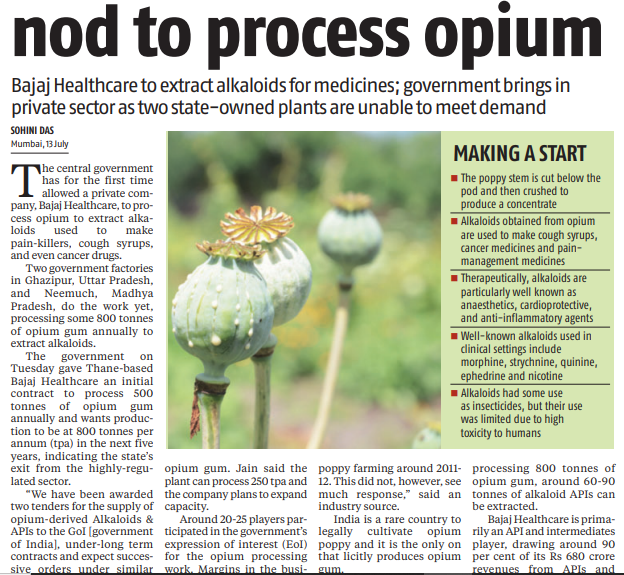

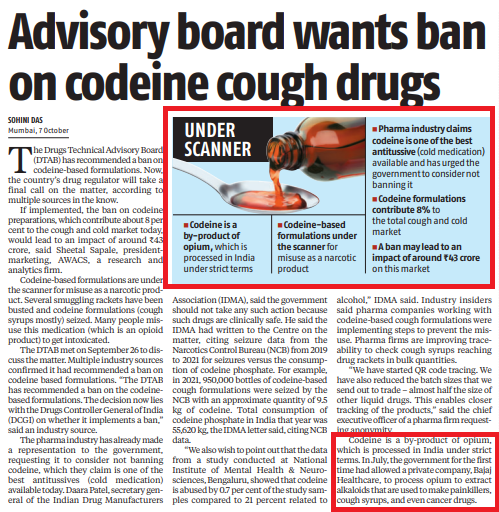

Opium Business foray partnering with the Government of India. Can be a huge opportunity considering the end usage is in pharma products like cough syrup, medicines, pain killers, Cancer related treatments. On the flip side, key risks come on Receivables and Pricing for the processing.

-

EIR USFDA Approval, foray into US.

-

Guidance and Bajaj Healthcare Outlook: ~900-1000Cr Revenue in FY24 and ~1,500Cr Revenue by FY25 with 16-20% Margins. In FY23 Company did ~670Cr of Revenue with ~16% Margins in FY23.

**1) Opium Business**

• Government has provided the tender for the first time for production of Alkaloids. There were 22 participants who applied for it and Bajaj Healthcare was selected.

o Company Received 2 letters of Award in July 2022, from Government of India:

- To manufacture Alkaloids & APIs from processing of 500 MT of unlanced poppy capsule along with Straw per year.

- manufacture Alkaloids & APIs from processing of 100 MT of Opium Gum per year.

o Company has constructed alkaloid extraction plant at Gujarat with extraction capacity of 2500Mt of Poppy Straw & 300 Mt Poppy gum / year.

o What is poppy straw: Poppy straw is crushed poppy capsule or poppy husk. It is what remains after the poppy seed harvest, that is, the dried stalks, stem and leaves of poppies grown for their seeds.

**But why Privatized (Reference: Finshots)?**

1) There’s the pollution problem.

There are two opium processing plants, run entirely by the government.

* One in Neemuch in Madhya Pradesh is over 85 years old.

* Other one in Ghazipur, Uttar Pradesh is over 200 years old.

* They’re in desperate need of a tech upgrade. And they’re not exactly having the greatest impact on the environment.

2) Issue with pricing.

-

Farmers have been complaining about their compensation. They argue they are being paid a pittance for their crop while the going rate in the grey market continues to be at least 30–60 times higher. They want more parity.

3) Problem of efficiency — specifically related to harvesting methods. In India, alkaloids are typically extracted using something called lancing. -

It’s a manual enterprise. Highly skilled farmers make incisions on the pods to draw out the gum. Even the Central Bureau of Narcotics (CBN) calls it a “precise art”. But it results in leakage. That is, farmers divert some of the output to smugglers in a bid to make more dough.

-

But other opium-growing countries like Australia have found a far better way to do this by using something called the concentrated poppy straw (CPS) extraction method. Instead of manually slicing the pods, the entire plant is sent to the processing unit for extraction. The end result is a higher alkaloid output.

-

Despite being the biggest producer of legal opium, we’ve had to import at least 30% of our Codeine needs in the past years and that’s not something we can brag about.

**Industry Economics of Opium/Alkaloids:**

o It’s a highly regulated market in India, which is over Rs 1,000 crore. The government is processing 500 to 700 metric tonnes, but the demand is more.

o To minimize the imports, it would be an opportunity for both government and private players to cater it. So, whatever the shortfall, a private company can bridge that gap is what Bajaj Healthcare stated.

o India is one of the few countries internationally permitted to cultivate opium poppy for export. Two types of narcotic raw material can be produced from opium poppy (a) Opium gum; or (b) concentrate of poppy straw (CPS).

o Until 2021, only opium gum was being produced in India. The Govt. of India has now decided that CPS production should be commenced in India. In this regard, the Govt of India in the Opium Policy 2021-22 has allowed licenses to cultivators for production of unlanced Poppy Straw to be used in manufacturing of alkaloids using CPS technology.

o The Central government’s move came as a part of its initiatives to boost the yield of alkaloids used in various drugs.

o Forming CPS from Poppy Straw: Poppy straw is first pulverized and then washed as many as six to ten or more times in water and/or various acids and other chemicals, to produce concentrate of poppy straw (CPS). After drying the concentrate becomes beige or brown powder. It contains salts of various alkaloids, and can range from 9 to 30 times the morphine concentration of poppy straw.

o For crop year 2021-22 Central Bureau of Narcotics has distributed around 10% of total licences for cultivation of poppy specifically for CPS. Around 7500 cultivators have tendered nearly 400 tonnes of poppy straw in crop year 2021-22. This also provides opportunity to CCF/GOAW’s to invest in R&D and be a torch bearer to develop an indigenous and efficient process for alkaloid extraction from CPS and make India “Atmanirbhar” in alkaloid-based medicines.

• How will private players reduce India’s import dependency in this segment?

o Bajaj Healthcare statement: The government has told us to do a minimum of 100 metric tonnes of opium gum and 500 metric tonnes of poppy capsules. We will start with a small volume of opium gum. As it gets going, we can process up to 800-900 metric tonnes of opium gum for the government annually. If we are through with the 100 tonnes, then we are sure that the government won’t require any alkaloid material imports.

• Bajaj Healthcare’s Role in this business as Stated by them:

o The government will provide us with the poppy straw. We will convert it through CPS (concentrate of poppy straw) technology into different kinds of alkaloids. These alkaloids will be given to the government of India, which will sell it to the sector concerned. We will get the processing charges, which have already been defined by the government of India.

o To minimize this import, the government felt that it would be an opportunity for both government and private players. So whatever the shortfall, a private company can bridge that gap.

Financial Economics of the Business:

o Price of Poppy Straw: 1500-3000 INR/kg.

o It will be a negative working capital business, raw material to come from government.

o The margins on opium processing will be 20-25% of EBITDA.

o This new segment is expected to contribute Rs 25 to 30 crore by the financial year 2024. Commercial operations are expected to begin in the December quarter of the current financial year.

How Bajaj Decided to enter this business?

o As stated by Bajaj Helathcare: This was an idea that we got from Pfizer – we have a good rapport with the company. The company uses alkaloids in a product named Corex. We enquired about it, got all the details. It looked like a good opportunity with high margins. So we entered the opium-processing business.

• Annual licensing policy for crop year 2023-24

o As per the general conditions enshrined in the policy, nearly 1.12 lakh farmers in these three states are anticipated to be given licenses, with inclusion of 27,000 additional farmers over and above the previous crop year. The number of opium cultivators who would be eligible for getting license are nearly 54,500 from Madhya Pradesh, 47,000 from Rajasthan and 10,500 from Uttar Pradesh. This is almost 2.5 times the average number of farmers given licenses during the five-year period ending 2014-15.

o Key point is demand is good: This increase is with the objective to meet the increasing demand for pharmaceutical preparations for palliative care and other medical purposes, both domestically and internationally. It would further ensure that the alkaloid production meets domestic demand as well as the requirement of the Indian export industry.

o The system of licensing for unlanced poppy was started in a modest way from 2020-21 and has been expanded since then. Central Government has augmented the capacity of its own alkaloid factories.

• Some legalities:

o https://static.pib.gov.in/WriteReadData/specificdocs/documents/2023/sep/doc2023914251601.pdf

**2) EIR Approval with Zero 483 Observations**

• EIR received with Zero 483 from USFDA.:

o Received in Sep’23 and Inspection carried out in Nov’22.

o The receipt of the EIR also opens up the opportunities for filing companies own Drug Master Files with the USFDA as well as CDMO opportunities that company is eying with various customers across the globe.

o Company had historically been supplying certain API & Nutra which do not require EIR to US. But prescription-based drugs require DMFs for which USFDA compliance is necessary.

Key point: Now DMF filings only happen when you already have customers, hence company is confident about delivering.

o One product will go to big pharma company for Para-4.

o Company has lined up 10 DMFs to be filed in US in FY24.

o Bajaj is strong in EU markets and has several DMFs there. Now with EIR, company is looking to enter US with product patents will be going off between 2024-26.

**• Guidance by Bajaj Healthcare:**

o FY25 Revenue: 1500Cr, management believes company might over deliver with success in Opium business.

o FY24: 900-1000Cr, driven by new product sales from US and Domestic Opium business.

o The management plans to increase its exports growth of 15%-20 % for FY24.

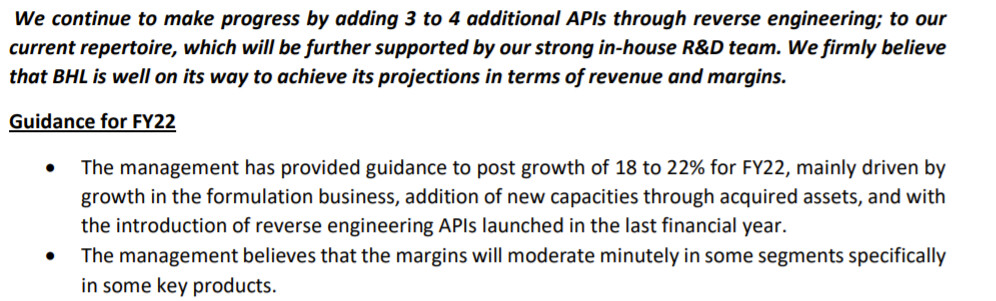

o The management expects that the EBITDA margins would be in the range of 16%-20% for FY24, mainly driven by growth in the formulation business and with the introduction of reverse engineering APIs launched in the last financial year.

o On the business front, we are expecting to launch 3-4 off-patented molecules in the API segment in FY24.

• Sale of Tarapur plant to bring in some cash: Might be helpful to service Debt.

o It was no upto FDA standards and no expansion possible.

o Company will be hiving out this facility by 2023 end. Good amount of cash to come in.

o Company has Announced the sale/disposal of undertaking/unit(s) situated at plot no. N-92, L-9/3 , T-30, MIDC Tarapur, Taluka- Boisar, District Palghar, Maharashtra and vacant industrial land situated at plot no. D-2/CH/42 & D-2/CH/43 Dahej industrial area, GIDC, Bharuch, Gujarat (which were acquired under SARFAESI ACT, 2022 from Saraswat Bank) and plot no.E-62 and E-63 MIDC Tarapur, Taluka Boisar, District Palghar, Maharashtra.

o The Company has reported loss before tax from Discontinued Operations of Rs. 568.65 Mn. out of which onetime loss from asset held for sale amounted to Rs. 435.89 Mn which was derived by the difference of the fair market value valued by Independent Valuer and book value and balance loss was operational loss from above said units.

o The operations at the said units at Tarapur currently generated a negative annualized EBITDA and after sale/disposal of the said units will enhance an EBITDA margin and profitability improvement in the existing business.

o Revenue generated from plant in FY23 was ~27Cr

**Other Points:**

o Company hired Dr. Mohammed Jaweed Mukarram, as an Advisor in the Research and Development division.

o His illustrious career includes significant roles at esteemed organizations, such as Sr. Associate Director at Wockhardt, where he spearheaded the Chemical Research Division. Over the years, he has made a mark in the industry by filing a noteworthy 156 patent applications. His expertise has led to the successful handling of over 70 bulk drugs and intermediates, boasting an impressive 35 US Drug Master File (DMF) filings to date.

• Promoter has bought ~0.23% stake since Mar’22.

o Latest deal was by Sajankumar Rameshwarlal Baja at Rs 445 per share for total shares worth of Rs 2.5Cr.

• A negative with Bajaj Helathcare: Over-guiding, Under Achieving

o Company guided for ~20% growth in FY22 but the Revenue was flat in FY22.

• Story of Government de-regulating Opium: The opium high for India’s private sector

Thanks, Looking for some views on this and the Company.

8 Likes

Hello can someone share their views why stock is in downward trend

Hi Folks, anyone tracking the company?

It is raising huge fund raise of 140crs (on marketcap of 900crs) and some prominent investors are expected to participate. Such big fund raise on such small marketcap is a significant event

They are going to reduce debt significantly, discontinue loss making operations, and have hired an industry veteran with deep knowledge and conencts as CTO. They have signed CDMO agreements in Feb’24.

Guiding for 620crs revenues and 21-22% EBITDA margins in FY25. With debt reduction, interest costs will cone down significantly and improve PAT margins.

3 Likes

Long term debt is only 65 Crs. Their short term debt for working capital requirement is high! How are they going to reduce their working capital cycle? Working capital days are 254 right now. It used to be around 60-70 few years back. Will shutting down loss making businesses help with this ?

1 Like

Bajaj Q2 Investor release.pdf (558.5 KB)

Company is working in the same direction

Debt was reduced by 150 Cr and impact will be coming in the Q3.

1 Like

Company entering into a definitive CDMO contract with UK/EU based companies for 15 new APIs.

Speaking at the occasion Mr. Anil Jain, Managing Director, Bajaj Healthcare Limited, said “We are

delighted to share this development which reinforces the capabilities that we are building in terms

of cost-effective route of synthesis in our R&D and the expansion of manufacturing capabilities,

mostly at our USFDA, EU and now TGA, Australia approved site located at Block No. 588, SavliKarachiya Road, At & Post: Gothada, Tal. Savli, Dist: Vadodara, Gujarat. The company is likely to

enter into few CDMO deals with clients in Australia, New Zealand and South Africa, after the

approval of the site by the TGA.

5 Likes