Hi. So in terms of revenues and PAT, what is the breakup of various subsidiaries ?

The annual report for FY 2019-20 is published:

http://karisma.kfintech.com/files/BFSL_Annual_Report_2019-20_INDI.pdf

Notes:

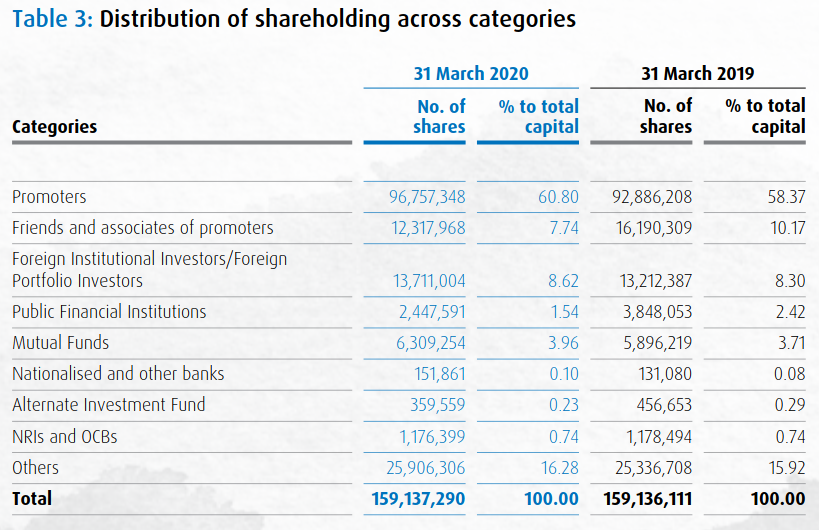

1. Shareholding structure

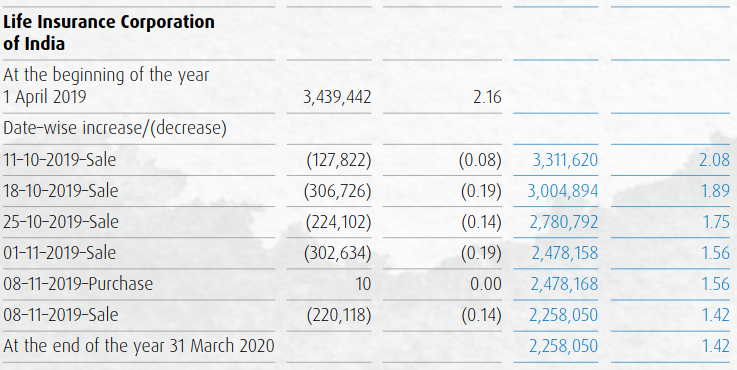

2. LIC brought down its stake

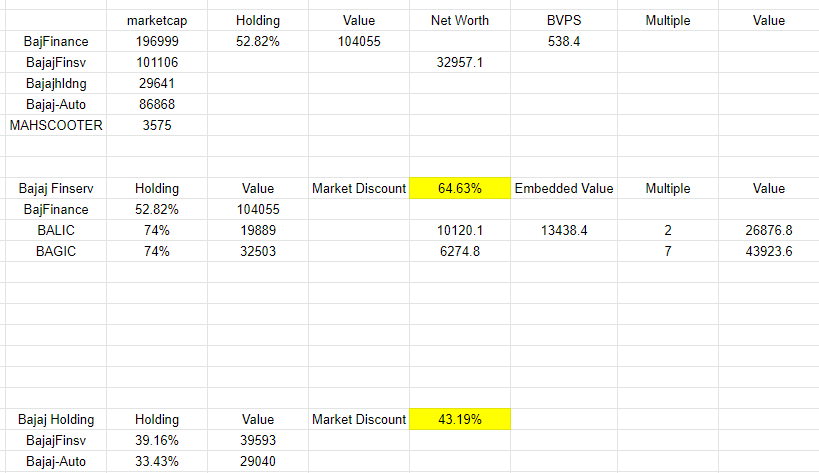

Great thread by Jeswin (j4jeswin) on twitter on Bajaj Finserv’s Valuation Anomaly. https://twitter.com/j4jeswin/status/1265784168790675456

Holding companies trading at a discount would be one thing but this seems to be a case of value unlocking pending in case of Bajaj Finserv. Thoughts ?

Guesstimate on the holding company discount applied by the market. Bajaj Finance value is taken on market cap. BALIC is based on FY20 EV and an EV multiple of 2x. Conservatively went with lower multiple from listed peers because they seem to have lower investment book leverage. They are handling lower AUM with higher net worth to listed peers and this is affecting profits and ROE.

You can tweak the multiples as per your liking.

BAGIC value is based on net worth, it is very similar in performance to ICICI Lombard which trades at ~9x BV. I used 7x multiple.

Now to come to the debate of what an ideal holding co. discount should be, this data is a single data point and we would need to track it for a few quarters to see how the hold co. discount moved in the past. Even then it could just be investor sentiment driving a particular discount range in the medium term. The discounts expand in bear markets and reduce in bull markets.

2 Likes

Some notes on Bajaj Finserv -

Bajaj Finserv holds 52 pc stake in Bajaj Finance and 74 pc each in Bajaj Allianz General Insurance and Bajaj Allianz Life insurance…both unlisted.

Bajaj Finance is widely discussed on this forum. So, I ll try and highlight some imp performance parameters of the Insurance companies.

GWP, AUM and PAT reported by Bajaj Allianz Life Insurance from FY 16 to 20 are as follows -

FY 16 FY 17 FY 18 FY 19 FY 20

GWP…5897…6183…7578…8857… 9600

( Rs Cr )

AUM… 44107… 49270… 51970… 56620…56085

( Investments )

PAT … 879 cr … 826 cr… 716. cr … 501 cr … 450 cr

Figures for Bajaj Allianz General Insurance company are as follows -

FY 16 FY 17 FY 18 FY 19 FY 20

GWP … 5900… 7687… 9486… 11097… 12780

AUM … 9211… 10829… 14822… 17236… 18745

( Investments )

PAT …564 cr… 727 cr… 921 cr… 779 cr… 998 cr

Covid impact on Insurance companies -

Since the insurance companies hold investments in listed stocks, the sudden drop in Indian Stock Mkts due Covid-19 has led to insurance companies realise MTM pre tax losses of 768 cr.

There has been in rebound in the performance of the two insurance companies, as is evident from Q1 results.

GWP(growth) AUM(gr) PAT( gr )

BAGIC… 2289(- 19 pc)… 19611(12pc)… 394(88pc)

( Rs Cr )

BALIC… 1699 (-7pc) … 60968 (5pc) … 130(111pc)

Clearly, when it comes to profitability…both the insurance subsidaries are showing a recovery post the MTM losses due to the Mkt meltdown in Q4.

Key things to monitor - recovery in the Bajaj Allianz life Insurance business.

Will keep posting more info, as I keep studying the company.

Disc : invested.

1 Like

Are we saying it is better to invest in bajaj finserve than Bajaj finance…

It appears to me Bajaj finserve is more diversified business with the best of both the world’s …NBFC & Insurance…

and Bajaj finance is only NBFC

1 Like

I would only say that I kind of like Bajaj Finserv.

Bajaj Allianz geneneral insurance can be compared to ICICI lombard.

BAGIC clocked PAT of aprox 1000 cr vs 1194 cr for Icici Lombard for the FY ending Mar 2020.

In FY 16, BAGIC’s PAT was 564 cr vs 505 cr for Icici Lombard.

In Q1 FY 21 BAGIC has reported a PAT of 394 cr vs 398 cr for Icici Lombard.

I ll post separately about other parameters like solvency ratios, combined ratios etc.

Now Icici lombard is valued @ 45 times its FY 20 earnings.

Valuing BAGIC at 45 times would make it a 45000 cr company with Bajaj Finserv’s 74 pc stake valued at 33000 cr.

Bajaj Allianz Life Insurance Company reported a PAT of 450 cr for FY ending Mar 2020.

Sbi Life is valued at 60 PE, HDFC life at 90 PE.

Even if one were to give a 30 times earnings multiple to BALIC, it would be valued at 13500 cr with Bajaj Finserv’s 74 pc stake at 10000 cr.

Adding the two - 43000 cr.

Plus the 52 pc stake in Bajaj Finance at current mkt price- Rs 114000 cr.

Combined value - Rs 157000 cr vs current Mkt cap of Rs 104000.

So…there is some discount here.

Also, going fwd…the profitability of the two insurance companies is likely to improve as the COVID related one offs are not likely to be repeated. The same is evident from the Q1 results as well.

Plus the spreading of risk due to the cushion provided by the non lending Insurance arms.

So…its an interesting story, I would say.

Disc: invested.

Will add more on corrections / improvement in performance of BALIC.

5 Likes

One of the factor that you are missing is the bonding company discount.

This discount has always been there. At times it increases to 50%+as well.

1 Like

I was also wondering instead of taking three different entry in nbfc, general insurance and life insurance why not take entry in bajaj finserve as it also serves the same.

But same time i also think that it will always be discounted and real benefit will only be on value unlocking.

Does any one has any idea when value unlocking may happen.

1 Like

Thats true. Holding company discount is always there.

However, Baj Finserv’s holding in Insurance Arms is at 74 pc…thats preety high.

It provides a unique exposure to one of the best NBFC and General Insurance companies in India. Once life Insurance ( already doing a descent job ), starts to do better, the stock may get re rated.

Over time, Insurance arms are likely to be listed at high PE multiples.

1 Like

If I remember correctly, management told that they have no plans to list insurance subsidiaries anytime soon.

Regardless, listing of insurance subsidiaries is unlikely to unlock much value for Bajaj Finserv shareholders as in all probability they will go for IPO instead of demerger, and in that process the shareholding percentage is likely to go down as well.

Lastly, I find the scepticism towards holding discount a bit astonishing. The only disadvantage of holding company is that the discount may broaden in occasions but there are greater chances of the discount remaining the same or narrowing. In the later cases one gains with the growth of the underlying companies.

Nice management interview

4 Likes

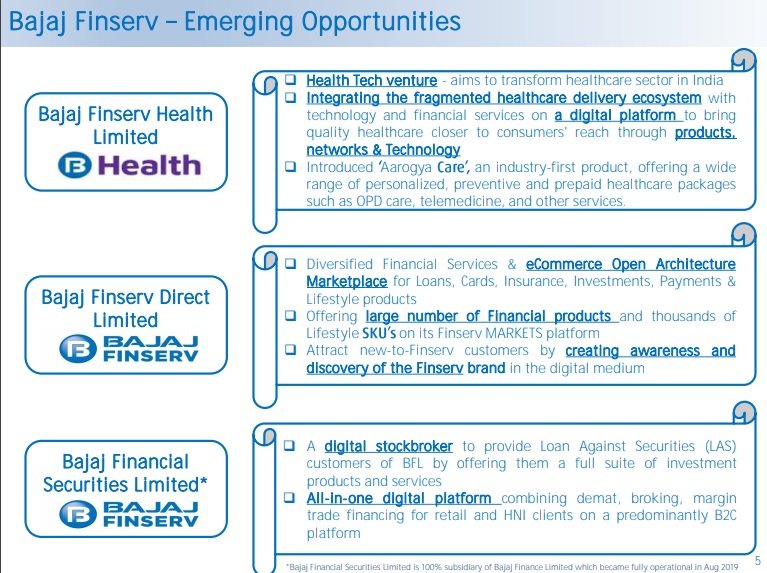

Extract from latest investor PPT

Extract from FY20 Annual Report

“Bajaj Finserv Direct Ltd. (BFSD) was set up as a wholly-owned subsidiary of the Company in FY2019, with the long-term goal of creating a digital marketplace which offers the full range of financial products including loans, life insurance, general insurance, mutual funds, investments, payments and selected e-commerce. In the course of FY2020, BFSD launched its platform ‘FINSERV MARKETS’, and the initial response to it has been encouraging.

During the year, the Company incorporated a wholly-owned subsidiary called Bajaj Finserv Health Ltd. Over time, this entity is expected to create a digital ecosystem in the healthcare segment connecting customers with service providers in the healthcare space such as doctors, hospitals, nursing homes, pharmacies, diagnostic centres and the like by offering a complete range of products including financial solutions.”

Do Bajaj Finserv’s these businesses have potential for significant scaleup and meaningful contribution in the long-term?

1 Like

4 Likes

5th July 2024

MCap of Bajaj Finance is 440,000 Cr

MCap of Bajaj FinServ is 252,000 Cr

If I subtract out the 51.34% stake of Bajaj Finance from the market cap of Bajaj FinServ, I am left with about 26,000 Cr.

For 26,000 Cr, you get a 74% stake each in BAGIC (general insurance) , BALIC (life insurance) and the whole of Bajaj AMC.

BAGIC and BALIC have 7.3, 5.8% of the market share respectively. I compared AUM of BAGIC with listed players (ICICI Lombard, HDFC Life) and the premiums written by BALIC with that of listed players (HDFC Life, ICICI Prudential). BAGIC and BALIC if listed independently, for the 74% share, would be at lease 25,000 Cr and 30,000 Cr respectively.

The AMC business just started a year ago, so still pretty small (AUM 10,000 Cr), but growing rapidly. Given Bajaj’s history of incubating comapnies, seeing what they did with Bajaj Housing Finance (100% owned within Bajaj Finance) getting to 1731 Cr PAT within 6 years, I am confident that the AMC business will do well. By the way, the housing finance comapny will get demerged and listed separately by Sep 2025. It should command a market cap of 50,000 if compared to listed peers.

For those who would have be happy to buy Bajaj Finance today, FinServ might be interesting to consider instead. You basically get BAGIC or BALIC for free - that’s 6-8% of India’s general or life insurance business. Not a bad deal. And who know what becomes of the AMC.

6 Likes

There is something called ‘holding company discount’ in India. It’s not as straightforward as you imply. What you know, market very well knows.