(Branded as Style Baazar)

Value Proposition –

Affordable, trendy, and high-quality apparel, footwear, and lifestyle products tailored for value-conscious customers in Tier 2 to Tier 4 locations, offered through well-equipped showrooms with trial rooms, hassle-free exchange policies, and a seamless shopping experience

Table of Content

- What Made Me Look at This Company at First Sight?

Key drivers for initial interest in Baazar Style

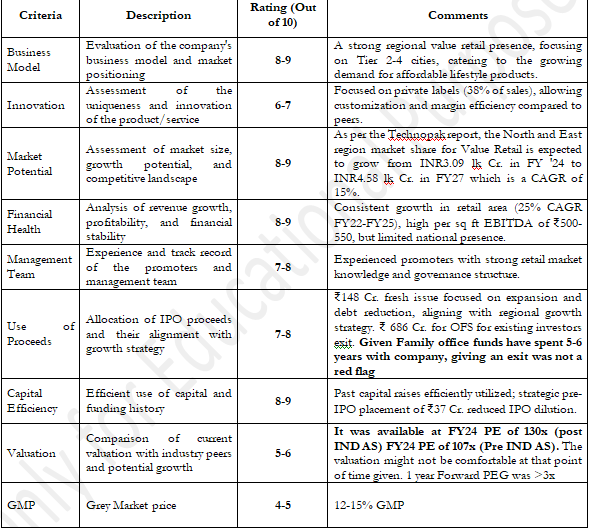

Summary of unique aspects and potential of the company - Dated IPO Rating Matrix

IPO rating matrix with metrics such as business model, innovation, market potential, and valuation. - Recent Management Commentary and Con-Call Highlights

Key insights from management’s earnings calls and strategic updates.

Updates on store expansion, operational performance, and future growth strategies. - Industry Overview and Competitive Landscape (Key Section)

Comprehensive analysis of the Indian value retail industry.

Growth trends, market opportunities, and evolving customer preferences.

Competitive landscape with a focus on Baazar Style’s positioning among peers like V2 Retail, Zudio, and others. - Valuation Analysis

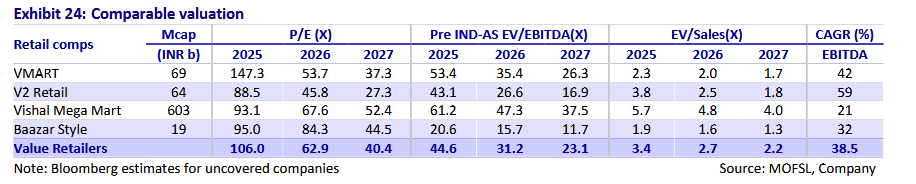

Peer comparisons using EV/EBITDA, P/E, and P/S metrics. - Investment Thesis

Summary of key reasons to consider investing in Baazar Style.

Catalysts for future growth, including market expansion, private labels, and omni-channel strategies. - The Story Behind Baazar Style

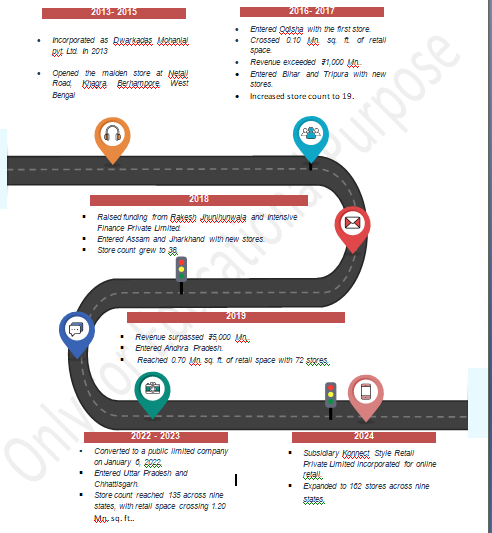

Founders’ profiles, vision, and leadership approach.

Key milestones in the company’s journey. - Business Model and Innovation

In-depth analysis of Baazar Style’s business model.

Discussion on its cluster-based strategy, private labels, and unique offerings. - Financial Performance

Analysis of revenue, profitability, and cash flows.

Comparative financial performance with peers. - Risk Assessment

Detailed review of operational, financial, and market risks.

Mitigation strategies and resilience factors.

What made me look at this company at first sight?

- Value Retail Industry Growth

- Industry growing at the

- Unorganized-to-Organized Shift : Capitalizes on the rising demand for organized value fashion in Tier-II and Tier-III cities.

- Scalable Store-Level Performance – H1 FY25

- Revenue per sq. ft .: INR 685 per month, up 19% y-o-y

- EBITDA per sq. ft .: INR YY,000, reflecting disciplined cost controls and solid operating leverage.

- Same-Store Sales Growth (SSG) : 21%, underscoring strong consumer demand and effective merchandising.

- Recent IPO & Comparisons with Industry Peers

- Public Listing: Follows the proven success of budget-friendly brands like Zudio and V2 Retail,.

- Capital-Efficient & Capital Light Business Model

- Positive Cash Flow (5+ Years) : Consistent operational cash inflows highlight prudent working capital management.

- Funds Raised: Since inception, ~INR 60 crore deployed strategically to grow store networks, strengthen brand equity, and optimize supply chains.

- Healthy Store ROI:

- Outsourced Manufacturing: Utilizes a network of regional and national suppliers, allowing for an asset-light model and flexible scaling.

- Historical & Projected Growth Rates

- High Double-Digit Growth :

- Projected Revenue growth & Margin Expansion Potential: Opportunities to improve cost efficiencies, scale sourcing, and invest in brand-building.

- Reputed Family Office Backing

- Credibility & Stability: Investments by notable family offices (e.g., Mr. Jhunjhunwala, DK Surana) not only bolster capital reserves but also provide strategic insights.

- First-Generation Professional Entrepreneurs

- Operational Expertise : Retail experience and pragmatic execution reduce common risks tied to new entrants.

- Customer Success & Retention

- Loyalty & Word-of-Mouth: Strong repeat purchase rates among middle-income families seeking cost-effective yet trendy apparel.

Basket Size Growth: Average transaction values continue to climb, reflecting increasing consumer confidence in the brand.

- Loyalty & Word-of-Mouth: Strong repeat purchase rates among middle-income families seeking cost-effective yet trendy apparel.

Dated IPO Rating Matrix

(Given I was asked about my opinion on IPO, what would I have done)

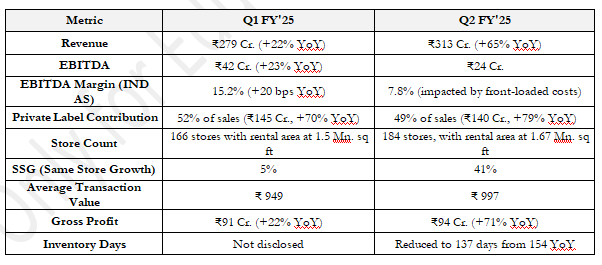

Recent Management Commentary and Con-call Highlights (2 Con-calls since IPO)

Growth and Expansion:

- Both quarters saw aggressive store expansions, exceeding guidance with a focus on cluster-based growth in core regions (e.g., Bengal, Assam) and forays into focus states (Jharkhand, UP).

- New stores contributed to higher revenue growth but incurred front-loaded costs, particularly in Q2.

Shift from Unorganized to Organized Retail:

Consistent commentary highlighted increasing customer movement from unorganized to organized retail, driven by demand for better shopping environments and brand consciousness at affordable pricing.

Private Label Strategy:

Private label contributions reached record levels, aiming for a 50%+ share. This focus on in-house brands supports margin growth and customer loyalty.

Operational Efficiency:

Inventory management improved significantly, with faster off-take during festive periods. The company achieved a reduction in inventory days YoY.

Future Guidance:

- Revenue growth guidance remains at 25% for FY’25, with PAT margins projected between 2.5% and 3% post IND-AS.

- Plans to expand store count further, targeting 45-50 new stores by year-end.

Challenges:

- Q1 faced exceptional loss due to a warehouse fire impacting profitability.

- Q2 margins were compressed by higher costs related to rapid store additions and festive season preparations.

Con-call Highlights

| S. No. | Investor Question | Management Answer | My Understanding |

|---|---|---|---|

| 1 | What is the store payback period and unit economics? | Average store size: 9,000 sq. ft., payback period: 16-18 months for CapEx, including inventory: 31-36 months. EBITDA margin for mature stores pre-IND AS at 13% | Strong unit economics with a clear path to profitability and scalability. |

| 2 | Why have margins contracted in recent quarters? | Higher costs due to 18 new stores and front-loaded expenses for festivals like Durga Puja. Expect profitability improvement in H2 FY25. | Temporary cost pressures tied to expansion; profitability likely to improve in H2 FY25. |

| 3 | How do you plan to scale store additions in FY26 and FY27? | Plan to add 40-50 stores annually, focusing on cluster-based growth in core and new focus states. | Strategic and measured expansion with an emphasis on enhancing supply chain and visibility in focus markets. |

| 4 | How is Baazar Style ensuring customer retention and loyalty? | Repeat purchase rates are strong among middle-income families, supported by attractive pricing, product quality, and regional campaigns. | High customer retention reflects satisfaction with offerings and loyalty-building initiatives, contributing to sustainable growth. |

| 5 | How are unorganized-to-organized market shifts impacting growth? | Significant traction from unorganized markets shifting to organized retail, especially in Tier 2-4 cities. | Sustained growth driven by increasing consumer preference for organized retail formats. |

| 6 | What is the marketing strategy to build brand visibility? | Focus on regional campaigns with local celebrities, BTL activities, and digital campaigns like YouTube hits in UP and Bihar. | Targeted regional marketing enhances local appeal and drives footfall effectively. |

| 7 | How is Baazar Style competing with peers like Zudio? | Zudio targets Gen Z with daily wear, while Baazar Style is family-focused, offering a broader product range, including ethnic wear and kids’ apparel. | Differentiated positioning as a family-oriented value retailer allows coexistence with competitors like Zudio. |

| 8 | How sustainable is the growth observed in H1 FY25, especially in SSG? | Same-store sales growth (SSG) guidance for FY25: 9-10%; long-term growth supported by loyal customer base and expanding clusters. | Growth is sustainable with strong contributions from both new and existing stores. |

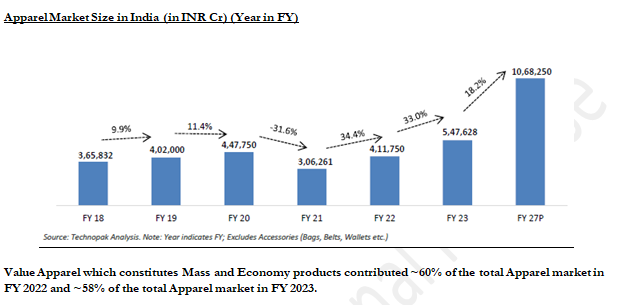

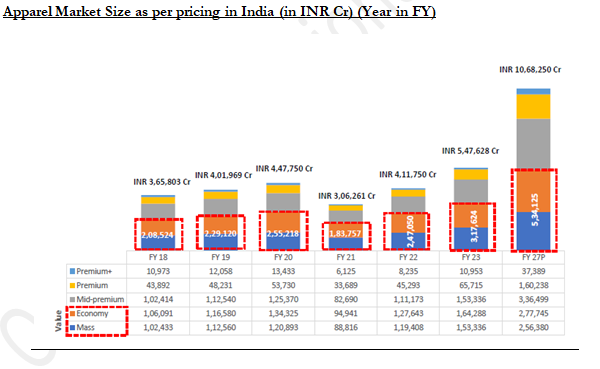

Industry Overview and Competitive Landscape

Retail Sector Growth and Opportunities (2023-2027)

Commentary:

The Indian retail sector’s projected growth from ₹7.61 lakh crore in 2023 to ₹11.35 lakh crore in 2027 highlights significant opportunities for value-driven retailers like Baazar Style.

Shift to Organized Retail :

- The share of organized brick-and-mortar (B&M) retail in categories like Apparel & Accessories and Footwear is expected to grow at 28% and 25% CAGR, respectively.

Apparel & Accessories Market :

- The apparel market alone is projected to nearly double in size, growing from ₹0.55 lakh crore to ₹1.07 lakh crore by 2027. Organized B&M’s share will grow from 18% in 2023 to 24% in 2027.

Footwear Growth :

- The footwear market, a key category for Baazar Style, is set to grow from ₹0.08 lakh crore to ₹0.15 lakh crore by 2027, with organized B&M retail’s share rising from 15% to 19%.

Unorganized-to-Organized Transition :

- The overall decline in unorganized retail (from 84% in 2023 to 77% by 2027) underscores the increasing preference for organized players, aligning with Baazar Style’s strategy of cluster-based store expansions in underserved markets.

E-Commerce Complementarity :

- While e-commerce is growing rapidly (CAGR of 24% across retail), categories like apparel and footwear continue to thrive in physical stores, particularly in Tier 2-4 cities, where Baazar Style dominates.

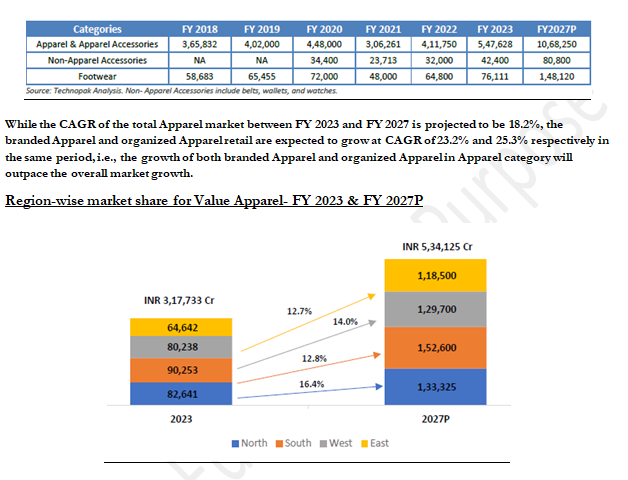

The Value Apparel market in East India is expected to grow at a CAGR of 16.4% from FY 2023 to FY 2027, which is the fastest among all regions. This is followed by the West region with a CAGR of 14.0%.

Potential for Value Retail in East and North India:

- The total market for Value Retail (Home & Lifestyle Segment) in North and East India was valued at INR 2,65,582 Cr for FY 2023 and is expected to reach INR 4,58,675 Cr in FY 2027. The level of overall organised play is also expected to grow from ~28% in FY 2023 to ~36% in FY 2027.

- These regions have the potential to accommodate ~8000 stores of Apparel Value retail chains by FY 2027. Currently, players like V Mart, Style Baazar, V2 Retail etc. dominate these regions in the Value retail market. For a single organised Value retail chain player, the region offers the potential to open approximately 800-1000 stores by FY 2027.

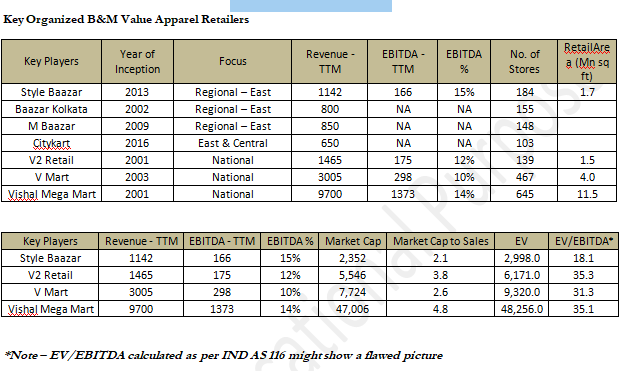

Competitive Landscape

Investment Thesis

Expanding Value Retail Market :

Key categories for Baazar Style, like Apparel & Accessories, are projected to grow at a CAGR of 28%.

Industry Tailwinds Supporting Growth :

Transition from unorganized to organized retail is accelerating in Tier 2-4 cities, Baazar Style’s core markets.

High-growth categories include Footwear (CAGR: 15%) and Home & Living (CAGR: 11%), which align with the company’s offerings and expansion strategy.

Dominant Regional Presence with Expansion Potential :

Strong foothold with 3.03% market share in West Bengal, 2.22% in Odisha, and 2.45% in Assam, showcasing ample room for growth in underpenetrated Tier 2-4 cities.

Aggressive expansion plans to add 40-50 new stores annually, with a current footprint of 162 stores (FY24) and 2.1 million sq. ft. of retail space by FY25

Efficient and Scalable Unit Economics :

Payback period: 16-18 months for CapEx, and 36-40 months including inventory.

Revenue per sq. ft. of ₹ 685/month in H1 FY25 , up 19% YoY, with 21% Same-Store Sales Growth (SSG) highlighting operational efficiency and strong demand.

EBITDA margin for mature stores: 14-15%, driven by disciplined cost controls and private label growth (~50% contribution).

Asset-Light Model with Private Label Advantage :

Focus on an asset-light approach through outsourced manufacturing, enabling flexibility and scalability.

Private labels (~50% of revenue) enhance margins, improve customer loyalty, and offer a competitive edge.

Strong Financials and Operational Discipline :

Revenue CAGR of 33% from FY20 to FY24, with management guiding sustained double-digit growth.

Positive operating cash flows for the last 5 years, reflecting efficient working capital management and profitability.

Strategic Investor Backing and Credibility :

Supported by reputable investors like Mr. Jhunjhunwala and DK Surana, ensuring financial stability and strategic guidance.

Proven ability to attract investor confidence for expansion and operational upgrades.

What is Baazar Style Retail Ltd

Baazar Style Retail Ltd. is a leading value-focused retail chain specializing in affordable, trendy, and high-quality apparel, footwear, lifestyle products, and general merchandise. The company operates across Tier 2 to Tier 4 cities, primarily targeting value-conscious customers in underserved regions of India.

Employee – 2600+,

Office space - 30,000 square feet

Warehouse - 1.8 lks square fee

Key Features of Baazar Style

Product Offering :

A wide range of clothing, footwear, home decor, and lifestyle products designed to cater to middle-income families.

Menswear, Womenswear, Kidswear and all household related articles, plastic wear, toys etc.

Private Labels:

Significant contribution (~50%) from private labels, enabling cost control and higher margins.

Square up is one of the largest brands in the private label which stands at INR117 Cr. of revenue as on FY '24.

From FY20 to FY '24, private label segment has experienced growth of 64.6%, contributing to 38% of our overall revenue. These have also enabled to achieve better profit margins

Geographic Focus :

Stronghold in Eastern India, with operations in states like West Bengal, Odisha, and Assam.

Have a decent presence in focus states like Tripura, Jharkhand, UP, Andhra Pradesh and Chhattisgarh.

Aims to bridge the gap in Tier 2-4 cities where organized retail is still emerging.

Customer-Centric Approach :

Features like trial rooms, hassle-free exchange policies, and a family-oriented product mix enhance the shopping experience.

Growth Trajectory :

Rapid store expansion with a cluster-based approach.

Clusters help to optimize marketing expenditure, supply chain expenditure and optimize on the inventory side.

Focused on maintaining efficient inventory turnover and improving operating margins.

Strategic Strengths :

Backed by reputed investors, including family offices like Mr. Jhunjhunwala.

Asset-light business model leveraging outsourced manufacturing for flexibility and scalability

About Baazar Style

Pre-requisite - How to read financials of Baazar Style

Leases (IND AS 116) :

Lease expenses are capitalized as Right-of-Use (RoU) assets and liabilities, shifting expenses below EBITDA.

Impact on EBITDA : EBITDA as per IND AS is inflated compared to IGAAP, as rental expenses are excluded. For Baazar Style, PAT is impacted by ~0.5% due to IND AS 116 adjustments.

Relevance of IGAAP EBITDA : In value retail, IGAAP EBITDA provides a more realistic view of operational profitability since it accounts for actual lease expenses.

Revenue Recognition (IND AS 115) :

Revenue is recognized based on performance obligations, ensuring alignment with the timing of actual sales.

This approach reduces discrepancies between revenue recognition and cash flow realization.

Working Capital Analysis

Working capital efficiency is critical for Baazar Style’s scalability and profitability in the value retail segment.

Debtors :

- Close to 0 days as Baazar Style operates on a cash-and-carry basis. This is typical for retail businesses, ensuring strong cash flow.

Inventory Days :

- Most critical metric for value retail companies. Lower inventory days indicate faster inventory turnover and efficient demand-supply matching.

- Baazar Style has improved inventory days, reducing from 154 to 137 days in FY24. This reflects better inventory management and aligns with market demand.

Payable Days :

- Given the low bargaining power of suppliers, Baazar Style can stretch payable days without impacting relationships.

- Longer payable days reduce working capital requirements, freeing up cash for growth.

Overall Working Capital Days :

- Efficient management can result in 0-100 working capital days, depending on inventory turnover and payable management. Baazar Style’s ability to operate with minimal debtor days is a significant advantage.

Sales Metrics

Sales per Square Foot :

- Baazar Style reports sales per sq. ft. on a gross value basis.

- To reconcile Net Revenue:

* Multiply Sales per sq. ft. by the average sq. ft. of operational space. - This metric is vital for assessing store-level efficiency and profitability.

Same-Store Sales Growth (SSG) :

- SSG of 8% for H2 FY25 and 5% of FY26 is considered while building P&L Projections

Key risks

Competitive Intensity

- High competition from organized players like Zudio, V2 Retail, and e-commerce platforms.

- Pressure to differentiate through pricing, product variety, and in-store experience.

Consumer Behavior Shifts

- Rising adoption of e-commerce in Tier 2-4 cities could divert traffic from physical stores.

- Changing preferences towards fast fashion or premium brands could reduce demand for value retail.

Geographic Concentration

- Significant reliance on key regions like West Bengal, Odisha, and Assam.

- Underperformance in these markets could adversely affect overall growth.

Inventory Management

- Mismanagement of inventory could lead to higher inventory days and working capital strain.

- Seasonal and festival-driven demand fluctuations increase the complexity of inventory planning.

Economic Sensitivity

- Value retail is highly dependent on consumer spending patterns, which can be impacted by inflation, unemployment, or economic slowdowns.