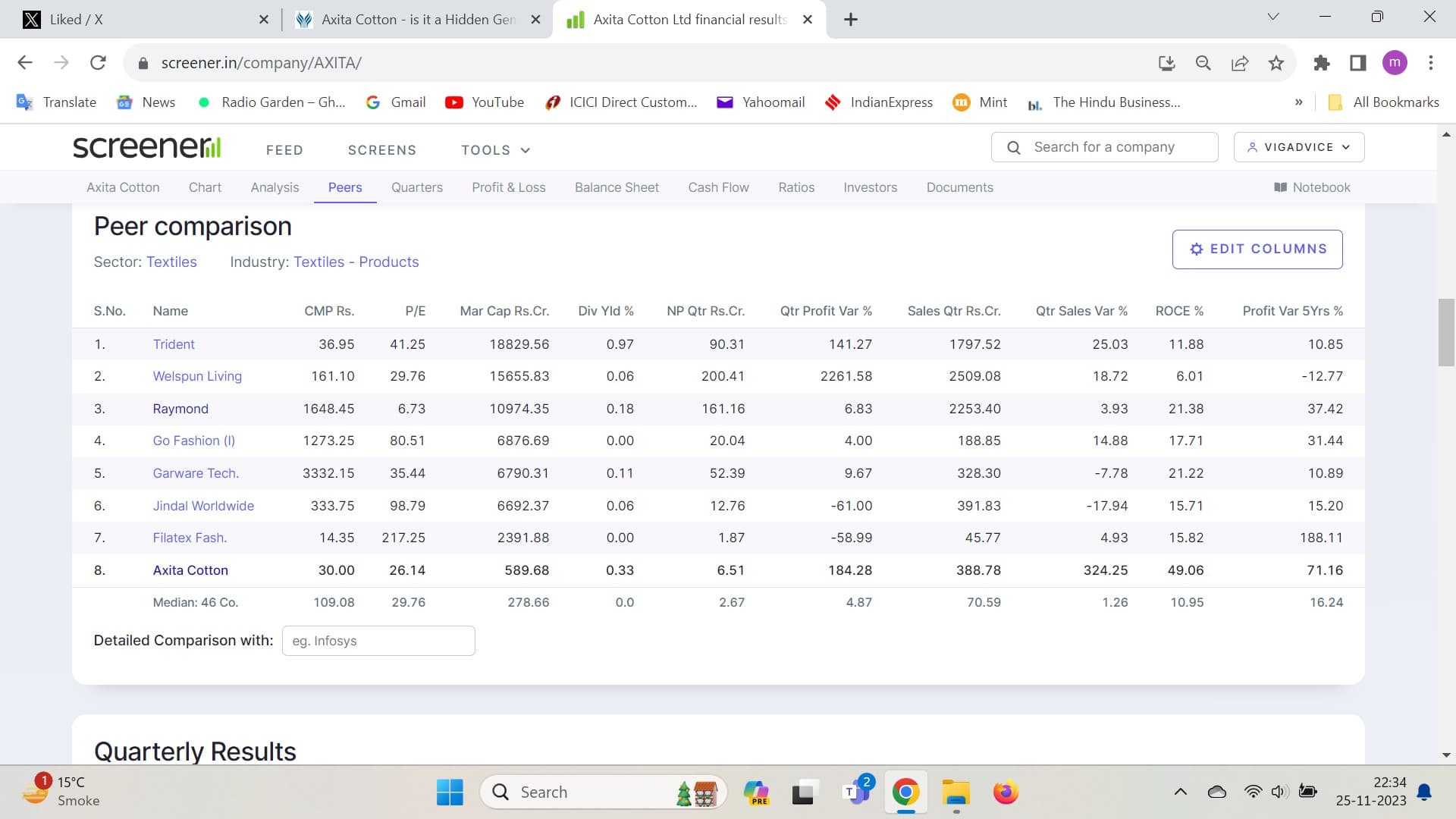

Axita Cotton – A cotton Bale manufacturing company. It is also engaged in trading and export of Raw cotton Bales and seeds. Cotton Bale consists of 15 percent of sales. Customers are wholesalers. Export customers include Big fashion houses These are used to make branded apparels, fabrics etc.

-Incorporated in 2013-14 as a Pvt ltd firm

-2015-16 Introduction of Organic Cotton segment

-2018-19 - Generated over 100 Cr revenue in sales conversion into a public Ltd company. Went public

- Associated with organizations like lobal Organic Textile stds, Better Cotton Initiative, GCCI, TexProcil, Global Recycled Standard

- Production location in Kadi, Mehsana and remains operable for 8 months a year.

- Focus on Environment sustainability, biofertilizers, crop rotation , hand picking to reduce environmental impact

→ Introduction of cotton yarn in product portfolio in 2022

→ share split of 1:10 in August 2022

→ Buyback of 900000 Rs worth of shares in May 2023

→ No subsidiary, Associate or JV

→ caters to 8 Indian States and 12 different countries

Why Attractive?

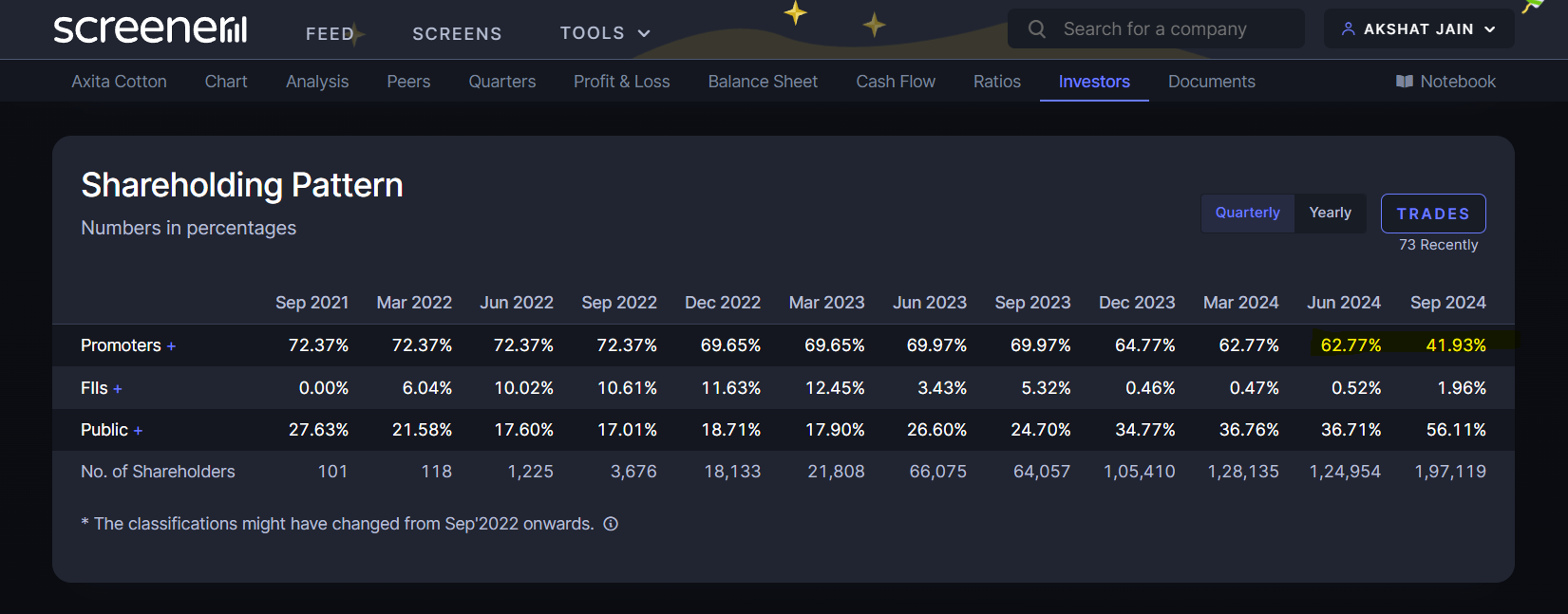

- Fair promoter holding around 70 percent

- Total Reserves and Surplus increased from 16.82 to 32.71 YoY

- Total Shareholders funds increased from 36.48 to 52.37 YoY

- Trade Payables has reduced significantly

- Tangible assets increased 3 times

- Trade receivables decreased considerably from 73.42 crores to 44.15 crores

- Increase in Cash and current assets

- Cost of materials sold reduced from 13 to 1. is it good or concern?

- Profit increased considerably over past few years.

- Clean management, Auditor has given no adverse remark

- China plus one strategy and govt initiates working in favor

Declared Bonus shares

Gave Dividend in 2022 and 2023

NITINBHAI GOVINDBHAI PATEL being reappointed as Chairman cum MD

Concerns/Threats:

1. High water need, uncertainity of monsoon.

- High cost of Raw matrials

3. Other long term liabilities and long Term provisions introduced to 6 Crores as compared to 0 in 2022.

-

current Liabilities has increased considerably

-

Revenue from operations reduced for first time since 2019

-

P/E high at 64.89

-

high cost of organic cotton

-

Lack of availability of organic cotton (overall industry). Global demand for organic cotton exceeds supply. This can lead to shortage and price volatility.

-

Only one plant location in Kadi, Mehsana - prone to Disease or area specific challanges?

-

Exposed to Commodity risks - Such risks are managed by tracking the commodity prices on a daily basis taking physical position of commodity as well as entering into fixed price contracts with the domestic and overseas suppliers in order to hedge price volatility.

As per MoneyControl:

I request experts to put their view on this stock. I went through the reports and find it interesting.

Disclosure: Not holding any stock. Just for study