I think Mr Chuggani has presented compelling reason for Bajaj Finance undertaking their digital transformation. While we can all agree that Bajaj is the leader in offline store consumer financing, the Company seems to be building something big comprising of an eco-system of apps including

- E-Store

- Wallet (Bajaj Pay) and related payments infrastructure.

- Insurance marketplace (For Bajaj Finance- this would be distribution)

- Investments marketplace (For Bajaj Finance- this would be distribution)

- Bajaj Financial Securities - Mobile Trading App

Relevant Q4 Concall transcript:

“The Bajaj Pay for consumers which is our payment infrastructure with BBPS services gone live”

"The three marketplace we have which is our e-store, insurance and investment market place are in advance stages of development at this point in time. The first phase of estore has gone live in February, we are now 25,000 SKUs on it for consumer electronics business, 40,000 retailers have been onboarded and the final capabilities of e-store will go live between July and August 2021. The insurance and investments marketplace will go live between July and August as well. The onboarding app of Bajaj Financial Security has gone live and the trading app will go live on 31st of May. 12 adjunct partner app are live and overall, 28 apps will go live as the premium financial services goes live. Quickly on customer experience I had outlined that we are clear that if we have to be a moment of truth company we will need significant transformation in customer engagement and experience, we think engagement comes from service so there it is just to give you texture 33% of the overall app ecosystem is dedicated to service just at a frame level so clearly we think it will lead to what is really the core reason why customers will engage more and will do more business"

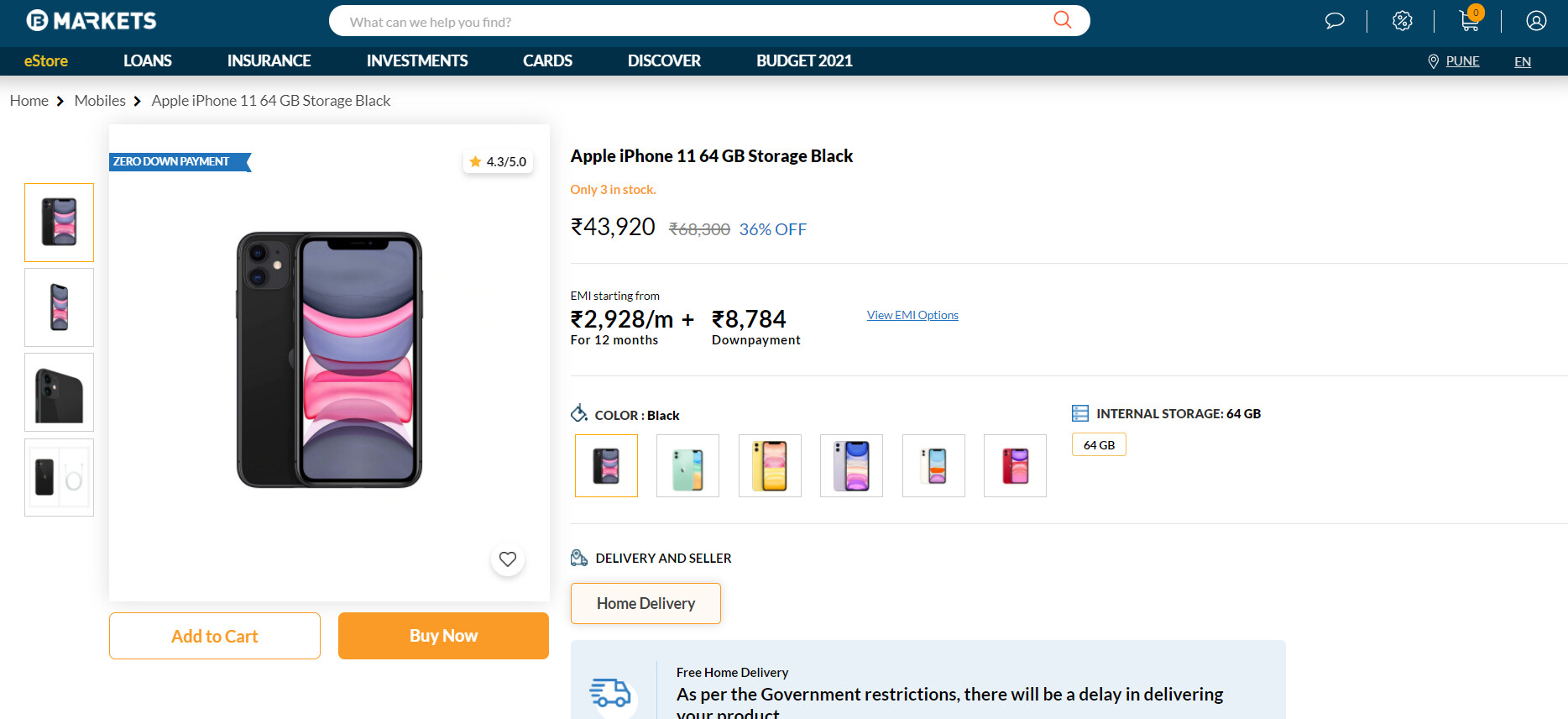

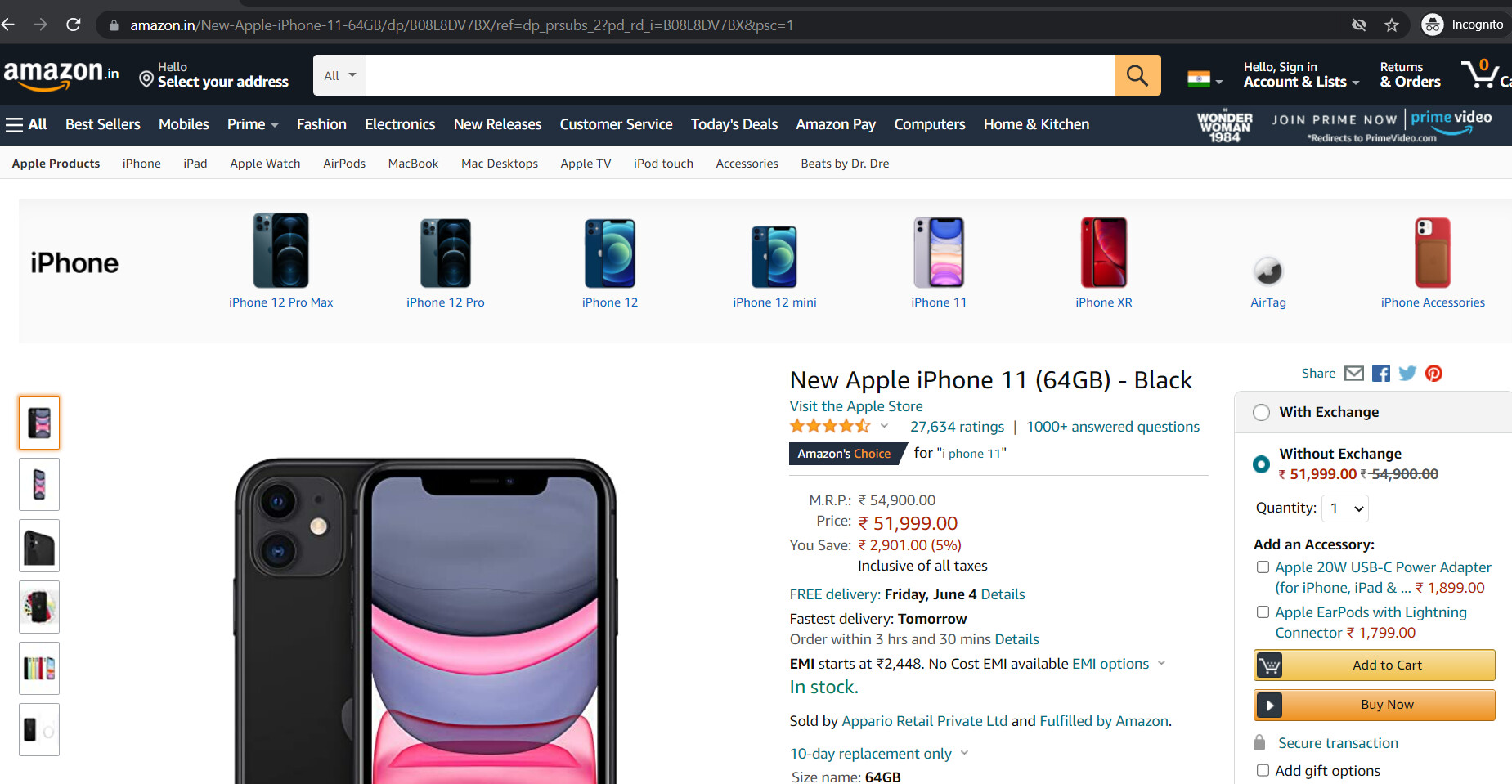

- Estore - Bajaj Finserve Markets has already gone live and can be viewed at - https://www.bajajfinservmarkets.in/

I was surprised to see that sellers were offering certain products at rates cheaper than Amazon. For eg:

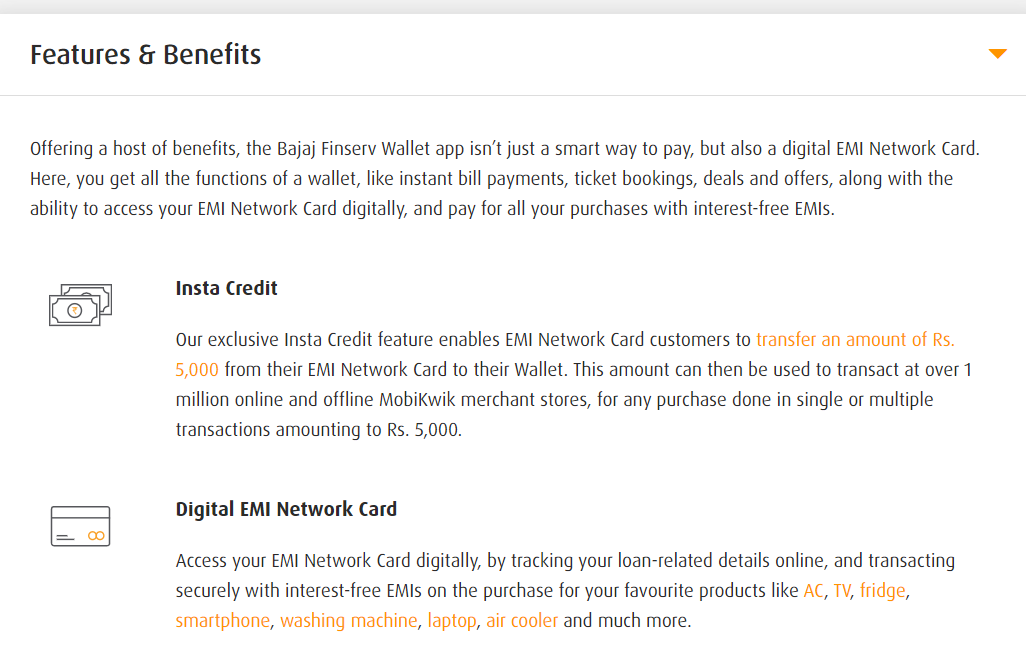

- Wallet has been there for some time now but one added benefit available to Bajaj versus competitors like Google pay, Amazon pay etc is that since it is has an NBFC license, it can allow customers to draw into wallet from EMI card

-

and 4) Cross selling online through Bajaj Finserv markets app - One can already see Products of most AMCs (I haven’t checked insurance since one has to enter personal details)

-

Trading App - I dont have an account with Bajaj but would love to hear feedback from anyone who has started using it.

Another very relevant concall transcript of Mr Rajeev Jain with an intriguing example in Q4 call was-

"How you fundamentally see phase I app as integral phase I app, merchant I app are integral to what we call the omni channel infrastructure is integral to the overall design it is important for and that is why we are saying an omni channel framework where customer will be able to transition in a frictionless manner between offline and online and vice versa so I think that is something for you to remember now let us just take an example for a moment so that it becomes clear point to sale you would have an e-store you are on e-store at home you look for a retailer in your vicinity you identified product you do not buy it you go to let us say add to cart and you left it we realize that appliance is a high involvement

category we will fundamentally flow that lead to the store that you have chosen and the person either to the retailer based on our arrangement or to the point of fair person that we have who based on a point when do they speak to you and assess to you and help you probably at the store and do the transaction that is the one example of omni channel the other example of omni channel we may pre-approve you. You have downloaded the premium financial services you do add to cart but are not able to go ahead because you need some assistance and we need something from you that leads based on a allocation methodology will flow to a particular person in the field who would assess you and help

you go through the transaction. We are very clear that on the other hand it may be an insurance product or an investment product that you maybe want to buy in three clicks it maybe a broking account that you will be able to if you are a KRA customer. As KRA customer you will be able to open in three clicks so it will defer product-by-product and nature of the product and the nature of the transaction so the ride when you look at it would be as it emerges between August and September as the experience there is a customer that is really where the imagination would become more clearer so we are all excited about launching this."

On customer acquisition through the new ecosystem:

"We are not building as a new customer acquisition at a design level as I said in two panels before we continue to originate customers at point of sale that does not mean that this will not originate new customers avail we see EMI card origination has now become a reasonably large standalone engine digital engine for us we are now originating anywhere between 60,000 to 40,000, 45,000 paid customers and 60,000 to 70,000 approved customers on a month-on-month basis, we think as this ecosystem will become large it is very much possible that number will significantly expand but leave that aside our focus is on originated the point of sale and acquire and cross sell is really been our strategy and that is really what this panel and platform is intended to serve. We have enough customers we are very clear that we will be a sometime in the near future we will be 100 million customers company given the distribution and the product portfolio that we bring to the table and the geographic presence that we bring to the table.

We will continue to originate customers, our origination frame is not changing, it (new eco system) may bring additional customers at no cost… We don’t need more customers, we need greater engagement and we need greater share of the wallet

In my opinion, with the roll out of the new ecosystem of apps, the aim seems to be to not just get higher share in existing business (B2B lending / EMI card based lending), but to get higher margin - lower risk business such as Trading, Distribution.

So far, Bajaj Finance have been one of the best in execution - be it in on the spot customer acquisition, popularising BNPL product for the mass affluent, cross sell of other lending based products and industry leading recovery metrics. If the new digital ecosystem platform implementation are similarly executed in line with the promise, the overall business and image of the company itself can be transformed from a lending business doing cross sell into an integrated consumer products company offering a host of products like online stores, wallets, broking etc.

Disc- Invested from lower levels and biased