The color of the money is same whether an adroit/sensible insurer deriving it out of sound underwriting process received as a premium or an financial institution deriving it out of well laid out scalable framework that reduces per unit of incremental cost and increases per unit of incremetal profitability.

Whether each of them uses it to acquire new business/ increase customer base/strengthen their balance sheet or adjust their Opex it is their jurisdiction.

No money is absolutely free, though it might seem so and we have seen how many insurers in the world even break even. There is nothing called as a free Money. The whole illusion around it has brought many ruins.

What will be scenario if all get combined-

(1) Management has little negative news on rising NPA / collection problem (next con call)

(2) Downgrade by Bernstein - negative view by FII

(3) Sovereign funds liquidity from Indian blue chip equities

(4) SEBI ban promoters for inside trades/ buying their own company shares

Human beings tend to extrapolate bad news to extinction and vice versa. There could some turbulence, nothing much.Bernstein report has no meaning now,as the valuation has compressed by 50%. Please remember, BAF is a market leader. I cannot imagine India will have no NBFC operating successfully, because the rest have been decimated and may have survival issues.

After 50% Corr, it’s still trading at 6 PBV, plenty of room for correction. Nifty is still somewhat away from it’s swinglow, whereas BaF is ready to break its in the next session.

For reasons rightly pointed out I think Bajaj Finance has at least 20% more down room.

I feel turbulent times always shakes out weaker players from every sector and helps better players become stronger. Current event seems like mother of all times. So it would have major impact on the economy which will eliminate many “fly by night” operators in financial sector also. I expect Bajaj Finance will be beneficiary and will emerge stronger. So its a long term buy for me. As far as how low it can go, that depends on how bad it can get before it starts getting better. So that would be individuals call.

Looks like too many participants - tried multiple times but couldn’t correct, here is some summary from media participants:

From what I could hear towards the end - The more the lockdown stays the harsher the impact. They have created 3 scenarios based on how long the lockdown stays.

Impact of lockdown is so severe that even doctors are not making any money ie no OPDs happening.

They generally don’t lend to aviation and hotels sector or employees… but no sector is untouched by this

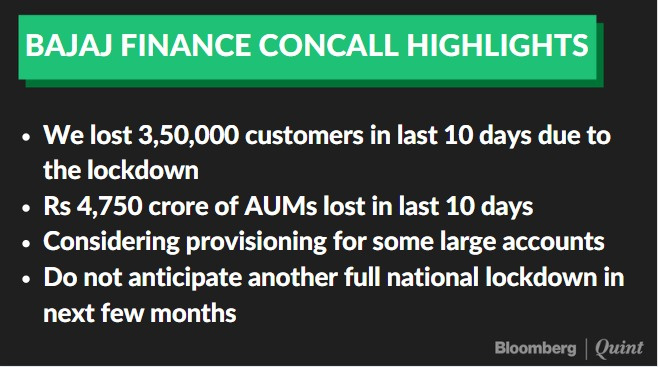

I was there on the call. Dont think RJ said they lost 350,000 customers. He was like we could have added that many customers and Rs 4750 cr AUM if the quarter lasted for 90 days instead of 80 days due to lockdown.

They said they will release call transcript tonight so better to wait for that.

What will happen in April 2020 …should we get bottom?

For retail investors - Will it be catching falling knife ? or Getting opportunity once in a life?

I think to save capital is the first priority - wait until dust get settled !! De-growth + negative news = PE De-rating +pendulum effect could be in play to get at below 1000!

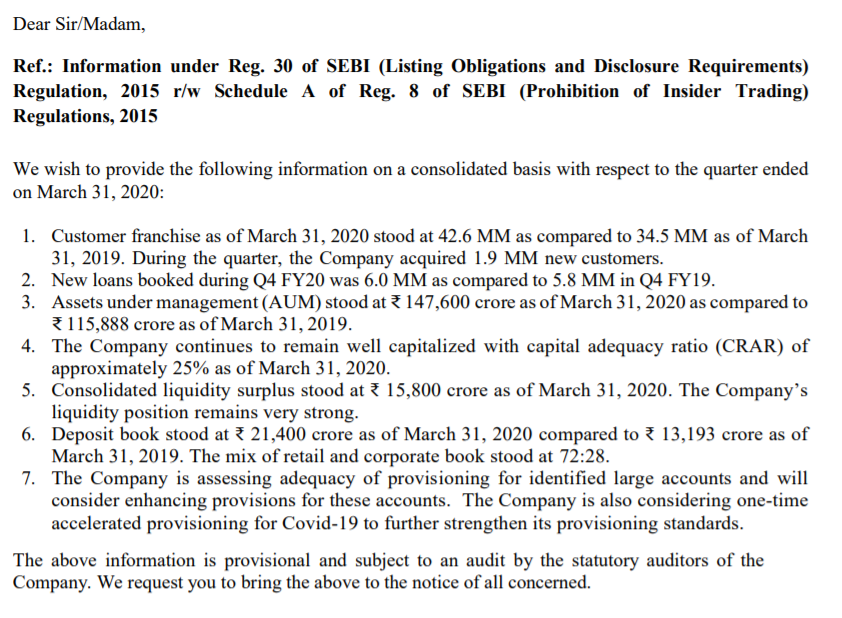

"1. Had it not been for lock down, the company could have added another 350,000 more customers taking the total to 2.25 million new customers addition during the quarter. " - rajeev jain

I think the common consensus is that Bajaj Finance is heading for a price collapse. But thanks to Anant bhai I looked at the insider trading data.

3 Promoter group companies have been buying equity shares from the market in the last couple of weeks. Do look at the price chart on each date of purchase as per table below.

These companies have directors from the promoter group family (bajaj). These companies have never purchased shares of Bajaj Finance since May 2015 also.

In this video, Guy Spier and Mohnish talk about (Bajaj Finance) why they would never invest in a fast growing consumer finance company, which they met with that morning:

In a world of such 6 sigma, unemployment spike, the thanksgiving turkey needs to choose between survival and growth. And the valuations would not like either choices.