well, nothing wrong in being optimistic, on lighter note..a third way to look at it can be that now even the middle class in India is able to afford Audi (and SUVs of course)…as I said nothing wrong in being optimistic

(I am imagining how a bag full of groceries and ashirvaad aata would look in an Audi’s trunk )

In FY25, the company added 50 stores, taking the total to 415 stores. Total bill cuts in FY25 stood at 35.3 crore (v/s 30.3 crore in FY24), supported by stores addition. The management continues to remain bullish on the brick and mortar business along with e-commerce. The company is focusing on rapidly increasing the number of stores in the coming years. The management is seeing good opportunity in North India for store expansions, mainly in Uttar Pradesh (UP).

Dmart is now diversifying into Hotel business as well . They are coming with chain of hotels and aggressively acquiring space.

By the end of the FY they may start some of the hotels . They are coming up with budget hotel segments and targeting business hubs . Can this be a value unlocking step ??

Disc: not invested , just tracking it .

D-Mart itself has not officially announced a direct entry into the hotel business. Radhakishan Damani has investments in listed hotel companies. Maybe some news source would have been confused by it with that.

However, they have been aggressive in their F&B offerings in Vadodara, Gujarat, at least what I have seen near my Dmart, including First Popcorn, Ice Cream, and Now Pizza. Have also seen some stores in Mumbai with a Pharmacy.

They have recently finalised a land parcel at Surat from a prominent real estate group and construction has started where half of the area is for DMart store and half for hotel project .

I got to know from the reliable sources and u can say it’s from horse’s mouth .

This is a very interesting piece of information. Assuming the news is true, it could mean that they acquired a large land parcel in excess of their needs at an attractive price.

Now they have two options:

A: DMART is going to build the hotel, then lease it off or manage it themselves.

B: Lease the land to a hotel developer who builds the hotel, and DMART makes money off the lease income.

I am inclined towards option B, as it seems like a smart capital allocation strategy relative to option A, where the competency does not exist in DMart at the organizational level. Also, RKD is one of the most astute investors in India.

Thank you for sharing the information. Let’s see how it works out.

The hospitality sector is a very capital-intensive and cyclical business. Even the existing players, like Indian Hotels and ITC Hotels, are moving into an asset-light model of not owning but leasing the property and managing them. I hope DMart doesn’t venture into that space.

That’s interesting. Thanks for sharing. I think it is a good approach for DMart to cash-in on the influx of people, who might be tired and hungry at the end of their monthly grocery shopping.

The key is the ingredient. Domino’s Pizza Mania does not have real cheese to cut costs. They use cheese alternative made of oil. Here the board says real cheese.

Was at Dmart to buy Kellogg’s muesli but picked up this, thinking it was some new product of Kellogg’s, but to my surprise, it was Dmart’s Premia (in-house premium brand). The packaging and colors are becoming better than the earlier pale and minimalist type .

Saw this self ordering screens at my nearest Dmart in Bhopal. Previously it used to be like people all over the counter no queues or anything. Hopefully this is an upgrade to the after shopping experience for hungry people .

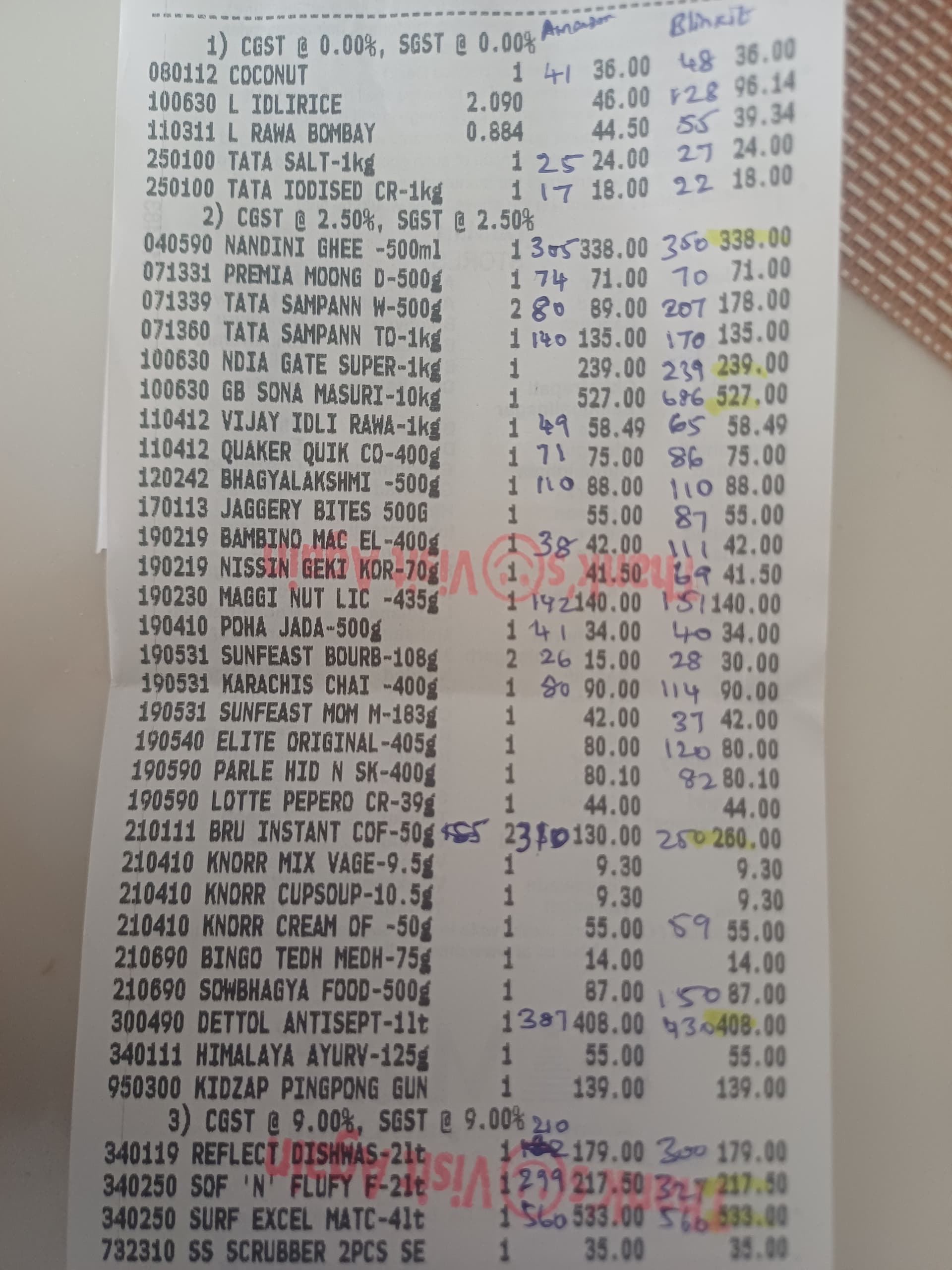

Though recent dip in prices concerned me a bit, the critical question i had is whether the price offered by quick commerce giants could dominate dmart’s. Was able to compare dmart prices against amazon and blinkit for the commonly available products. For the products that were not directly available in the quick commerce platform, the cheapest available products were taken as proxy.

This analysis summarized to me that dmart is the price leader even at this point. However, the stalling/reduction in the number of customers in their oldest stores could be attributed to the customers who are not that price sensitive or just liking the comfort of ordering from home instead of a planned visit to a nearby store. If later, its an alarming trend to any investor.

@vignesh_J Interesting take, but to me, the fact that DMart still emerges as the price leader even against heavily funded quick-commerce players actually strengthens the moat, not weakens it. Convenience can win some baskets, but in India, value has repeatedly proven to be the bigger habit-former over time.

The softer footfalls in older stores may look worrying in isolation, but I see it more as a channel mix shift rather than a loss of relevance, with incremental demand moving online, while the core value-seeking customer stays loyal. As long as volumes and economics at the store level remain strong, this doesn’t break the story for me.

A small parallel is Walmart in the US: every few years there were fears that e-commerce or newer formats would eat into its base, yet its relentless focus on lowest cost and execution kept compounding the business for decades. DMart’s culture feels closer to that playbook than to a retailer chasing growth at any cost.

So unless DMart actually loses its price edge or discipline on costs, I’m still bullish. Temporary shifts in behavior don’t change a structural advantage built over years.

DMART is making cash hands over fist and once the war in quick commerce and e-commerce settles down and if profitability emerges it can and will venture into it as it can fund the unit through internal accruals.

DMART is also planning to venture into pharmacy business (not manufacturing but I guess for distribution and retailing) which can be new growth vertical.

This strong cash reserves and cash generation capabilities make it immune to shocks.