Agree with most of the thoughts here.

We have to understand the changing dynamics here. DMart is not a compromise of convenience for cheaper prices any more, though that used to be the case. DMart’s clustering approach of stores, increase in size of stores that come up, and DMart Ready are the efforts in improving the convenience.

For example, I used to be a DMart B&M store customer, but it has been about a year I went to a DMart B&M store thanks to DMart Ready. This helps me to save time and avoid the crowds while still taking advantage of DMart’s low prices.

I believe a section of users will move from B&M store to DMart Ready. I think this preference is not specific to COVID situation. There are people who want convenience while still wanting low price for major portion of our monthly expenditure. Local kiranas will continue to hold the edge for quick low value needs and cravings.

Disclosure: Exited recently.

4 Likes

I was trying to express the perception of regular folk, the majority’s perspective. The complaints are more or less the same but they are answered with discounts.

And regarding the changes, Dmart does not fall under the category of ‘strike the iron while it is hot’ but rather of, we are in for the longest haul, so we will not waste any resources for the short term just because everyone else is doing. Dmart Ready is yet to become a Swiggy, catering to small towns. When people from small towns too get limited time in the future, they may opt for Ready. Until then, Dmart predominantly will remain a B&M chain. The land they purchase, and the constructions they build may very well be used for fulfilling centers, even if created for stores. So I don’t deny the expansion of Ready. And I believe the same operational efficiency will be displayed with Ready too when it becomes fully active.

But, if the changes with Ready or others don’t reflect in the numbers, the valuations will not remain as they are today. Probably the only recurring concern with Dmart.

2 Likes

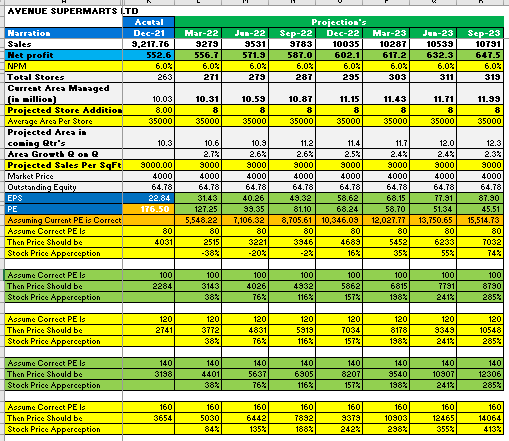

Avenue Super Working.xlsx (48.2 KB)

Self console exercise

Considering conservative numbers on below mentioned parameters, I am trying to assess what would be the best/worst price if mkt assume the PE is x or x-.

- Assuming every qtr, dmart will only add only 8 new stores

- Store size is 35000 even through the recent ones are 60K+

- NPM considered 6%. I think in coming days it will be improve through.

4)Considered per sq ft sale per qtr 9000 as against 9900 in Q3 and 10K in previous qtr

Outcome indicates what will be the price of dmart Qtr wise, if mkt assume the PE is 80,100,120,14m160 etc…

7 Likes

Dmart is not the story of a few quarters, so quarterly numbers although help in assessing the price, don’t necessarily provide the full picture. It is not just about opening stores, it is also about rented/owned stores, increase in fixed assets, further expansion plans, clusters or new areas, opening in new states etc.

Sales should increase in proportion to the past, even with new competition coming in. Margins should remain same, if not increase. Merchandise should expand in tandem with the tastes and preferences of people, higher margin goods should be part of sales, which should be accepted by customers and should increase.

A lot of moving, but relatively predictable to an extent parts, with strong management which is both clear and nimble, and with less retail holding, valuations may not always remain exorbitantly high but will be high relative to the market.

1 Like

Here is a report from Monarch AIF on high PE stocks. They have presented their views on some stocks which are trading at high multiples. Dmart is one of them.

2 Likes

Thanks for sharing this .I think EPS calculation is wrong from JUN-22 quarter onwards, EPS looks more than the net profit numbers. Can you please check.

It’s trailing 12 month EPS,

What I have done is

Previous trailing eps + current qtr projected EPS. In case of June Qtr the calculation is

31.43 + 571.9/64078 =40.20 and it continues throughout.

Let me know if I am missing something, I have also attached the excel for reference.

If I calculate 12 month EPS projection for Sept 22 quarter , It would be

552.6 (Dec 21)+ 556.7 (Mar 22)+ 571.9 (June22)+ 587 (Sept22) / 64078.

2267cr / 64078 = 35.37EPS

EPS should be 35.37 for Sept 22 not 49.32.

1 Like

Got it, my calculation takes 5 qtr… will modify the excel.

2 Likes

Can anyone please comment on why the ROCE (12%) and ROE (9%) for DMART look so depressed?

1 Like

Just my contrarian view: If HUL [one of the largest selling SKU brands in Dmart] takes a stance to deliver less to Dmart and more to Reliance Smart; won’t it have an effect on the share price of Dmart?

I think thinking on these lines would be quite interesting? I would appreciate your view on the same.

Why would HUL do that? You should have presented your views for this scenario.

How would HUL gain by this move? Would RS pay more than Dmart, or would they pay quickly than Dmart, or would they purchase more than Dmart? Even if it is profitable for HUL to do so, how long will it be profitable?

New competition will always exist for Dmart, and if this competition takes away business from Dmart, and if Dmart posts less profits continuously due to this, then the valuation will not sustain.

The same thing was done by Nike last week with Foot Locker, and due to that share prices of Foot Locker tumbled 30% in a week; citing that Nike wants to double down its D2C presence.

I don’t know about that. So can you draw a parallel between Nike-Foot Locker and HUL- Dmart. I cannot, as I don’t know about Nike-Foot Locker story.

What I can say is that, we are talking about 2 different geographies, 2 different businesses, daily needs vs partly discretion etc. Perhaps 2 different business models too? So think, it cannot be extrapolated here.

And it seems Foot Locker’s 70% sales come from Nike, is it the case with Dmart? I guess not. HUL is a dominant player in Indian FMCG space, perhaps number one in some certain categories, so if HUL does make such a move indeed, the material impact on Dmart should be considered, if there will be any. And market will surely react to this.

What is your view if HUL reduces it presence with DMART and DMART kicks HUL completely out. How much is that going to affect HUL.

These are scenarios which are completely out of anyone’s control. We should concentrate on scenarios that are in our control.

Cheers

1 Like

Firstly, I would not call it contrarian but rather hypothetical view and I think that although this is not in our control, but so is nothing. We don’t actually own any of the business we invest in and neither run them, so we must accept that actually - Nothing is in our control, beyond a point of mere buy, sell & hold decisions.

Therefore, it is good to discuss on such hypothetical views also as it makes us understand businesses better.

Few points that come to mind (and some of them common with @ChaitanyaC who answered them well already) -

- There is difference of being a Staples brand vs consumer discretionary/durables. Similarly, difference being the retailers of these two. Therefore, we cannot extrapolate the impact of such move in case of Nike/Foot-Locker Vs HUL/Dmart.

- Strength of Dmart is not presence of HUL brand and neither the strength of HUL brands is their presence in Dmart. Strength of Dmart is offering quality products at lowest prices possible. Tata Consumer, Marico etc. provide similar quality as HUL (just for example). Reliance Mart/Star also provide ample opportunities to HUL (Not to mention the neighborhood friendly Kiranaas who are above all at the moment.

- Therefore, Dmart would not make such move of removing HUL products as that would serve no purpose to them. Also, HUL would not remove their brands from Dmart (even if they want to push peddle on D2C strategy) as for Staples - more the distribution, the better. Competition will benefit if HUL ever makes such a move and Dmart would have enough levers (unlike maybe a Footlocker) to continue the consumer pull.

Just to give a perspective - When a consumer would enter Foot Locker store, he/she may have Nike shoes in mind even before he enters and may be hugely disappointed if didn’t get it but before entering Dmart, consumers may not have a Dove soap in mind. They would have just Soap (There would be some exceptions but most would have just soap, detergent etc .etc. in mind). Also, if Dove is not present, the disappointment would not be huge and they might try a Cinthol.

Thanks

5 Likes

Sanjiv Mehta, chairman and managing director at HUL, after announcing its results for the quarter ended March 2021, told investors that the company’s contribution from e-commerce stood at 5-6%, and the profitability of this channel is higher than modern trade, comprising supermarkets and hypermarkets.

Source :

1 Like

With due respect, every FMCG company is doing this. I think this (as well as threat to FMCG brands from Private Labels) has been discussed multiple times (and rightly so) and so far boils down to same conclusion that (good to revisit again as dynamics keep changing)…the ecosystem comprises of Retailers - both online & physical, FMCG brands, D2C, Private labels etc. and all are mutually inclusive, interdependent and coexistence is the key.

Wherever sub-segment/disruption throws more growth - both Retailers as well as FMCG brands will keep venturing and in a growing consumer driven economy, its good to be invested in both sector leaders.

Disc: Invested & biased. Not a buy/sell recommendation. FMCG & Retail form my highest holdings. I maybe completely wrong in all my assessments

Few new observations as DMart customer:

- DMart’s private labels are succeeding. We switched to Hand-aid, Clean Plus, Reflect, and Home chef (private labels of DMart). The prices are considerably less compared to popular brands (objectively), with no compromises on quality (subjectively).

- DMart’s loose groceries are considerably cheaper than packed one (same stuff).

- DMart Ready’s prices are on par with DMart store, never higher in my cursory checks. At times, DMart Ready prices are cheaper than DMart store (surprise!). Today I found Hershey’s Chocolate Syrup 200ml at DMart Ready for ₹75. It was ₹89 at the store (Over 18% higher price). I checked this is not due to change in MRP or the newer package.

I keep wondering why DMart Ready price for certain products is cheaper than the store. I suspect this could be due to DMart’s area/store specific pricing. Or could we conclude that DMart Ready is becoming cheaper than running the store?

Please do share your observations.

Disclosure: No holdings now. Tracking.

6 Likes

My personal observation (in Mumbai) over last couple of yrs is that prices across both Dmart formats are identical. This may be a stray incident of the physical store not updating the price /offer on a more real time basis.

1 Like