Bajaj Finance get advantage of this (Gain market share)?

3 Likes

Thanks for the response Sanjeev

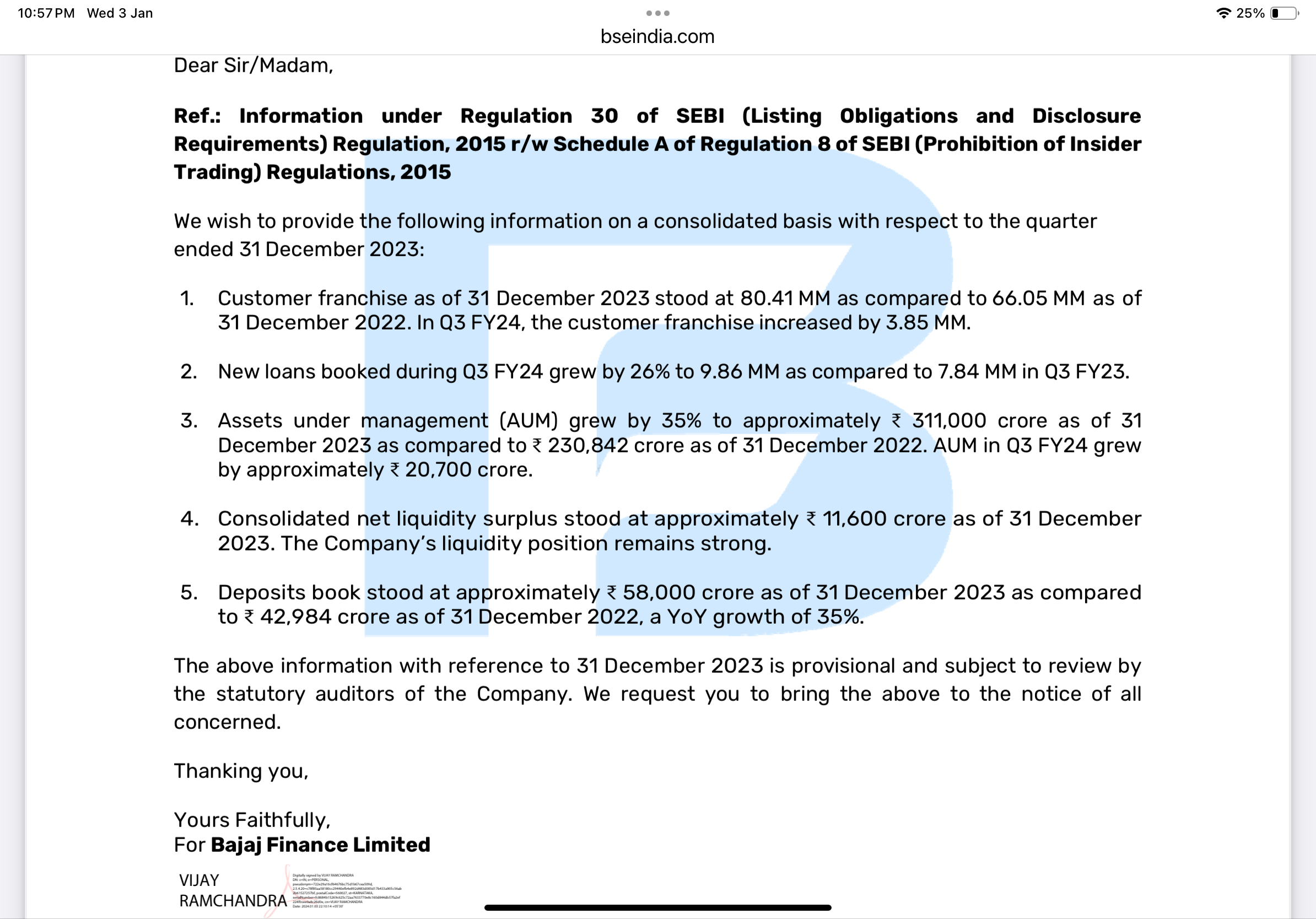

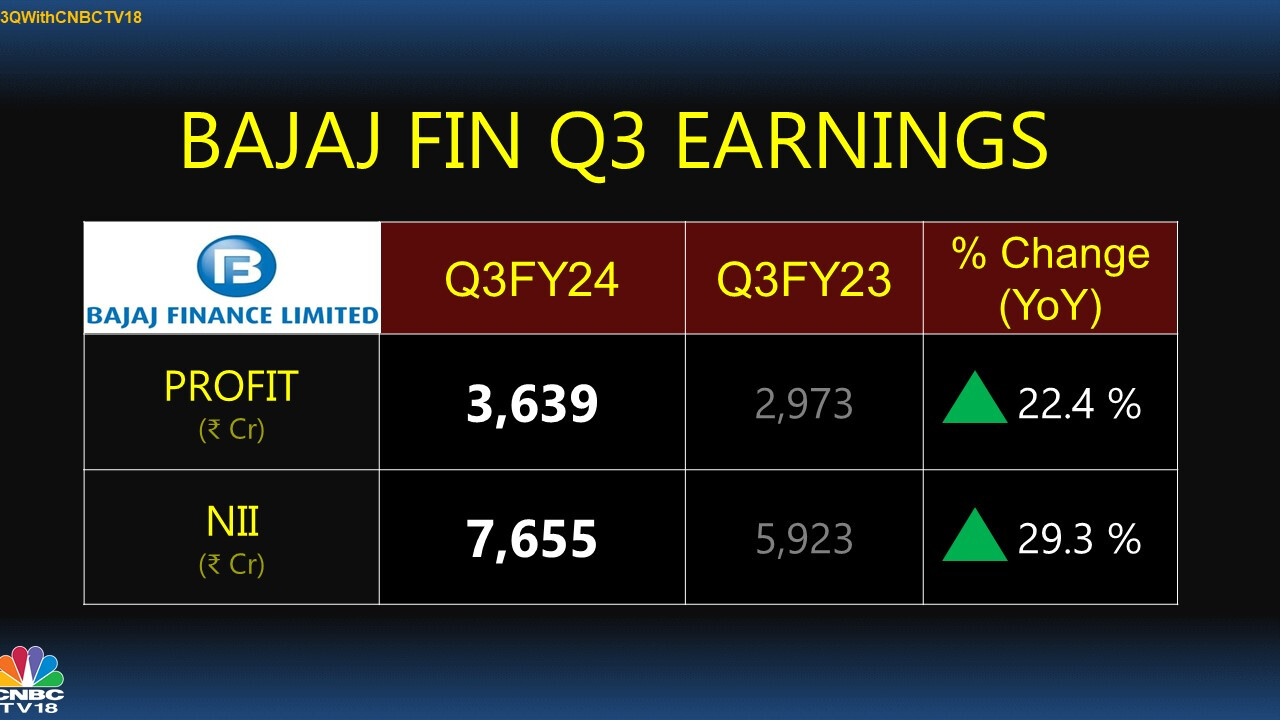

Q3FY2023-24 Quarterly Results

Press Release

https://cms-assets.bajajfinserv.in/is/content/bajajfinance/q-3-press-releasepdf?scl=1&fmt=pdf

Conference Call

Transcript

1 Like

Sometimes unnecessary greed to make money left right and centre can lead to a downfall of an otherwise humongous multi billion dollar business. Such idiocy is prevailing and very well acceptable of otherwise very dignifying business managers who claim “corporate governance” in every public appearance they make.

But is it the fault of bajfinance? This seems like fault of hospital rather than bjafinance

Yeah it’s not about fault. It’s that, as dignifying corporate citizens, we must distance ourselves from acts, that when written about by an able but not so friendly journalist in a regular newspaper, we as managers/owners of that business do not feel ashamed reading it out to our family members.

I am sure that in financial sector you have to do things which don’t look ethical.

Giving a personal loan at 24 perc+ interest is not ethical. Creating mounting pressure on an individual to repay a loan is not ethical, calling millions of people and convincing them to take a loan is not ethical. But doing all of this makes money.

Also, is giving loans at higher interest rate to needy people ethical? But will we ever invest in a company giving loans to needy people at 10 percent? We won’t be able to, such a company will not survive.

A finance company takes all opportunities available to it for growth, optimising its own risk reward ratio.

As a share holder you will like a company growing at 25 perc rather than an ethical company growing at 10 percent, sometimes going into losses so that it can give some leeway to people who might be facing difficulties repaying loans.

7 Likes

We should learn to draw our lines somewhere. Yet we will always justify our holdings. That’s just innate human psychology.

Keeping ethical considerations aside, this may turn out to be a very big addressable market for NBFCs in future as hospital cost is rising.

Also even comsidering ethical stand, just imagine, selling your house or ancestral land or begging from relatives and friends and taking their favour is better or taking loan from NBFCs and then repaying them monthly is better???

11 Likes

Any specific reasons for why Bajaj Finance is falling so much? Any new circulars or guidelines or usual profit booking? I tried to search but couldn’t find anything on usual sources.

Request the more informed members of the group to kindly throw some light on.

Thanks,

5 Likes

Provisional results for Q4 FY24.

The AUM growth despite RBI restrictions are pretty impressive.

It would be interesting to see how much of the incremental 19k Crore Aum growth this quarter (83k crore this year) came from existing customers vs new customers.

bfl-Pre-result-earning-disclosure-for-q4-fy24pdf.pdf (188.3 KB)

1 Like

RBI lifts restrictions on Bajaj Finance’s digital loan products https://www.financialexpress.com/business/banking-finance-rbi-lifts-restrictions-on-bajaj-finances-digital-loan-products-3475570/

5 Likes

How is IPO of a subsidiary good for Bajaj finance?

Demerger will give the existing shareholder the shares of demerged entity. IPO will only make the parent a holding company and hence will result in holding company discount.

Disc: Invested in Bajaj finance, so opinions are biased.

I am unable to understand the logic behind IPO of Bajaj Housing Finance. All the existing shareholders are clear-cut losers in my view. Earlier they were getting the value of a big balance sheet. Now the balance sheet has shrunk and book value will dip as subsidiary becomes a separate entity. Also share price has not comedown. Why not? Reasons are not clear to me. Also for shareholders quota in the IPO, what is the cut off date?

Senior forum members can elaborate for benefit of others.

1 Like

This is RBIs mandate to list Bajaj housing.

From shareholders point of view, there is nothing great to celebrate in this IPO (I feel).

Book value is not going to dip. On contrary, there will be marginal upside to book value in doing this.

Sorry. I agree that book value may increase due to IPO proceeds. But business will decrease and so also profits, at least in the short term.

Why would business and profit gonna decrease. Both will increase

1 Like

If you are referring to the fact that even though BHFL profit raises, share of BFL will reduce because of stake sale, that should be fine considering they will sell at higher price to book and they will good cash from this transaction.

Moreover this Housing arm is not such a great profitable business compared to parent business. CRAR is already at 20-ish range, but generating a RoE of only 15-ish range. Offcourse book grown at great pace, but all this major growth is funded by capital from BFL. But after IPO, as and when new funding requirement araises, it will happen in open market and at a higher PB, this will provide lot of inorganic returns through valuation rerating.

But since bajaj finance itself is a good business and listing a subsidiary does not make much of a diffrence. This is more or less like a neutral event(My thought).

2 Likes