ROE & ROCE are around 7-8 % and revenue growth is 30% more. This will need additional funds for growth. It will be either with dilution or debts. Will it be sustainable.

Disclosure: Invested but still in confusion

ROE & ROCE are around 7-8 % and revenue growth is 30% more. This will need additional funds for growth. It will be either with dilution or debts. Will it be sustainable.

Disclosure: Invested but still in confusion

Pre Ind AS ROE is 18%, with 40-50% of the stores opened in the last 12 months and not being at full potential, store level ROE for older stores stands at >25%

Any view on the remuneration is severely misaligned with profit growth?

Executive remuneration grew 12.5 times faster than profit, with remuneration increasing 50% while PAT grew only 4%.

The company appears to be rewarding management for the IPO event rather than sustainable profit growth, which is concerning for long-term investors.

STYLE BAZAAR:

Generational shift: Even in TIER 2, 3,4 cities , nobody wants to buy clothes for mom pop shops given variety, cost, bargaining, experience and decreasing relations and no pressure of coming out without buying .

Store Level Matrix: Capex cost is 1.25 cr . Inventory is mostly funded from payable days. Even if I assumes overall 2cr is required for a store which will generate 10 cr sales and Pre IND AS EBIDTA of 14% , which gives 60-70% ROCE. Note: At company level corporate cost is 5-6% .Therefore at company level Pre IND AS EBIDTA is 7-8%.

Sales per sq ft: Approx 800 when company is present in WB , Bihar , Orissa and Assam . As the company moves towards northern belt sales may increase due to per capita and Winter effect.

3.Growth: SSSG of 7-10% , And organic store expansion of 20-25% . Any fund raise or debt will further accelerate the growth.

Cylicality : Today skewed towards Q3 due to durga puja , but will decrease as company will open stores in other state

Operating Leverage : Corporate expense today is 6% , As Number of stores increases it may be halfed to 3%, Increasing PAT margin to 7-8%, which in turn trigger ROE and PE

Growth Longevity - Atleast 10X stores can be present as of today(250). Vmart has 170 stores Just in UP.

Valuation - Company is available at .9X forward Sales to Mcap , While V2 at 3X and Vmart at 6X

8.Managment : HIghly conservative and making front loading investment on people , processes to reap future benefits. (Marwari managment shifted to bengal)

Disc: Invested and may increase or dec in future

People always talk about not cannibalising your own sales, but Baazar Style Retail basically just threw that rulebook out the window. They went ahead and opened 25 new stores right near their old ones, which, yeah, caused an 8% dip in same-store sales for a bit. However, the total revenue for those clusters actually increased by 52%.

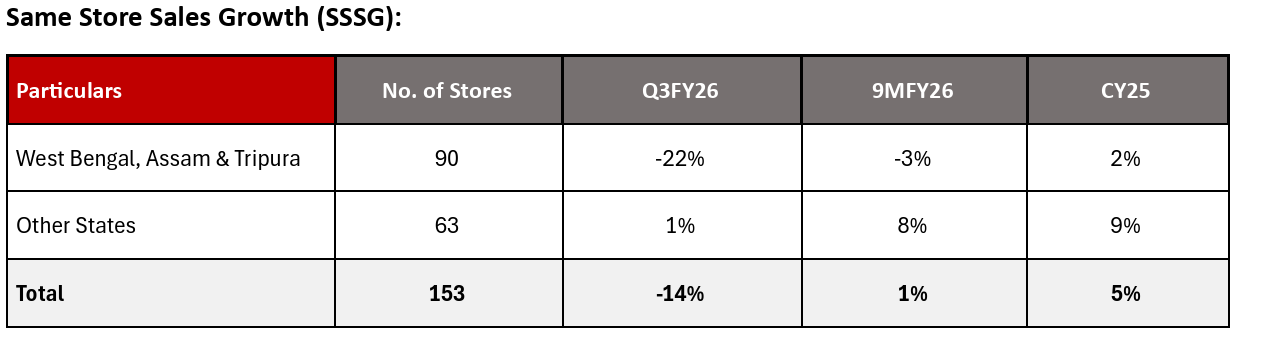

Honestly, if you just look at the Q3 headline number, that -14% SSSG looks a little scary.

But it’s mostly just a calendar trick because of when Durga Puja fell this year. Once you factor that in, plus all the floods and unrest they had to deal with, the business looks pretty tough.

They’ve managed to hit 252 stores now, which is like a 27% jump.

The company is growing fast by opening many new stores, with 252 stores and 38% revenue growth, and it operates in a fast-growing value fashion market. However, the business is not using capital efficiently, which is a major concern. Even though sales are growing strongly, the stock is still down 26% from its IPO price, showing that the market is reasonably worried about whether this growth is actually creating long-term value at current valuations.

Disc : Currently invested and may exit in the future.

Expecting a good Q4 from them, remember Bengal elections in March and Eid too is in March. During elections the state will be flooded with elections money and a Bengal heavy retailer like BSR should benefit immensely.

Add this to the list - Cold snap fires up weak winter sales across north, east India - The Economic Times

1/3rd costs of style bazaar are fixed cost(Rents , employee ,HQ). which are only inflationary.

Any more than 4% (inflation) increase in SSSG will be reflected in EBIDTA as 33% compared to present 7-8%(Pre- Indas) leading to Operating leverage.

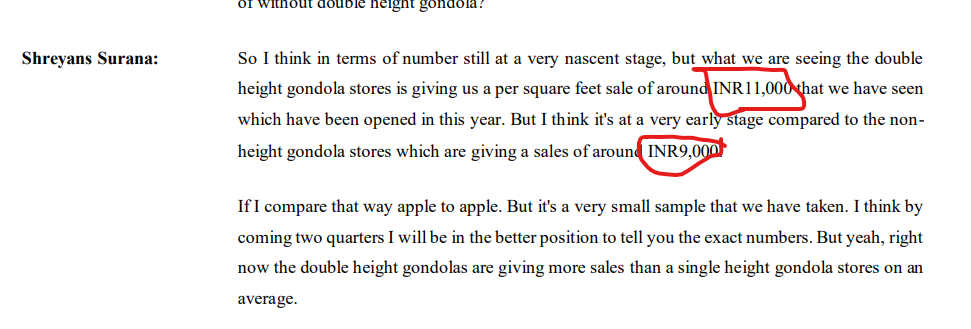

SSSG is key monitorable for Mature stores (how much more than 4%), while SPSF will determine overall store performances including new ones . Can Double height gondola increase SPSF from 9K to 11K .

Managment making significant software and warehouse investment and Single investor Warrants at 330Rs (Current CMP:240) indicates some confidence .