https://www.carelyst.com/india-needs-two-three-new-banks-every-two-years-for-a-decade-sanjiv-bajaj/

Competitive pressure and action on the same (need to track )

Disc :: Invested

https://www.carelyst.com/india-needs-two-three-new-banks-every-two-years-for-a-decade-sanjiv-bajaj/

Competitive pressure and action on the same (need to track )

Disc :: Invested

I fail to see the significance of this move. Payment solutions as such is not a profitable business in India anymore.

The more intelligent things BFL limited has beeen doing till now may be restricted in a way after JUNE 2021.

Amid a number complaints from consumers against banks and digital payments platforms, the Reserve Bank of India on Friday announced to roll out an Integrated Ombudsman Scheme for banks, NBFCs and digital transactions in June 2021. The aim is to simplify the process of redress of grievances easier, Das said.

Following the global initiatives on consumer protection, the banking regulator took various initiatives to strengthen the grievance redress mechanism of regulated entities.

Basant Maheswari exits Bajaj Finance @ ₹5000

The famed investor (15:10) informed that it was to avoid the volatility in portfolio and because he has found better opportunities.

I believe that the current year performance of Bajaj Finance may be the real reason for the exit.

Div policy revised.

Rgds

RR

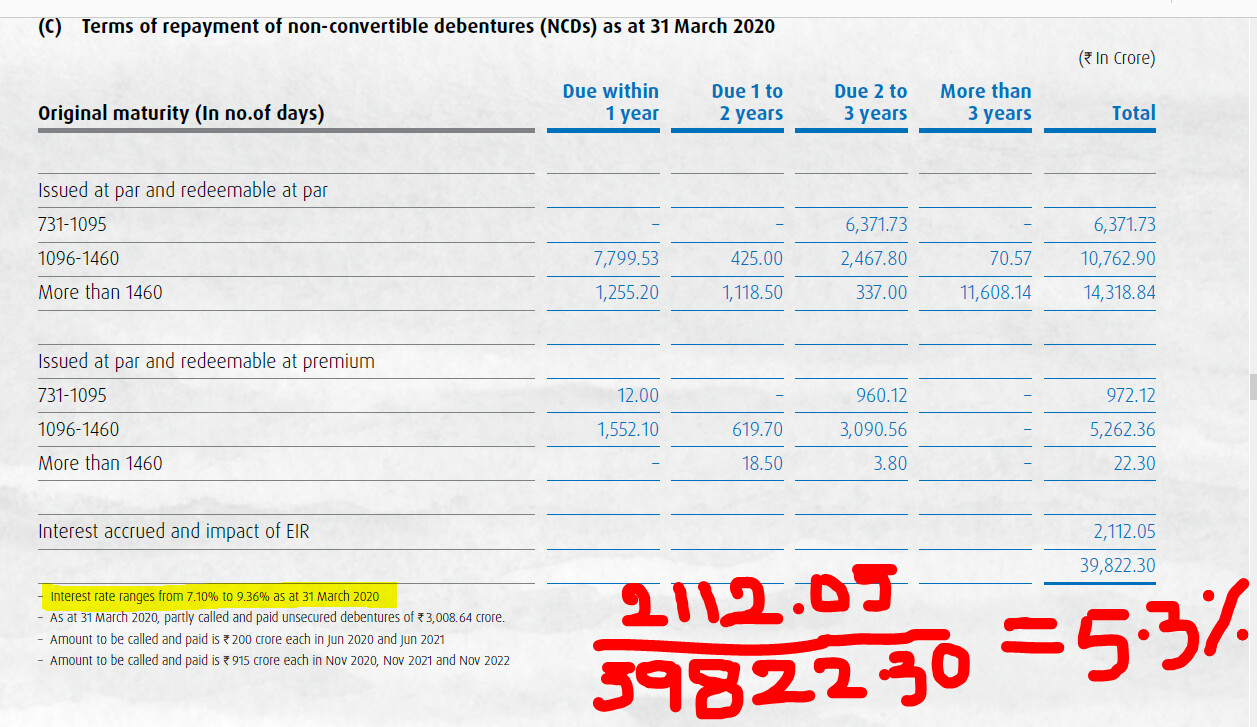

Dear Investors ,

can you help with below , how do they calculate EIR for these NCDs…

i felt EIR should be around 7 to 9.36 % , but its coming way less at 5.3%…

can you help me understand my mistake

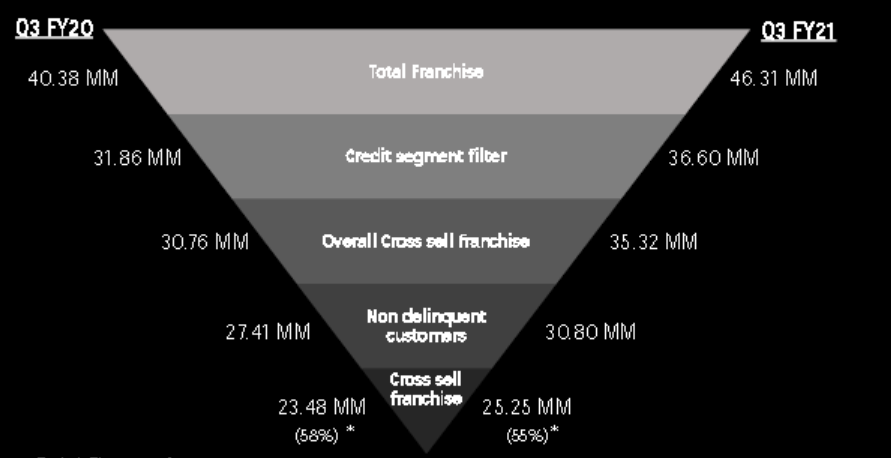

Point No 2 ::

could not understand difference between both the below charts … I felt both should be ideally be same

Regards,

Rama

There could be some overlaps

AUM growth back to pre-covid levels.

Rgds

RR

hi All

below is my detailed thesis on Bajaj Finance Ltd. (BFL)

While Bajaj Chetak was the largest selling 2 wheeler in India till 1990s, Bajaj Finance was its only captive lender, established in 1987. Foray into consumer finance (unsecured retail lending for appliances and durables) in 1999, also gave an early start to Bajaj Finance with its retail touchpoints. As of 2008, Bajaj Finance was chugging along at a loan book of 2,800 crores. All the wealth that the stock created comes from how the next 12 years panned out on the most important metrics –

| Particulars | 2008 | 2020 | Increase |

|---|---|---|---|

| Loan Book (in INR crores) | 2,800 | 141,300 | 50x |

| Net Worth (in INR crores) | 1,063 | 32,328 | 30x |

| Gross NPA | 9.0% | 1.6% | 0.2x |

| Net NPA | 6.4% | 0.7% | 0.1x |

| RoE | 2% | 20% |

Isn’t this spectacular? I took 2008 as a base, since the management changed in 2008, and the new management under Mr. Rajeev Jain is credited with making BFL the behemoth it is today. What follows might appear as 20/20 hindsight, but here I want to understand how did the above performance transpire?

| Particulars | 2011 | 2012 | 2013 | 2014 | 2015 | 2016 | 2017 | 2018 | 2019 | 2020 |

|---|---|---|---|---|---|---|---|---|---|---|

| Capital | 1,358 | 2,034 | 3,352 | 3,991 | 4,800 | 7,427 | 9,600 | 15,848 | 19,697 | 32,328 |

| Borrowings | 6,755 | 10,392 | 13,698 | 19,751 | 26,655 | 37,025 | 50,298 | 67,553 | 102,923 | 129,811 |

| Others | 344 | 435 | 666 | 1,976 | 2,867 | 4,727 | 7,001 | 630 | 944 | 1,403 |

| Total | 8,457 | 12,860 | 17,716 | 25,718 | 34,321 | 49,179 | 66,900 | 84,031 | 123,563 | 163,541 |

| Loans | 7,272 | 12,283 | 16,744 | 22,971 | 31,199 | 43,272 | 57,683 | 79,103 | 112,513 | 141,376 |

| Cash | 877 | 65 | 422 | 805 | 556 | 2,360 | 4,396 | 3,479 | 8,948 | 18,927 |

| Other | 308 | 511 | 551 | 1,942 | 2,566 | 3,546 | 4,821 | 1,449 | 2,103 | 3,239 |

| Total | 8,457 | 12,860 | 17,716 | 25,718 | 34,321 | 49,179 | 66,900 | 84,031 | 123,563 | 163,541 |

| Interest Income | 1225 | 1928 | 2814 | 3632 | 4892 | 6548 | 8692 | 11427 | 16349 | 22970 |

| Income from investments | 83 | 141 | 144 | 220 | 243 | 325 | 679 | 1032 | 388 | 688 |

| Processing fees & charges | 59 | 68 | 109 | 157 | 228 | 409 | 566 | 909 | 1751 | 2715 |

| Total Income | 1367 | 2137 | 3067 | 4009 | 5363 | 7282 | 9937 | 13368 | 18488 | 26373 |

| PAT / Total Income | 18% | 19% | 19% | 18% | 17% | 18% | 18% | 20% | 22% | 20% |

| Total Income/Total Assets | 16% | 17% | 17% | 16% | 16% | 15% | 15% | 16% | 15% | 16% |

| Total assets/Equity | 6.2 | 6.3 | 5.3 | 6.4 | 7.2 | 6.6 | 7.0 | 5.3 | 6.3 | 5.1 |

| RoNW | 18% | 20% | 18% | 18% | 19% | 17% | 19% | 17% | 20% | 16% |

| Efficiency Ratio | 34% | 31% | 28% | 29% | 27% | 27% | 26% | 28% | 23% | 21% |

| Interest / Earning assets | 17% | 16% | 17% | 16% | 16% | 15% | 14% | 14% | 13% | 14% |

| GNPA | 3.8% | 1.1% | 1.1% | 1.2% | 1.6% | 1.4% | 1.7% | 1.5% | 1.5% | 1.6% |

| NNPA | 0.8% | 0.1% | 0.2% | 0.3% | 0.5% | 0.3% | 0.4% | 0.4% | 0.6% | 0.7% |

Further this RoE is a blend of 18 different businesses, whose RoE profiles are as follows (variation in RoEs across business lines is on account of secured / unsecured loans, competitive intensity, duration etc.) –

| Loan Vertical | RoE % |

|---|---|

| 1. 2W & 3W finance | 22-28 |

| 2.Consumer durable finance | 24-26 |

| 3. Digital product finance | 24-26 |

| 4. Lifestyle product finance | 24-26 |

| 5. Personal loans cross sell | 16-33 |

| 6.Salaried personal loans | 14-16 |

| 7.Salaried Home Loans | 9.6-10.5 |

| 8. Business loans (BL) | 17-20 |

| 9. Professional loans | 14-17 |

| 10. Loan against property (LAP) | 11-12 |

| 11.Self employed Home Loans | 10-10.7 |

| 12. Loan against securities | 10.8-12 |

| 13. Vendor financing | 10-12.5 |

| 14. Financial institutions group | 10.5-12 |

| 15.Corporate finance | 10.5-12 |

| 16. Infrastructure lending | NA |

| 17. RM Business (LAP, HL, BL) | 10-12 |

| 18. Rural lending | 14-35 |

As can be observed from above, there is a large variation in RoEs across business lines. The same is on account of secured / unsecured loans, competitive intensity, duration etc.

BUSINESS

A successful lenders recipe has the following ingredients – conservative underwriting, diversification in its loan book, low cost operations and adequate compensation for the risk taken. BFL started the flywheel through its distribution as follows –

It further helped BFL that RBI in 2013 rendered banks uncompetitive through stringent regulation on ‘0’ EMI products. This business is fairly customised with BFL financing 25,000 SKUs across 26 manufacturers with monthly changes. Almost 20-22% of white goods sales in India are pushed by Bajaj Finance, with 70%+ MS in consumer lending. Below is growth in distribution over the years –

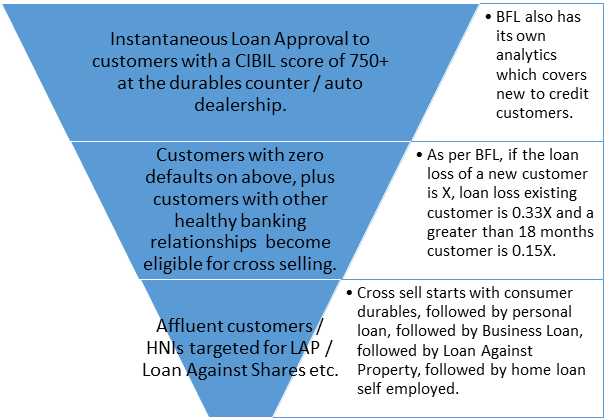

BFL is aggressive in cross selling its loans to the internal pool of customers through its direct channel. Below is the filter applied by BFL -

As of today, almost all individual loans (home, personal, lifestyle) are sourced directly from the inhouse pool of customers, due to which the company saves on acquisition costs, processing costs and distribution costs, along with having a lower risk of default as highlighted above. BFL also derives income from selling of insurance products, credit reports, credit cards, wealth management etc.

BFL’s focus on affluent customers is wide ranging and across loan categories. Eg. It started consumer finance only on Apple products, and even now finances only phones worth INR 10,000 or more. The Loan Against shares and LAP are only for super affluent customers. The salaried home loans to are only for those whose salary incomes are higher than 15L pa. In rural lending too, it only targets affluent households and has no MFI exposure. Below is the illustrated franchise –

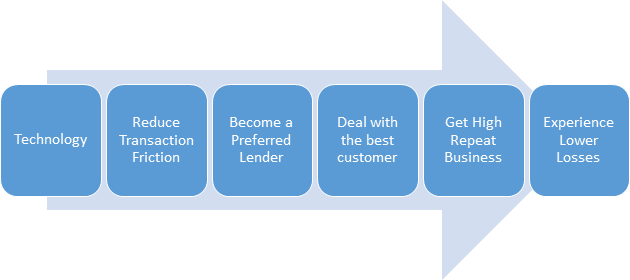

For the uninitiated, technology in lending could mean the instant loan apps thronging the market. However, those are simply poor business models waiting to blow up. For BFL, the genesis of technology is –

In company’s own words – “on an average the weight of the file used to be 2 to 3 kgs we found that clearly there are only 14 to 15 variables which are relevant so those are the variables which we used and we converted a decision support system. That decision support system is built on cloud so employee now or a distribution partner has to only take out from the financials and the balance sheet of a client those 14-15 variables based on that he gets an instant approval and a loan ticket as well. What happens is our approval rate in this business used to be 55% because he used to create a file then log it in it would go through verification and then 55% would get approved, now 95% gets approved because he does not login for whatever is reject to him he does not even login that file. So 50% you get the answer, right? Automatically 50% less files will come but the approval on balance of the files would be 95 to 100%. ”

Since the earlier post was too long, thought will continue with risks and thoughts on valuation here -

RISKS

Apart from Gross NPAs, which market participants have a key eye on, its very difficult to understand the troubles brewing inside lending businesses. What we can simply do here is understand how the company navigated during the downturns historically –

| Year | Event | Industry Impact | GNPA reported | Comments / Actions |

|---|---|---|---|---|

| 2013 | Taper Tantrum | Credit Freeze | n/a | BFL started to maintain a liquidity reserve @4% of borrowings. No impact on financials. |

| 2016 | Demonetization. | higher credit losses in 2w and LAP. | increased from 1.36% to 1.68% | total hit of INR 120 crores on a 58,000 crore loan book. Recovered fully in 90 days. |

| 2018 | IL&FS | Liquidity freeze in domestic debt markets | 275 crores w/off - 9 bps NPA | no problems faced in refinancing its borrowings. |

| 2020 | Covid crisis | high credit cost due to a 4 month lockdown along with moratorium | 2.9% GNPA with Auto book 11.5%. | BFL built a liquidity buffer of 22% till Oct 2020. Business resumed normalcy Dec 2020 onwards. Total provisions expected to be 6,000 crores, 4.5% of o/s loan book. |

source: management commentary over the years

As can be observed from above, BFL has escaped largely unscathed in the above downturns, and this gives us a conviction that the risk management practices of BFL are strong.

BFL further perseveres in maintaining safety with an Asset Liability mismatch leading to an outflow only after 1 year (thus eliminating the need to rely on short term sources of finance) nor undergo a credit crunch. BFL further has a liquidity advantage due to a churn in its consumer durables loans which have a tenure of 3 months, due to which a natural liquidity of 5,500 crores – 7,000 crores is generated on a monthly basis.

On Flexi Loans – Post suspension of moratorium on repayment of EMIs in Sep 2020, BFL gave an option of converting fixed EMI loans to flexi loans, whereby payment of principal could be deferred as long as the interest on it was paid. Essentially, these loans work like a credit line. While the market participants viewed this as a restructuring of loans, the company maintained that flexi loans were almost 25% of the loan even before covid hit, and thus new loans given out under flexi are not new or significant. in fact, Personal loans to doctors are all flexi, 90% of of salaried PL is offered only in flexi. 100% of LAS portfolio is on flexi, 60% of LAP portfolio is on flexi, 65% of SME which is 11,000 odd Crores portfolio is on flexi. Thus as per me, the flexi conversion does not seem to be a reckless behaviour from BFL.

Recovery Practices – With millions of loans sitting on its balance sheet, collections composes a major cost head for the company. of the 19,000 or so of its employees, almost 4,800 work in collections, where their role is simply to manage collection agencies, since BFL has outsourced all its collection operations and works with close to 16,000 agencies in 2,000 towns in India. A lot of these agencies work exclusively with BFL. In Jan 2021, RBI fined INR 2.5 crores to BFL on account of the strong arm and intimidation used by its agents in recoveries. While it is debatable on what % of blame lies with BFL, the reputational loss, both tangible and intangible, is a small risk to company’s operations.

By regulation and prudence, lending companies cannot grow their loan books faster than the rate of earnings that they have retained, since its capital limits would be breached. Hence, both fast growing NBFCs and banks need regular access to the capital markets. Although never articulated well, analysts and investors have an obsessive compulsive fascination with growth in loan book, giving only a lip service to the return on Equity (RoEs) earned. While initially puzzling, I understand somewhat why this is true. The P/BV multiple at which a lending company dilutes its earnings has a significant impact on the incumbent shareholders since this multiple also determines their incremental RoE. Simply put, Incremental RoE = (P/BV multiple) x Business RoE. As an illustration –

| Dilution | Multiple | ||

|---|---|---|---|

| Particulars | 1x | 3x | 5x |

| Existing Shares | 100 | 100 | 100 |

| New shares | 10 | 10 | 10 |

| Capital Added | 10 | 30 | 50 |

| Business RoE | 20% | 20% | 20% |

| Net Profit | 2 | 6 | 10 |

| Incremental RoE / share | 20% | 60% | 100% |

Funnily, analysts in J&K Bank Ltd.’s concall kept asking about loan book growth even when the bank was making losses (the J&K govt smothered these guys diluting at 0.3x P/BV). BFL, however, has diluted its shares at incredible valuations, not only spinning the growth wheel faster, but also making the incumbent shareholders wealthier, such that they have gained from the growth in business, as well as benefiting from the appreciating currency (Bajaj Finance’s own shares) –

| Year | Price | PY BV | P/BV | Closing BV | % diluted |

|---|---|---|---|---|---|

| 2020 | 3900 | 341 | 11.4 | 539 | 4% |

| 2018 | 1690 | 177 | 9.5 | 276 | 5% |

| 2016 | 427.5 | 96 | 4.5 | 139 | 7% |

| 2013 | 110 | 42 | 2.6 | 67.5 | 17% |

Taking the 2012 book value of Bajaj Finance as opening value, this is how Mar 20’s BV has been built over the years –

| Particulars | INR | As a % of BV |

|---|---|---|

| 2012 BV | 22.0 | 4% |

| Issue of Shares | 268.3 | 50% |

| Profits | 294.6 | 55% |

| Dividend | -34.4 | -6% |

| Other | -32.4 | -6% |

| 2020 BV | 533.6 | 100% |

Almost half of all gains in book value till date, simply come from diluting its share capital, which I found incredibly interesting. I am still thinking about the repercussions on its valuation. This analysis is only 50% complete, since I have been unable to identify inherent risks in the business, nor have studied the competition. So I’ll take up Sundaram Finance Ltd. next, a lender with ratios as good as Bajaj Finance’, but has not diluted even once post its IPO. Honestly, figuring out Bajaj Finance Ltd. made me realise my own blind spots in being unable to identify or believe in the ability of some businesses to thrive so phenomenally. I doubt I would ever be able to pull the trigger here. This one defies gravity.

It would be incredible to know your view on this too!

Umang

This is a very good analysis! Kudos to you. I have some queries i will list them below maybe you can help me understanding them:

The main benefit or moat of BFL was the physical presence of the BFL person in a consumer durable (etc) store. Now that it moat is getting slowly disrupted as i) store sales have reduced due to the pandemic and ii) there is stiff competition in online lending. So, I don’t think BFL will be able to keep this part of their moat intact for very long.

BFL is quite well capitalized and it had raised 8500 crs in Nov 2019. It has also raised another 750 crs in Oct 2020 through ECBs. Plus, it has a retail fixed deposit scheme from which it gets capital. In fact, it is perhaps one of the strongest in terms of their ability to raise capital so I don’t have too many concerns on that front.

Their home loan rates are comparable to all the major players in the market. Plus, with their strong tech background, I presume (and this is an assumption, which needs to be validated), they would be able to process the loans faster. Moreover, they are growing their book by getting a fair number of transfer cases from other banks. Home loan is a segment which has great untapped demand so the main point here is execution. Banking as such is a commodity business and creating differentiation is very difficult other than through the softer aspects of usability, technology etc.

We are now at a time, due to Covid, where retail loans are under stress and commercial loans are slightly better off. That is why you will find the banks with higher exposure to commercial borrowing is doing better and the ones with higher retail assets are struggling a bit. But this will not continue forever. Indian consumption growth is a multi-decade theme. It is on pause for now, not stopped.

in addition to the points mentioned by @basumallick, following are my points -

BFL simply walks away from a consumer durable financing category if banks are undercutting it on rates, highlighting that this business does not make sense for them at lower RoEs (they did this for Samsung phones initially).

As far as sustaining the advantage they have, i can point out to 2 things -

a. they have a large pool of customer franchise which is pre approved and get financing without friction (no KYC, form filling) at the storefront.

b. geog expansion since the competition significantly reduces for BFL after top 15 cities.

agree with the point that if ecom increases, their advantage will be weaker.

BFL raises funds only when its leverage aproaches 6x. Just because other lenders are raising money, why should they?

Home loans are the lowest RoE business for BFL for the reasons that you mentioned (sometime back SBI gave loans to BFL at the same rate as their home loans). The home loans are only given to their existing customers (low acq and processing cost), only given to customers with a high income / loan threshold, and are necessary since they help keep the customer in BFL cross sell franchise for a long time (high durations).

so just banking sector o/s is around 100 lakh crore. when you add NBFC o/s to the same, BFL, with a 1L crore loan book, is not even 1% of the market. i think those who are losing share currently are the PSBs.

Thanks a lot @bozo_investor and @basumallick your answers solved most of my queries just not able to understand this loan transfer concept! Do lenders transfer home loans to other lenders? And how does it work?

loan transfer (Balance Transfer) are nothing but transfer of customer loan from one bank to other bank/NBFC.

Normal this happens when customer gets better interest rate when moving to new bank/NBFC…

In general the terms used Balance Transfer

Balance Transfer Out :: amount of AUM which has been moved to other banks

Balance Transfer In :: amount of AUM which has been moved to the Bank/NBFC

In my view , High % of BT Out /BT IN should be taken with pinch of salt as both could have negative effects

High BT out indicates that the company is loosing to competition

High BT In could indicate that the company is putting pressure on the margins to gain customers

Note : Please check and correct me if I am wrong

during the covid crisis, the way hdfc, kotak and idfc banks are growing its seems that banks have taken market share of many other banks and nbfcs so is the growth engine of BFL which we seen in last decade is slowed down due to this black swan event?

Along with the above, Please find my views

@basumallick , @bozo_investor please correct if my thought process is wrong

Bajaj Finance Q4 Results: Net Profit Rises 42% (bloombergquint.com)

Bajaj Finance Q4 results

Disc : holding Bajaj Finserv

Any ideas, how this is different from the already one’s in the mkt.

Disc : Invested.