The information about insider buying that you have shared is not exactly proprietary. It has been in public domain since last couple of weeks, when the consensus opinion was that India would open up after April 14. But in the meantime, the Covid cases have really spiked and total removal of lockdown after April 14 seems far fetched. Buying of shares of Rs 80 crores is not enough to change the direction of the trend of a company of market cap of Rs. 1.4 lakh crores.

In the last couple of years, BF has really gone aggressive about lending financing anything under the sun. There are even EMI schemes for Byju’s online classes. The quality and earning capability of BF customers is less than HDFC Bank and others. For example, couple of my employees earning 8k-12k have BF Cards of more than 1 lakh each. Moreover, there is a massive migration undergoing from cities to villages right now. I really wonder if they would be that cautious about their CIBIL score when things turn difficult.

The most important headwind is not during the lockdown but what comes after. A prolonged distress situation would drastically change the consumerism behaviour like it happened in 1929 and 2008 in US. People who have ample capability and liquidity to take loans would also hesitate to spend by taking loan. I tried to discuss this couple of weeks back too but my post got flagged as spam.

Disc.: Holding from lower levels but not sure about the direction of the long term trend now.

I’ve seen lot of arguments over long vs short on BFL, and I would say that’s the beauty of financial markets. Its a zero sum game. The most imp thing is for one to have a strong opinion to enable his investment decision whatever it may be.

Personally I like to simplify stuff rather than get entangled in the complexity of various kinds, trying to become a future teller!.

Whatever ratios you look at P/B, P/E, P/FCF, Provision%, etc there are millions in the market looking at the same stuff. BFL is not trading at elevated valuations now, it has been there since long and the market knows about it. So the key question here is not IF they deserve higher multiples, question is WHY there deserve that?. I would say any company in any sector deserves (and gets) higher than industry avg multiples because of the growth premium. (one can argue there are other kinds of intangible premiums like management quality premium, ESG premium, etc). If I am a long term investor, I would think whether BFL will be able to show similar growth or not (which is I guess a 20-30% CAGR in earnings, loan book, etc). Now given where India is in its macro developmental path, and the way consumerism is growing, I would put my dollars in assuming that there is a lot of potential growth and penetration left for consumer finance and BFL is a industry leader (because of reasons we all know).

As I said its just a simplified view: Consumer financing has lot of growth potential, Bajajs are good management group, BFL has done many industry first things to become and remain a leader (cross-selling, AI, cards collaboration, etc) - net net I would put my some long-term dollars to work in this stock and just go along. Will there be short-term stress - yes, but I am prepared for that and will hold to hopefully see a higher ground later!

Disclosure: Entered the name during this correction. Technically looks weak so will get more at 2000-1650 levels (where i think this will bottom out)

Excerpts from the interview of Mr Anand Tandon in ET :

What about retail delinquencies? How much of a risk do you see there? Today we are in fact seeing Bajaj Finance take another bit of hit, down about 10% odd and we already heard their guidance. I know it is a market leader but they are being cautious and rightly so. How big a threat do you see there?

We have to wait and see. We have not seen the kind of retail delinquencies of any significant amount so far but going forward, I would not be very surprised if the numbers are fairly high and in strong double digits. When I say strong double digits, maybe 10-15% range at least because that is one sector which has been taking loans left right and centre. The domestic household in India has actually doubled its leverage over the last five years. Most companies who have been lending have been lending unsecured and therefore, you are assuming that life continues as normal.

Someone who is let us say earning on the basis of a small business he has or has erratic earnings will still have to pay off; all of which has changed for the worse now. So you will look at a fairly significant drawdown in terms of the retail portfolio which means that NBFCs are likely to be hit quite badly. More importantly, the microfinance companies to my mind are going to take it on the chin and of course, all the private sector banks that have gone up in effect over the last few years are the ones that are likely to get hit.

The flip side of this is that credit is going to become far more expensive or far more difficult to get for the retail sector, which means that the one leg that the market was working on in terms of consumer discretionary has to now take a back seat in terms of growth. So portfolios which are heavily focussed on consumer discretionary will probably lag in the near term.

Bajaj Finance, one of the largest financiers of consumer durables, said the ‘bounce’ rates for consumer loans were 2.5 times the normal. The lender has already warned delinquencies could climb 80-90% in the current lockdown.

One of the things in Bajaj Finance’s favor is the 8000 crore of QIP money recently raised.

This would help.it cover at least a major part of its losses over the next 2 years or so.

Given this capital buffer what would be a fair price for this stock? Any inputs from seniors appreciated.

Liquidity is not an issue with Bajaj Finance it is very well capitalized. Key question are:

How much would be equity damage, once it comes out of Covid19 & new book value

At what valuations Price to Book it should trade in future which is dependent on:

Can it rub this event off, retain investor trust and grow like it has in done the past?

Both points are evolving with time and news flow

I have listened a few portfolio manager calls and everyone who owns it gives it a benefit of doubt - Great company and would come out stronger

Opponents to above theory question the gravity of impact of Covid 19 on its book and say even current valuations are high

Sincere advise - If you are owning it - don’t over allocate as ‘All In’ kinds of bet.

When financial environment is not good and company keeping higher liquidity is good but it impact bottom line of the company as (1) it has additional cost to company (2) Reducing RoE (3) Reduces loan book growth…reduces income

However, excess liquidity raised from equity dilution is better than raised from borrowing money from market!

For Bank / NBFC … velocity of money is important… (Lend fast and more, collect efficiently and lend again)…if company borrow and not able to lend or not able to collect efficiently and lend again…it is negative for any Bank/NBFC.

Till date many NBFC and low grade Private bank were able to show top and bottom line growth by playing only half of the money velocity cycle i.e. borrowing fast and lending fast …but failed to recover money effeciently…this is landmine/explosive situation as it will destroy company by higher NPA and Higher provisions . !!!.

Sometimes investors fail to recognize quality of growth of balance sheet… companies playing half cycle only could show excellent top and bottom line growth by wholesale lending to poor guy who must pay higher interest rate. By lending poor guy at higher interest, company could show excellent growth in top and bottom line in first half of the cycle but go bankrupt in second half. We have examples…Yes bank, DHFL, PNB, PNB Hgs Fin…many are in pipeline!!! Investors who has extra ordinary skill / luck could make lot of money by entering at start of first half and exit at end of first half cycle!! But many are in loss as they buy when growth at peak (end of first half) and remain invested!! Only few has such skill like Basant M (who entered and exited PNB Housing Finance on right time!!)

“Note that BajFin has about 15K cr of liquidity, and has incoming cash flow of between 5 and 7K cr per month (my rough estimates) even if there is a moratorium for some customers. They will also be able to raise, at a low cost.”

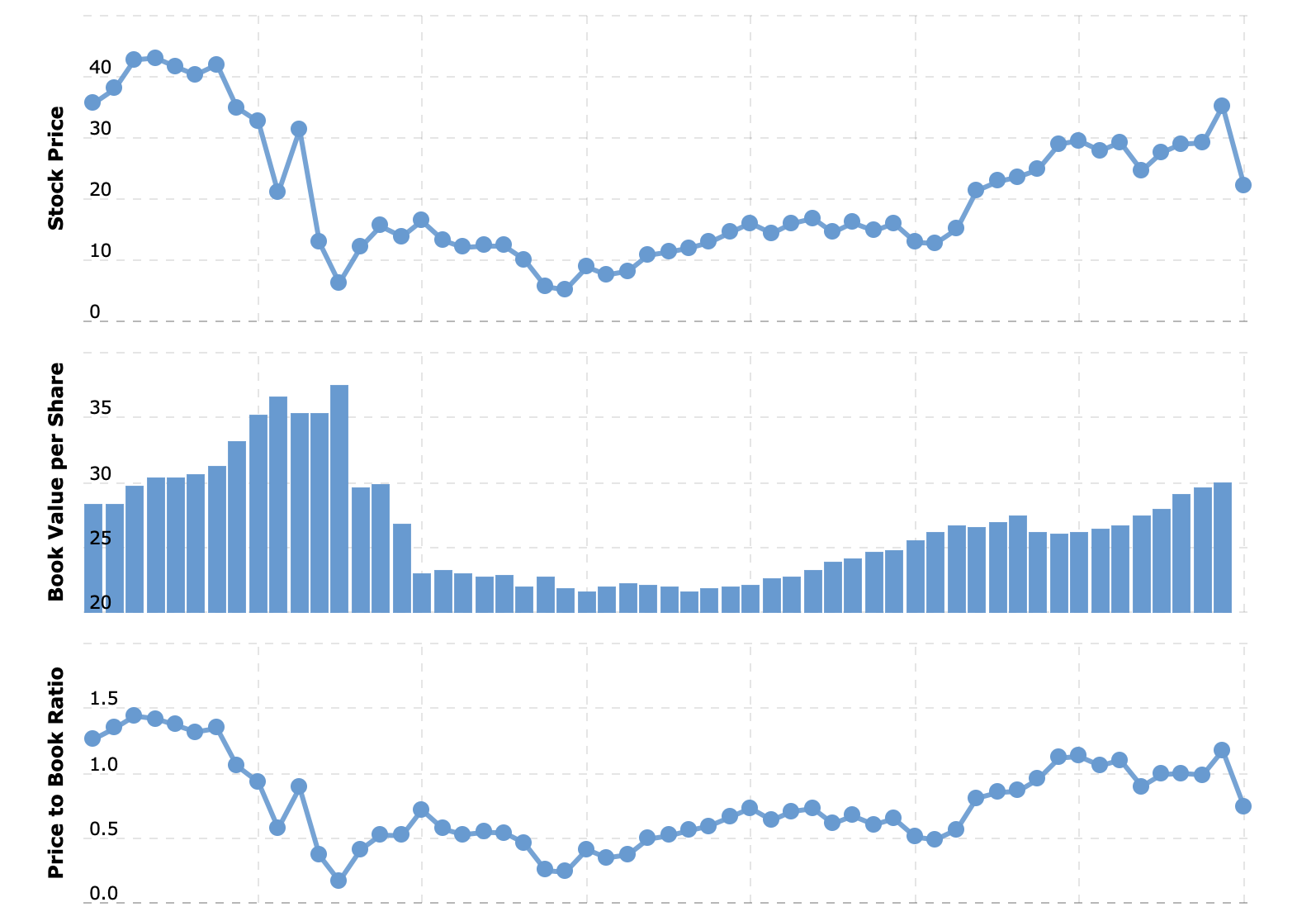

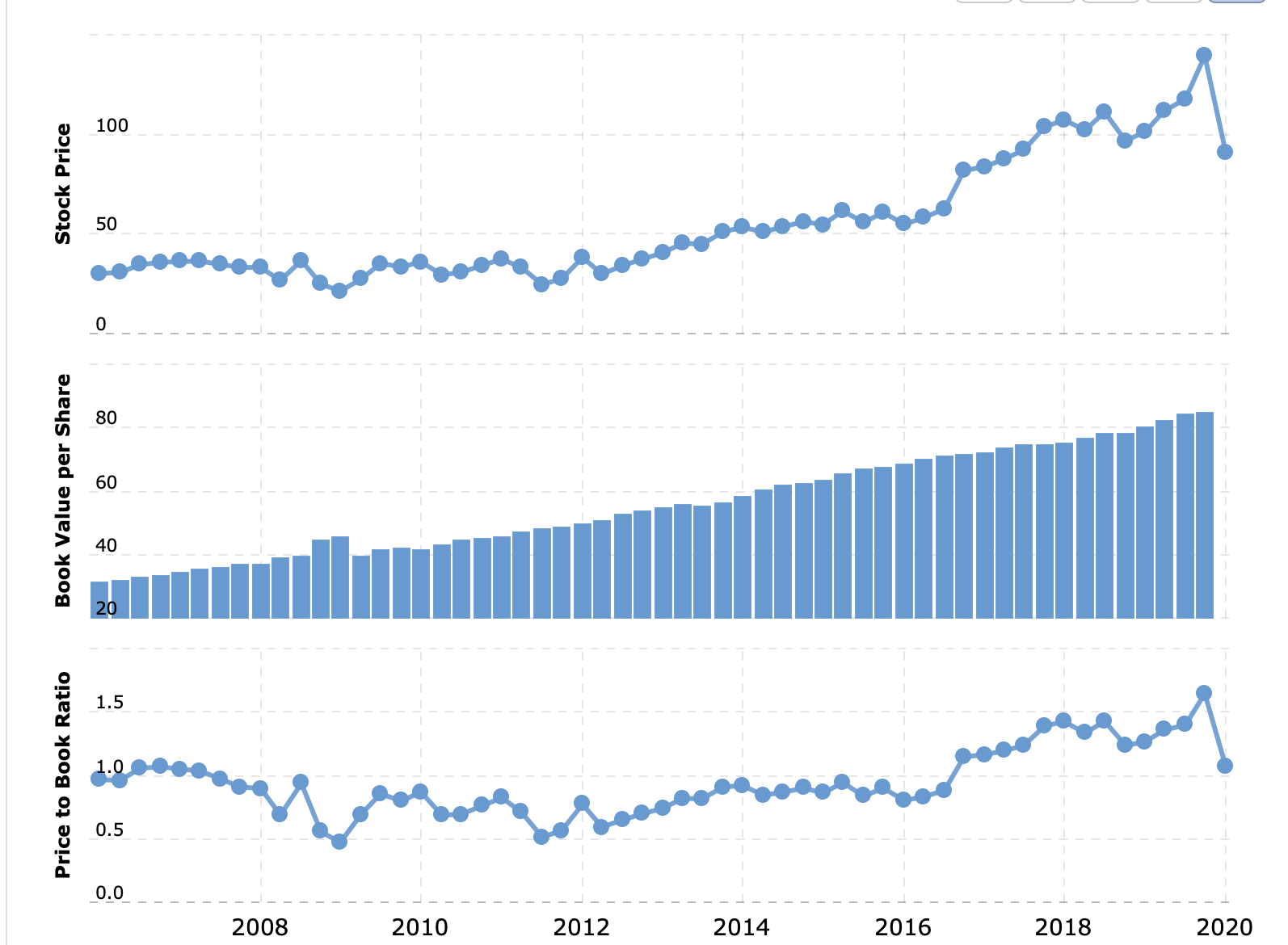

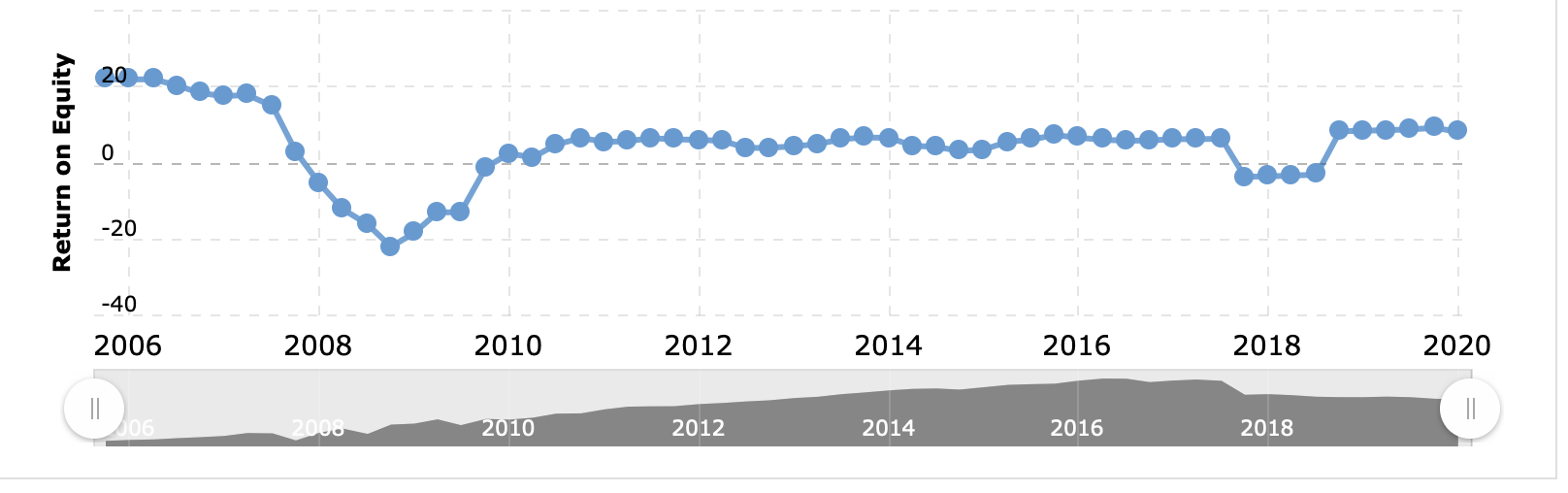

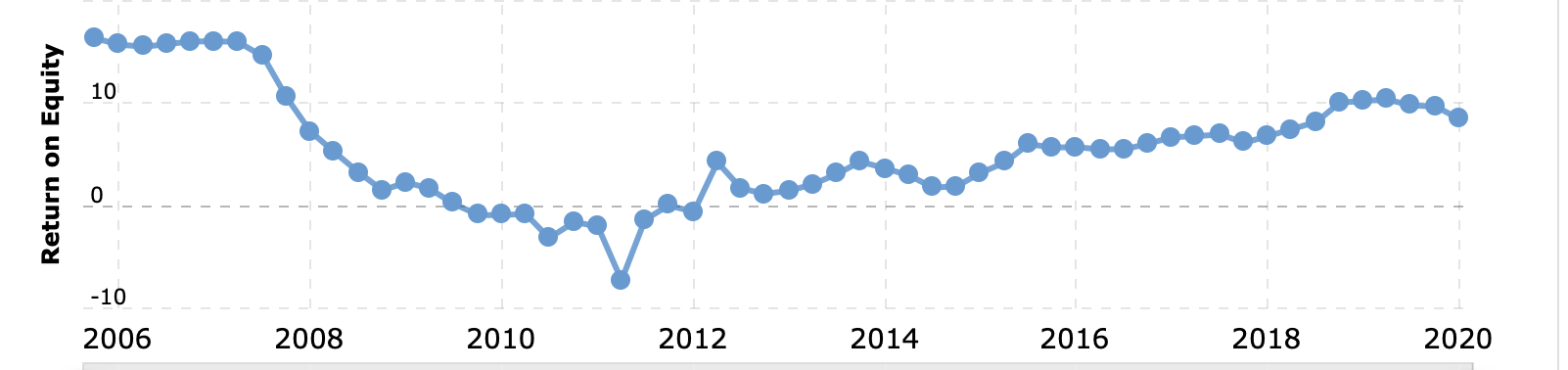

We can look at three large US consumer lenders as reference …

First what happened to subprime lender Citibank in 2000 - 2020 . Price fell from 550 to < 15 and today after 12 years it is around 45 odd . This is becos of multiple capital infusion required over period of time

India’s Discount for lack of Govt / Public support during financial crisis ( as USD has reserve currency and hence US Govt can support troubled banks better than Indian Govt support to its banks )

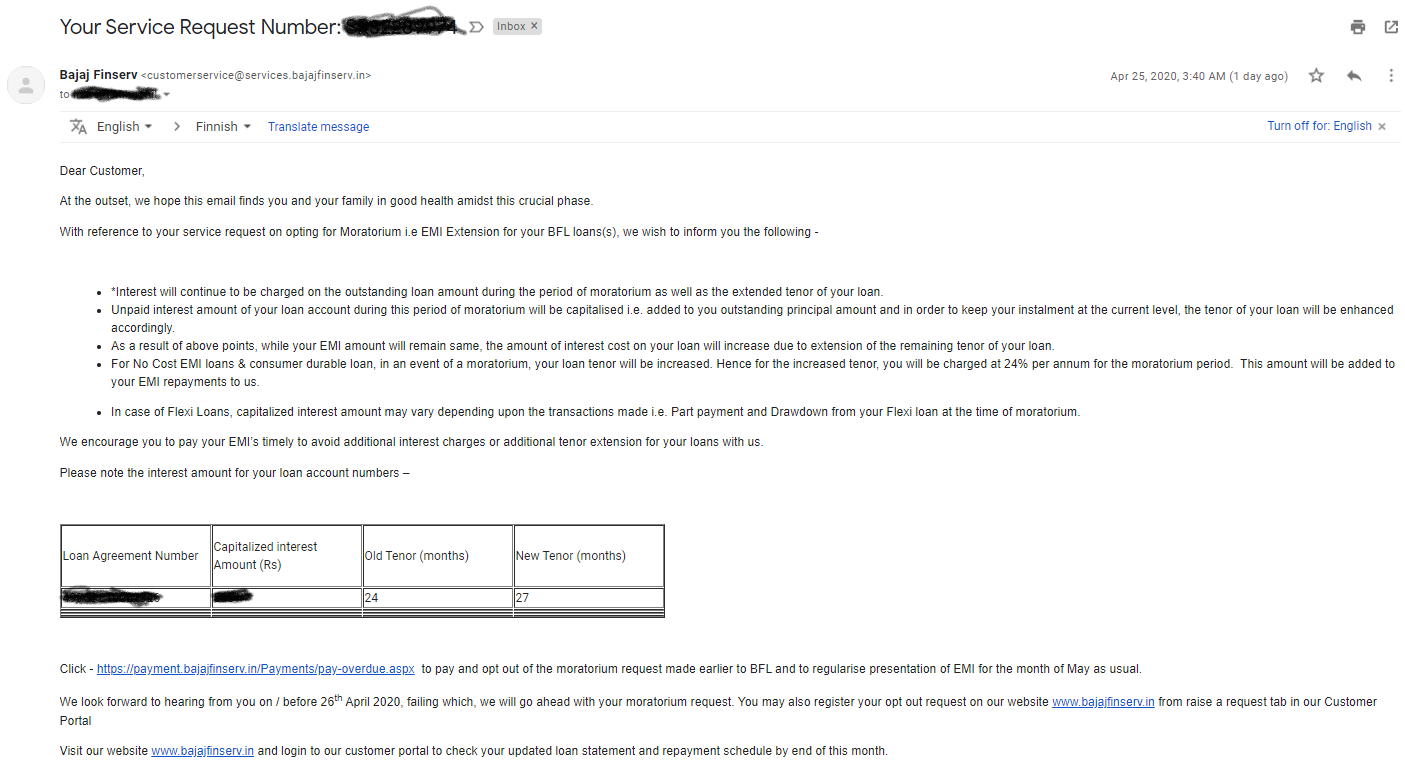

“For No Cost EMI loans & consumer durable loan, in an event of a moratorium, your loan tenor will be increased. Hence for the increased tenor, you will be charged at 24% per annum for the moratorium period. This amount will be added to your EMI repayments to us.”

It says they are going to charge 24% interest on all consumer durable loans including zero cost EMIs. And right below the loan details table, they have provided a link to opt-out from the moratorium. Looking at the interest rate they are charging, most of the people will decide to opt-out from the moratorium. Which will fix the liquidity issue as more repayments of the loan will come in. If someone decides not to pay the loan, then also they can get low-cost liquidity from the market and repay it when they receive payments. But additional interest income is going to impact their profitability positively.

I request other investors to share their viewpoint if I am missing something here.

Agree that P/B below 3 offer MOS but the problem is most in the market knows that and waiting to buy below that price. My view is that Until & unless their is Big broader market fall you wont get Baj Finance at that price. Another way to invest is via bajaj finserv as when you do SOP calculation holding % discount is at max level in past 3 years. As the saying is payup but dont overpay

Its a fact that risk averse individuals will buy it after trend reversal confirmation.

Whereas risk ignorant or risk loving individuals may start accumulating it even before reversal confirmation (according to their logic - be it price-action or according to momentum indicators etc).

However, in any case - one should not jump-in early just because of Fear Of Missing Out.

If there is increase in delinquencies what will be impact on Book value … How much it can reduce - In above example of Bank of America - it fell by more than 50% from near 40 to near 20s …

What will be PE and P/B de rating ?? which is pretty common in such instances even if it is temporary - but as both Book value drops and P/B gets derated fall in stock price is magnified

Normally when a favored sector starts declining it takes 24 to 60 months to reach bottom …

IT services in 2000 -2004 , Pharma from 2015 - 2020 , HUL from 2003 - 2010 etc …

So you will get lot of opportunity to catch Bajaj finance at attractive price -

Can you please calculate if it’s actually 24%? Or, are they showing some calculations to make you pay. If 24% is on incremental, interest on interest, and if that amount is small, that should be fine.

Such tricks are not good for a company as customer will loose faith/trust in company and never take loan from the company. Repeat customers are the asset for this company. Hence, for short time gain they shall not loose long time growth and relationship with customers.

Just type hashtag #bajajfinance or #Bajajfinserv in tweeter, you will be surprised by seeing so many customers have lost trust in the company due to such tricks!!

Good company which built long term customer relationship is the one who helped their customers in difficult time. Recently Asian paints and pidilite extended their cash support and credit line to their customers to come out from such difficult time. Such customers are become loyal to the company