Unlikely. Reliance, despite it’s super power status, never has got into Financing business. It is a messy business and not sure if they would get into it now. What may happen is Reliance partnering with Piramal, where in Piramal provides financing.

Hi Peabody, thanks for your comments. I have been tracking the business since early 2018 when it was completely out of my buying range. Im a big believer of risk management through buying at fair prices. Before Covid-19, the fair price according to me was Rs. 2300 and i must admit i was losing patience day by day as i saw this stock rise close to Rs. 5000

No, Covid 19 doesn’t change anything except a discount has now been applied to older fair value in order to reflect probability of losses in coming 1-2 years.

Thank you hnk_so. Its indeed very much possible that Bajaj Finance may face competition in terms of growth, market share and deteriorating margins if Reliance comes up. This might lead to Bajaj’s patner stores forcing them to reduce their cuts in every sale. It would be interesting to see if RIL would be able to manage its risks just like BFL.

However, i have not researched about this particular risk in depth and do not want to give out any incorrect views ![]()

1 Like

Reliance has never managed it’s BtC well. Be it reliance jeo or reliance retail.The customers seem unhappy with issues not resolved to their satisfaction.

1 Like

I believe they (RIL + WhatsApp) will partner with Piramal Enterprises in Consumer Financing.

Piramal has already announced their Consumer financing business and they also highlighted in their Investor presentation that they wish partner with a Telecom company.

Its not a hard guess which telecom player it will be. Also Piramals and Ambanis are relatives, so it makes more sense to join hands.

Piramal has already roped in Jairam Shridharan from Axis bank(ex CFO) to head the Consumer financing business.

The telecom company(Jio) will be generating the leads from a huge pool of prospective customers and if we combine the data they collect from customers along with Facebook,privacy and consumer rights be damned they would not only have built complete consumer profiles but also have the ability to track changes in real time.

The credit risk for this will be borne by PEL,so this is a win win for RIL.

With lending businesses,just having money does not guarantee success as we have seen time and again.

The ability to have a stable liability profile juxtaposed with proper underwriting are critical for success.

4 Likes

NBFC is not everybody’s cup of tea. Strong Risk management and lending takes years of practice to be implemented at ground level.

Some of the best investment banks like JP Morgan which had its NBFC arm in India surrendered their NBFC license. Its just not the customer base or network effect which will make one NBFC successful, Its the recovery and understanding the landscape is what makes them successful.

Even if RIL + FB which will have strong customer base can lend to people but when it comes to recovery their mettle will be tested. Lot of NBFC’s have come and gone, This space is not for everyone.So there will not be any imminent threat to BF by RIL+FB combo.

4 Likes

I agree your points. however, sometime such euphoric belief lead to speculative high price. Bajaj Finance reached @ 5000 when everyone believed that Bajaj Fin is the only company has special DNA!!

However, even good company stock price one day adjust to its intrinsic value!!

If you look at thread on Piramal Enterprises Ltd in 2018, people were comparing Ajay Piramal with Warren Buffet and PEL with Backshire hathaway!! But now story reached to normal level!!

hence, we have to evaluate company with open mind and accept that any NBFC get affected by new competition and risk in the lending market!!

Borrower always looks at interest he/she has to pay (the most important), accessibility and service offered (secondary objective) while lender always looks at repayment capacity of borrower - all NBFCs are working on this simple equation - The company which has command on this will have good future!

2 Likes

That was news to me. But even then, does it make sense for RIL to take all the risks for a customer. They already are giving mobiles away. Similarly with Jio Fibre router boxes.

Reliance is a smart business. They should prefer for someone else to take the credit risk.

It also doesn’t fit well with their goal of becoming debt free. Being a Financial Services business means picking up a lot of debt.

Let’s see how it pans out.

1 Like

I cannot agree more with @hnk_so. Most of the customers availing “No Cost EMIs” for electronic appliances are lower-middle-class people. They live on a monthly salary and apply for such schemes as they cannot afford appliances at once. It will be a very bad experience for such customers.

At the same time, I don’t rely on social media to see companies customer relationship because of below reasons:

- Human Nature - People never share a good experience on social media (if they do, it’s rare). On the other hand, if you feel something not up to the mark, you quickly share it on all social media.

- Paid reviews - Nowadays, the business started to give incentives for the positive reviews. eg. Hotel offering a free drink for 5 stares. Mobile shops offering free screen guard for a positive review.

Now let me take some time to explain why it seems a trick to me.

Any loan, which has a pre-defined interest rate, cannot be tweaked. eg. My home loan with HDFC, it has an interest rate of 9.0% according to MCLR (Marginal Cost of funds based Lending Rate) which cannot be tweaked for an extended period against the moratorium. Which means I will be paying extended EMIs with the same interest rate.

Now in the case of BFL No Cost EMIs, there is no pre-defined interest rate mentioned in the contract. They have interest-rate mentioned for late payment. If a person misses on the timely payment of EMI, BFL would charge interest of 24-36% p.a. BFL is charging 24% interest per anum (in my case. it might be different for other customers) for extended EMIs due to moratorium. It means BFL is treating “defaulters” and “people opting for a moratorium” the same way. Which I feel is not correct. Of course, they are going to loos some customers because of this.

The management is thinking short term (liquidity problem) now v/s long term (customer relationship) ![]()

1 Like

my reading is all NBFCs and banks are charging interest if client opts for moratorium.

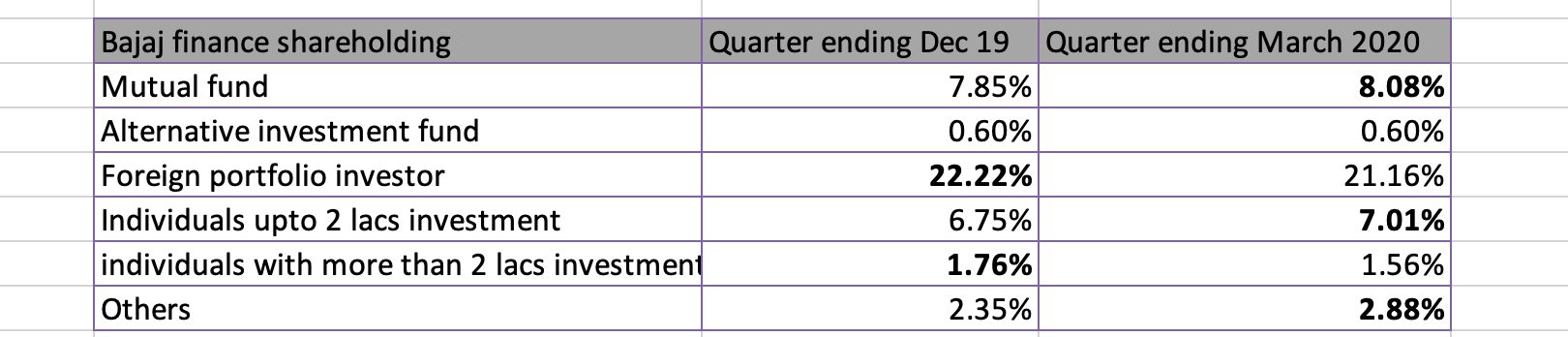

There has been a serious debate on social media about the “VIGOROUS” retail participation in Q4 FY 2020 vs Q3. I tried to capture the shareholding pattern of these 2 quarters and found below ![]()

Mutual funds: there is an increase of 0.23%

FPI: Decrease of 1.06%

Retail investors less than 2 lacs investment: increment of 0.26%

Retail investors more than 2 lacs investment: decrement of .2%

I think numbers speak beyond words or sensationalism so as to say

13 Likes

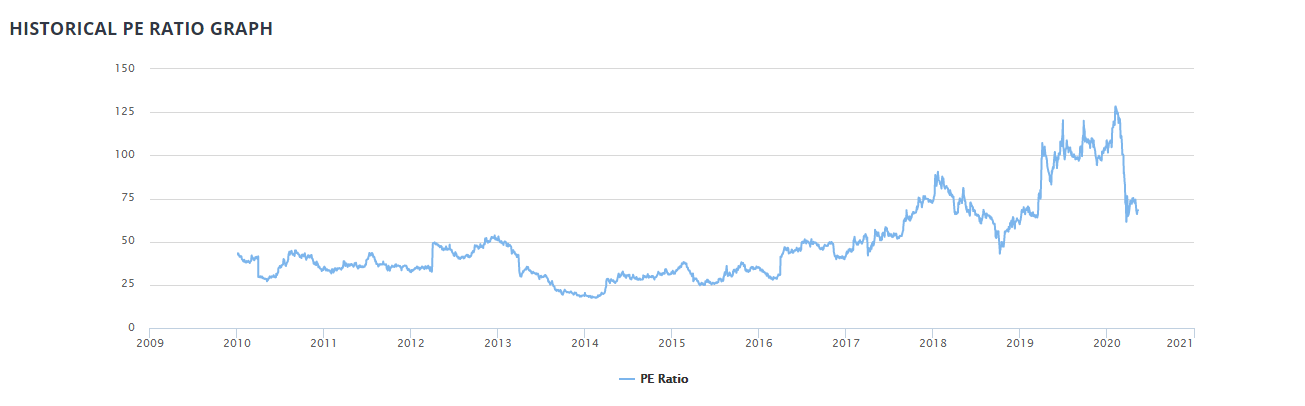

Yes, the probability of losses arising out of the potentially disruptive market environment in the near future due to the Covid-19 crisis must have played over the investor’s sentiment thereby leading to a sharp fall in the stock price. The major thwart should have come from the fears relating to the repayment of a major portion of the loan portfolio given the unique disruptive environment hurting the incomes of the retail(middle & lower middle income ) customers which forms a major chunk of customer pie for Bajaj Finance Limited. The absence of clarity on the subsiding of the crises has only made things worse as far as improvement in consumption sentiment is concerned. This has though has created sharp correction in the valuation of Bajaj Finance Limited with its PE ratio being at lowest level in the last five years.

Over the years Bajaj Financed gained customer base exponentially by focusing on consumer durables financing which was often ignored by the banking sector due to its low ticket size. They made the business model feasible and affordable by latching on to operational effectiveness by adapting to technology platforms & integrating the ecosystem with the manufacturers. Also unlike many other NBFCs, Bajaj Finance adhered to financing models wherein they borrowed the long term and lent short term with prime focus on short tenor loans such as consumer durable financing, personal loans & two-wheeler loans. This made them relatively less exposed to asset-liability mismatches.

These two factors have helped Bajaj Finance to scale stupendous growth over the years and helped it to emerge as one of the largest retail asset financing NBFCs in India. But with the Covid-19 crisis taking its course more intensely & with strict lockdown norms in place, consumption has slowed down considerably and discretionary buying is also out of sight & is in serious jeopardy. So the strong growth that the company was clocking over the past few years is seemingly not coming back at least for a quarter or a two. However sharp correction in valuation, strong management & robust track record of growth remains key noteworthy attributes from a long term perspective.

12 Likes

bajaj finance 14 may 2020.pdf.pdf (465.0 KB)

5 Likes

Based on the April Covid update call - Bajaj Finance had penciled in a worst case lockdown of 49 days & a rise in delinquencies by 80-90% which works out to excess credit costs of approx 2,000 cr.

Given that the lockdown is longer than the originally anticipated 49 days, has anyone come across any research report modelling the growth in delinquencies? The curve is definitely more exponential than linear based on optimistic, base case & worst case projections. I don’t think a 30% YoY de-growth in PAT for FY 21 can be ruled out. Hopefully we will get more clarity on how to model the risks going forward on the call.

2 Likes

Results:

https://www.bseindia.com/xml-data/corpfiling/AttachLive/1723c0e2-6471-43d8-91a2-9bb44e15c693.pdf

Investor Presentation:

https://www.bseindia.com/xml-data/corpfiling/AttachLive/b9158543-a086-4f6e-86c9-c0210e7cdd47.pdf

Concall at 6.30 pm today.

Live Webcast of the concall can be accessed at this Link:Bajaj Finance Q4FY20 Result Call

To register for the Concall:Diamond Pass Registration

5 Likes