-

Waluj (Aurangabad) plant is the largest plant of Bajaj Auto. There, the number of covid-19 positive cases inch closer to 300 and about 6-8 people have succumbed to the infection thus far.

-

Bajaj Auto has decided to continue operations at its Waluj plant in Aurangabad despite some fresh Covid-19 cases being detected at the unit.

.

“…Covid cases … have been dealt with as per standard protocols and in consultation with the authorities. Given the nature of the pandemic, we believe that this may be a regular occurrence despite best efforts by the company and its staff,” Rakesh Sharma, executive director, Bajaj Auto. -

Bajaj Auto has increased the attendance to 50%, in two shifts, six days a week from 1 July.

-

Workers continue to allege that there were no social distancing measures implemented in the plant. However, the company, in an official statement last week, had said that it had taken all necessary steps of testing the workers, contact tracing and complete sanitizing of the plant.

Rajiv Bajaj in his interview with CNBC has said that 250 out of 8100 workers in the Aurangabad plant are infected with COVID.

-

People who were infected weren’t coming to work. They weren’t affected at our facility

-

Contrary to media reports, employee unions are happy to come back to work

-

He also mentioned that 60% people in Aurangabad aren’t wearing masks (no idea who can have such insights) and there’s ZERO social distancing. Staying inside the factory is the safest in Aurangabad

-

However, the killer dialogue was “Just for media optics, co will not close the plant”

-

His view on the lockdown being dracorion in nature still stands

-

There will be a V-shaped recovery. KTM is seeing roaring sales

One Observation:

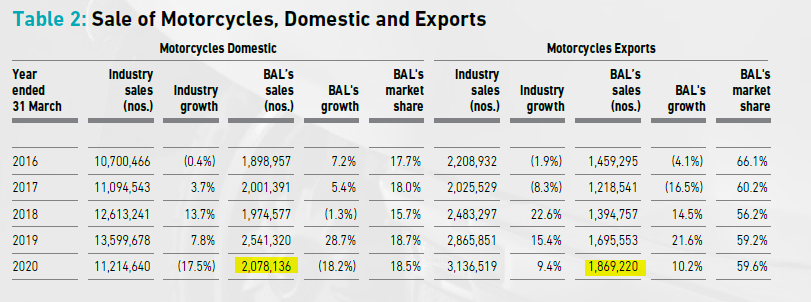

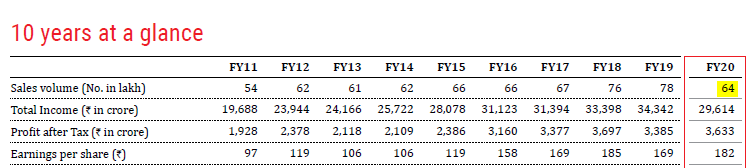

Bajaj sold ~ 40 lakhs 2 wheelers in FY 19-20, where as Hero sold ~ 64 Lakhs bikes in the same period. Reevenue for both companies is close to rs 30000 in FY 19-20

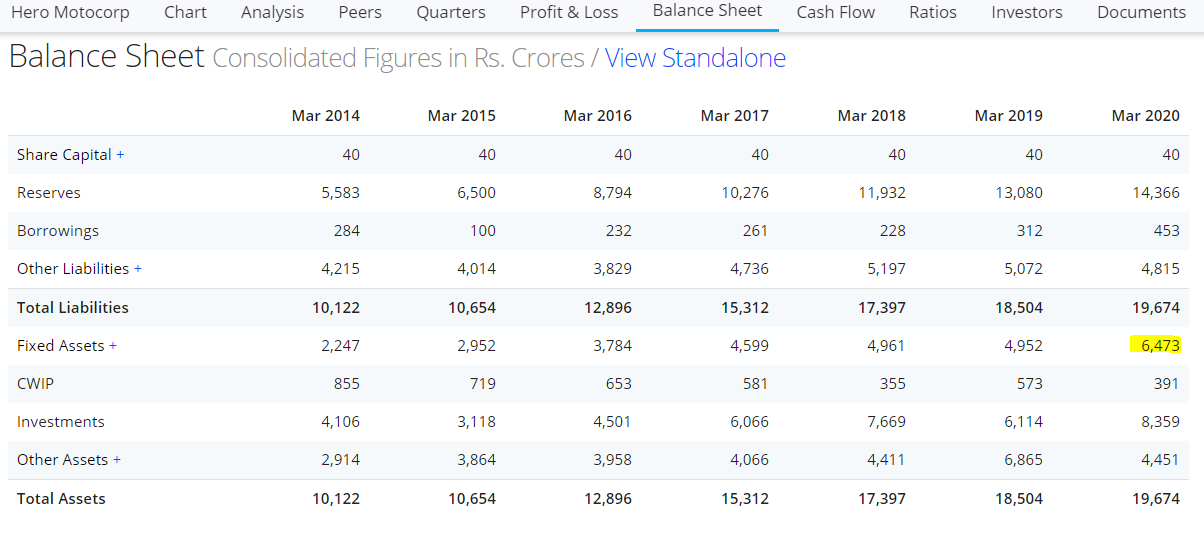

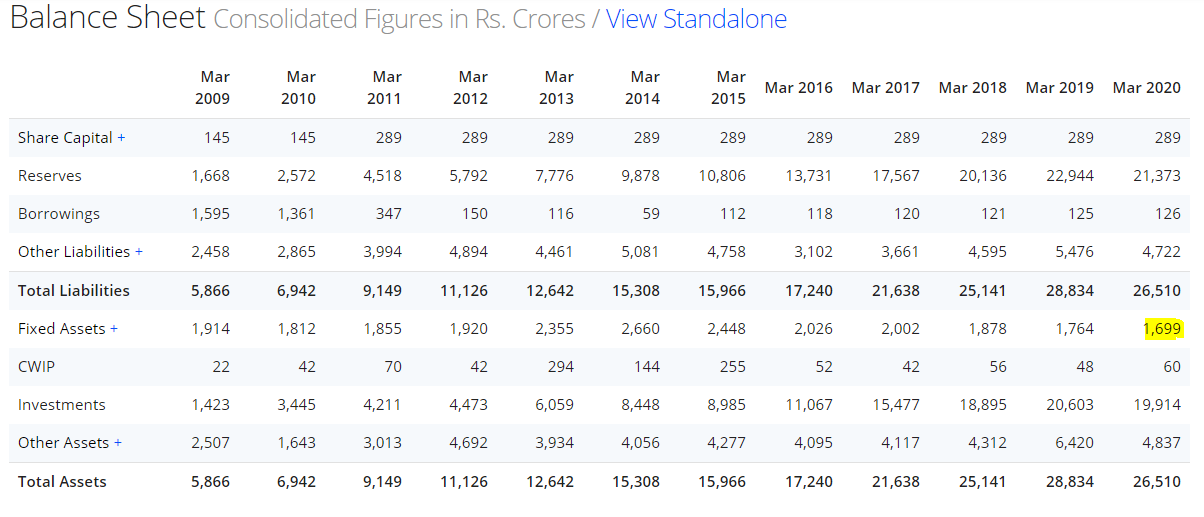

While Bajaj Auto’s fixed assets is ~ 2000 Cr, Hero Moto has 6500 Cr Fixed assets.

Question:

Why Hero requires such high Fixed assets compared to Bajaj? Or why baja requires so low fixed assets than Hero?

Can someone help?

Bajaj Volume

Hero Volume

Hero Balance Sheet

Bajaj Balance Sheet

Festive updates for Bajaj (link)

| o | Over last 9 days, domestic motorcycle sales down by 3% |

|---|---|

| | 100cc city & platina: Down 30% YOY |

| | 125+cc: 28%+ YOY growth |

| | KTM and other premium brands: 25% YOY growth |

| | 3wheeler: Down 60% YOY (Diesel portfolio has done well) |

| | Exports: Headed for 230’000 vehicles this month (15% MOM growth) |

| | Overall ~500’000 vehicles in October |

| o | MEIS hit has been ~300cr. this fiscal year |

Disclosure: Invested (position size here)

| - | October update (link) |

|---|---|

| o | Festive season sales from retail is flat YOY, growing very well in premium (125cc+) bikes @30%+ rates but de-growing in the entry level segment |

| o | Market share has improved from 10% to 20% in the 125cc segment; maintained market share in the 150cc+ segment; gained market share at the very top segment (KTM); lost market share in the entry vehicle segment |

| o | Rebounded really well in the international markets; Africa is back to 95%; Latin America is back to 90% level; South Asia is back to 80-85% (Sri Lanka is down because they banned certain imports); Asean market (especially Philippines which is very important for Bajaj auto) is still at 50-60% levels |

| o | Looking to break international sales record of October in November |

Regarding difference in fixed assets, Bajaj Auto does lot more outsourcing of components and relies more on partnerships and follows a relatively asset light model. Bajaj Auto has primarily focused only on motorcycles. Also take notice of the number of plants that Bajaj has versus that of Hero.

Summarizing the last few interactions of management with media

- ET (01-12-2020)/Nirmal Bang (03-12-2020)

o Oct-November: Retail sales are about 10% lower in 2020 compared to 2019, the expectations of OEMs have not been met

o Higher cc bike segments have done much better with growth (125 cc has done well)

o Want to maintain 35 days inventory at dealer network (currently at 41 days; need to correct to bring it back to normal levels)

o Africa demand is back to 95%, Bangladesh is doing well; Latin America back to 85% levels (higher profitability market for bajaj auto due to higher realizations); Export demand back to over 200’000 bikes each month (could have done 25% higher sales if not for supply chain constraints)

o Sri Lanka is facing economic problems and government has stopped imports until 2021 (forex exchange crisis)

o Import 3-4% of raw materials

o Chetak has faced immense supply chain problems (as a result unable to cater to the demand for chetak)

o Retail financing has been lower by 10-15%

o 3-wheeler has come back to 60% levels; people mobility is back to ~80% levels - ET (24-12-2020)

o KTM volumes have gone up from 65’000 motorcycles in 2007 to 300’000 in 2020

o KTM has witnessed very strong growth internationally ranging from 30-100% in different geographies because people in lower strata in developed countries are shifting from public transport to motorcycles (125-400 cc range). Said want to go big in Mexico (Hero announced on 27.01.2020 their forey into Mexico; may become a competitive market)

o Indian motorcycle market is well penetrated

o MEIS hit for company was 250-300 cr/annually

o Profitability has improved due to higher contribution of higher cc bikes compared to commuter segment; entry level commuter segment has done worse than industry

o Future plans: upgrade an introduce new bikes over the next 2-years especially in the higher end segment; upgrade electric vehicle portfolio; want to do some work on micromobility with partner yulu

o Want to take exports from 200’000 to 300’000/month; Want to focus on Brazil market where Bajaj is not present - CNBC (02.02.2021)

o Retail sales have tapered off, pushing at the upper end of the portfolio (125 cc+). It is at 65% of portfolio now and has grown at 30%+

o Top half of motorcycles is performing very well, have lost market share in lower half of portfolio

o Export markets have come back very nicely except for ASEAN

Disclosure: Invested (decreased position size recently; latest position size here)

It’s a treat to read Rahul Bajaj, the reason I have a small stake in B A.

The article is taken from an email from Intelsense Capital Blog by @basumallick. Thanks, Abhishek.

Worth reading it…

Good Points .

Since I had issues with their underinvestment in EV and no progress on Qute I had reduced my position …

Attended AGM Yesterday … I raised these points with Management . Management response

-

Current EV investment ( for Chetak) : Rs 30 crores … Will invest in capacity only if market demands pickup …

The bigger focus is getting product right and have adaptability to expand fast if needs arise … Not concerned on what competition is doing -

Qute issue was with state level regulation and hurdles Plus BS 6 … Will be aggressive post Nov 22

With moving the EV business to a new subsidiary, will focus increase ? I hope so.

I think there is a big question mark on the terminal value of Two wheeler with IC Engine

https://blog.olaelectric.com/eraofev/

Dilemma

Its too early to judge the success but you cannot wait to judge it later…

To me this looks like a Ola PR gimmick… till date they don’t have any dealership, no local service stations, no one has test driven their vehicles (except some very small media event).

It is too good to be true that highly demanding and value conscious Indian customers are booking 4 untested Ola scooters per second just because it is available on Ola app.

Bajaj Auto veteran in 2 and 3 wheeler with history of more then 50 years and cash of more then 25000 Cr is selling around 2000 EV annually and a 36 year old entrepreneur Bhavish Agrawal of OLA has sold 60000 EV scooter in a day…

Hats off to him and to his entrepreneurship efforts…

His claim may be grossly exaggerated but even if I discount it by 90% it comes to 6000 which is 300% of annual sales made by Bajaj…

We need this kind of animal spirit in India… He has dared to claim that he will sell 2 Million units annually and subsequently to 10 million units…

PE funds have faith on Bhavish and therefore funding his projects…

One difference between Ola and Bajaj is that, Ola doesn’t need to make money, doesn’t have worry too much about corporate governess or return ratios, etc. and can get away by making exaggerated claims.

By the way, Bajaj took Indian motor cycles all over the globe when no one thought about it and made India a force to reckon with in two wheeler industry across the world in spite of excessive competition from Chinese players. I am sure they will figure out this game as well.

Anyways, as retail investors, we don’t have access to Ola business yet and therefore our interests are aligned with Bajaj’s success (or of Hero / TVS).

By the way, here are a couple of interesting reads on Ola.

Disc: Invested in Bajaj from lower levels.

All startups burn money and if investors are still infusing money they would have some reasons…

“Ola Electric raised Rs 300 crore ($42.2 million) from Matrix Partners, Ratan Tata and Tiger Global”

These are marque names and who are we to question their wisdom.

Agree, we are no one. Reading about Financial Shenanigans at Ola makes me wonder about the wisdom of so called marquee investors, however I am definitely no one to pass the judgement. Agree completely.

I am also biased towards established players like Bajaj / Hero / TVS as I don’t have opportunity to invest in Ola.

May the most efficient and ethical player win!

Daewoo used to be similar aggressive once. Chevrolet was in same league and now Ford joining the band.

Seltos lost all its spike to Creta recently.

Long term marathon is much appealing then 100mtr race while we evaluate the stamina.

Similar fate got visible in telecom where more aggressive and exaggerated operators vanished overnight.

100s of such spikes vanished in air.

I believe the long term performances should be accounted over spiked one’s…

Investing is a long term phenomenon.

Electric Two Wheeler Sales 2021 Jan To Nov - Hero, Ather, Revolt, Okinawa, Ampere.

https://www.autopunditz.com/two-wheeler-sales-figures

EV growth story particularly in 2 wheeler segment is gradually picking up…

YOY sales on monthly basis is falling for 2 wheeler ICE. EV may be one of the reason as people would rather then buying new ICE 2 wheeler would prefer to postpone their buy for another 12 to 18 months and buy EV vehicles.

Indians generally buy 2 wheeler for 8 to 10 years and they may be in a wait and watch mode and that may be the probable reason for fall in ICE two wheeler figures. If the fall continues for another 6 to 9 months then the irreversible trend will be confirmed…

Bajaj should now take proactive steps to capture the EV market. Ideally EV Chetak will not cannibalize their existing Motor cycle business, It will first dent the Scooter market which is predominantly capture by Honda Activa. Infact Bajaj is not at all present in that segment.

Bajaj should have entered much before in EV scooter and regain its Number position in Scooter segment which it use to command for decades prior to 2000.

Has Bajaj missed this opportunity…??

Disclosure : Not invested but analyzing the EV trend.