comparing a finance company to a paint company is not logical. It won’t give you any results. People on twitter generally complain about their issues. It is a customer care handle. Who will say thank you for the loan to a customer care? So in case you go to a complaint forum, you are going to find issues only.

Lets compare Bajaj’s interest rates with other credit cards / loan instruments. Loans on CC

Axis Bank basic cc

Finance Charges (Retail purchases and Cash) 3.4% per month (49.36% per annum)

HDFC Bank Snapdeal CC

Finance Charges (Retail purchases and Cash) 3.49% per month

ICICI Bank

Platinum CC 2.49% per month or 29.88% annualized.

So Bajaj Finance’s interest charges looks very fair to me.

**It is basically unsecured credit. So do not compare with interest rates on secured credit.

I agree with your observations. People who pick up the point of paint vs financial are altogether missing the essence of what you conveyed…which is the way of doing business. I would prefer a credit card company which charges 100 percent interest than a company which plays trick on zero percent. A known devil is better. I am surprised how those who like a company only see the good things in it and dislike the odd things pointed. It is indeed like love. I am also a victim of such thinking many times…

I am not comparing valuation or product of the company but management behavior!!

Even though three months moratorium given by RBI, non-other than Bajaj charging 24% interest on no-cost EMI!!

Customers get angry when they come to know new conditions of the loan, which were kept under carpet at the time of giving loan!

It’s not a new condition. Let us understand that any financial institution gets money through it’s circulation only and they would definitely discourage EMI moratorium else it may lead to temporary cash flow issues. People who have capacity to pay will also avail the scheme. Even home finance companies change heavy interest on any delay in EMI payments.

24% charge is one to simply discourage you to avail moratorium. Secondly company can not simply forego interest on this period as they are answerable to the shareholders whose money is invested in business.

Let us put ourselves in company’s shoes and see how many would forego rentals delays from tenants willingly.

Madhav Bhatkuly is Awesome guy to hear but check his fund performance.

Glenmark top holding (Only pharma stock not able to join rally and thats his best performing stock)

2.Shemaroo (down 75%)

3.Parag Milk fought ( bought at peak 250rs )

4.Manpasand ( On June 8, 2016 Saif Partners India IV Limited sold 11,30,000 shares of Manpasand Beverages at Rs 595.01.)

5.Cox & Kings (bought @173 down 99.99%)

I understand underperformance but even if someone tries cannot underperform than his fund.

Disclosure: Though I agree with what is being said in above interview and hold bajaj finserv

Bajaj finance caters to a lot of customers , not all of them can pay an emi just because you are going to charge an interest of 24% or whatsoever. RBI has given moratorium only on EMIs and interest will not be waived but will continue to accrue on the outstanding amount. So interest will accrue as the per the contracted interest rate. It is to be noted that there should not be any penal interest or overdue interest charged during this period. So it’s just an extension of term of the loan along with adjustment of drawing limits. So for a normal loan there are no confusions. Now let’s take a no cost EMI if Bajaj charges no interest @ all for 3 months ie, a quarter ,it will have significant effect on their NIMs as the interest will accrue for the loans they have taken with no yield on the lion share of their consumer loans. As such they charge 24% , which will be close to their yield on consumer loans which seems fair. However it is to be noted that this period cannot be considered as overdue period and many of the customers can take them to courts. I have seen moratoriums declared on msme loans , education loans etc numerous times. I haven’t seen moratoriums declared on consumer loans before( situation is totally different now). They will surely be having clause for charging a higher interest for overdue period but cant be considered as overdue period. But I don’t think anything of this sort would be foreseen. This can surely cause a lot of customer complaints and legal issues unless the contracted rate is 24%.

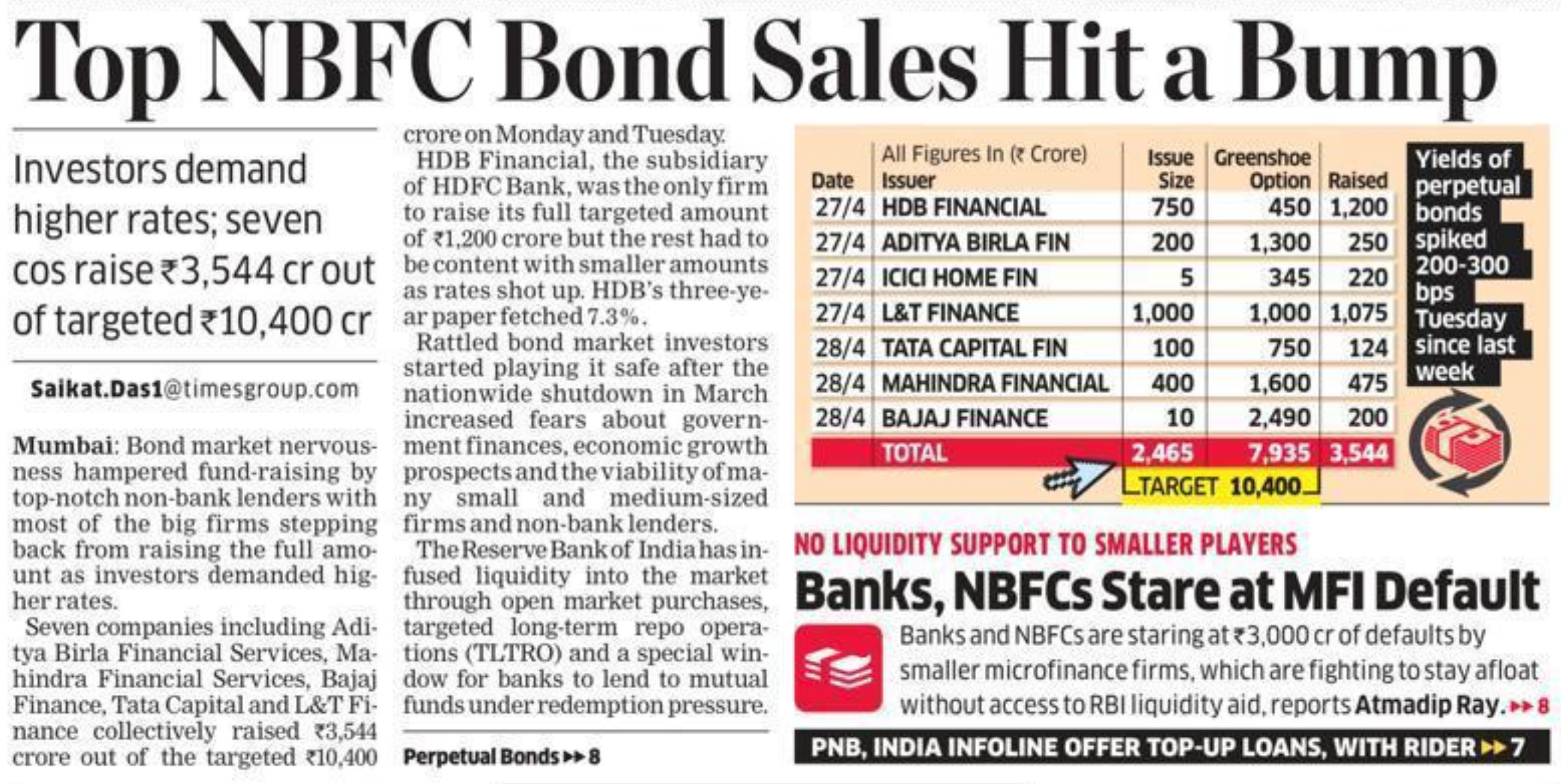

If you go by the below graphic,Bajaj Finance wanted to raise only Rs 10 Cr. with a green shoe of Rs 2490 Cr. and ended raising Rs 200 Cr.,one can see a similar pattern with Tata Capital and Mahindra Finance.

Total Issue size across issuers was Rs 2465 Crores and money raised was Rs 3544 Cr.,with Green shoe option(over-allotment) of up to Rs 7935 Cr. which only got partially filled.

HDB Financial however managed to get even their green shoe portion fully subscribed.

Yes, A Green Shoe option allows the underwriter of a public offer to sell additional shares/bonds to the public if the demand is high.

With information easily available now days its really important to analyse it rather than goby writer’s opinion. Deep dive analysis, Physiological behaviour & other soft valuation skills are the only edge available to us.

There is an error here as I also read an article which said BF wanted to raise 200 cr with a green shoe option for 2500 cr but could only raise around 200 cr.i would try to search the article and post it here.pl see the link below:

That article is by the same author(Saikat Das),the infographic is missing in the online edition,the total issue including green shoe was 2500 Crores(10 + 2490) and they raised Rs 200 Crores.

The discussion here seems to be divided between two groups; one, who believe BF going down the drain like DHFL and Yes Bank and two, who believe after a washout of two quarters it is going to find its lost glory. The truth lies somewhere in between.

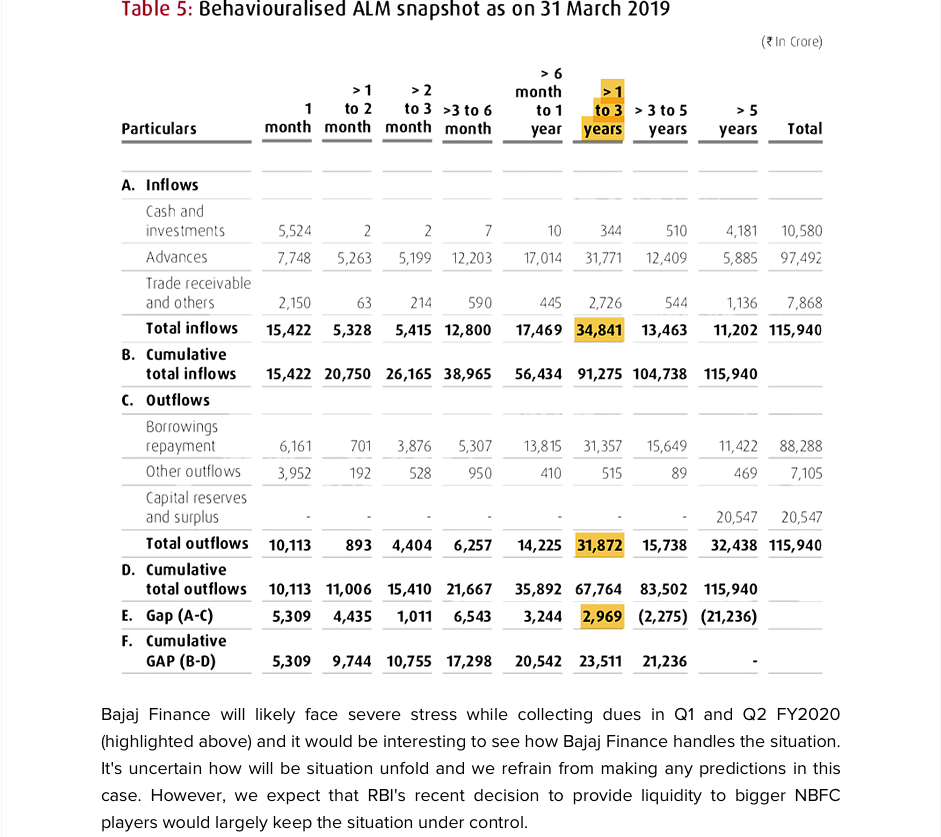

In spite of its aggressive and questionable lending practice, I believe BF has enough firepower and management bandwidth available to live to fight another day. ALM is not enough to take BF down.

But once a longtime trend line is broken, it takes a lot to course correct. Institutions who have distributed recently are not going to rush to buy again because it has become attractive pricewise. Someone wish to take a long term position needs to ask himself/herself a question - suppose the price doubles in two quarters, will he/she book profit or stay invested? For a long term upward trend, we need investors who are not only comfortable buying at today’s price, they should be equally comfortable to take positions after there is a significant price movement because the dream is still intact. Is it?

Issue size of Rs. 10 cr with greenshoe option of 24.9x shows they were unsure of the response and ready to take anything between the range, whatever comes their way. Typically, greenshoe option is a % of issue size; say 10-20%.

The strategy adopted seems smart given reputation risk in case they would have failed to raise with a higher issue size. Even Mahindra, Birla, ICICI and Tata went for that option. Only L&T and HDB seemed confident. This is my reading of the episode. Comments welcome.

I still feel that the figure of 10 crores seems incorrect as two different sources put different figures.Let us assume that the figure is 10 cr is correct. Does it give a negative signal that a company of such repute and size is seeking only 10 cr and if course it’s to meet ALM ? Moreover I have never heard a ratio of 250 between the green shoe option and original issue.

Tried to search on NSE website and internet to verify ,but could not get any further info on the same.

I view it slightly differently. The 10 cr figure is completely misleading. Let us look differently. Had they said that they need say 2000 cr and if they are able to garner only say 200 cr, it will have a huge negative sentimental effect on its stock price and its future borrowing plans. They purposefully put a lower number and tried getting all that they could get.

Thanks for the excellent analysis. The only question troubling me is…if the price had not crashed due to Covid 19 crisis, would you still hold your valuation view point. Often what we think, market thinks otherwise. There are no correct or incorrect answers here. I am not disagreeing to anything what you have mentioned in your analysis. Ignore if my question does not make sense

thanks

Excellent analysis @Anirudh1…Thanks for sharing. I want to add my view on your point on network effect moat. What if Reliance+Facebook+WhatsApp launch consumer financing (they revealed possible plan during Q4 result meet). They will have biggest network. We know how reliance kill all its competitors!! Jio killed many Mobil data providers!!. I see this is the risk… however Bajaj Finance might not be out of business but definitely it will feel though competition for growth and maintaining margin!!