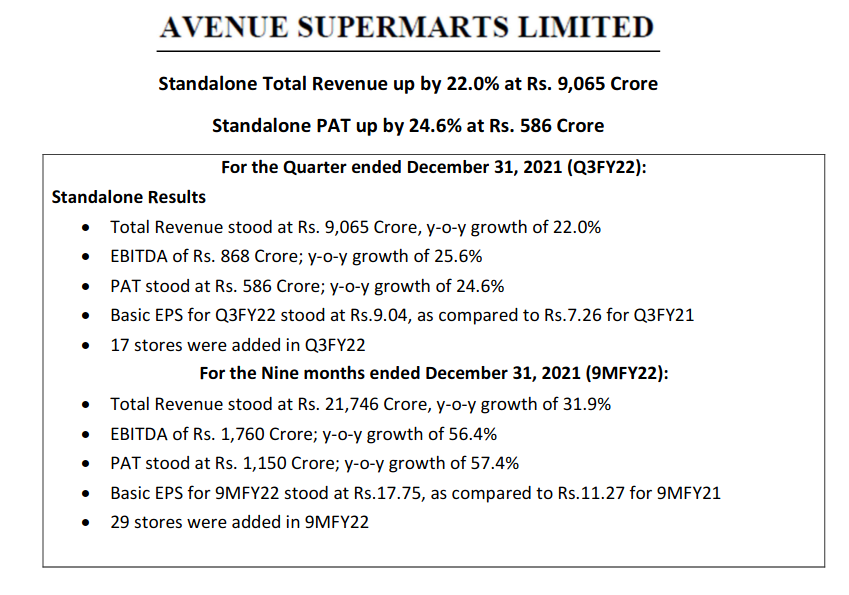

While the Q2 results have been very nice, today’s volatility in the price was surprising.

From +10% in the morning to -8% finally. Got a chance to add some more

Curious to know the reason for wild swing today, though whether its Axis Cap sell report or some instituational invrestor selling his stake.

While physical stores will be at full swing, I think they need to step up big time on Dmart ready(online version). I placed an order via DMART ready first time and they have evolved their delivery big time.

Like Big basket, they have dedicated delivery slots which is same day or next day. All the items were delivered.

Price wise, all the items were reasonably cheaper than Big basket or amazon fresh.This is where the USP of Dmart is. For example, Himalaya hand wash pack is Rs 84 compared to Rs 115 at amazon/BigBasket.

But, UI of the mobile app needs a big improvement. It is very basic at this point of time.

Tie-ups with credit cards/wallets need to be strengthened so as to get discounts which they are doing for sure.

I can see a seriousness in their online business now in the last 1/2 quarters which was missing earlier.

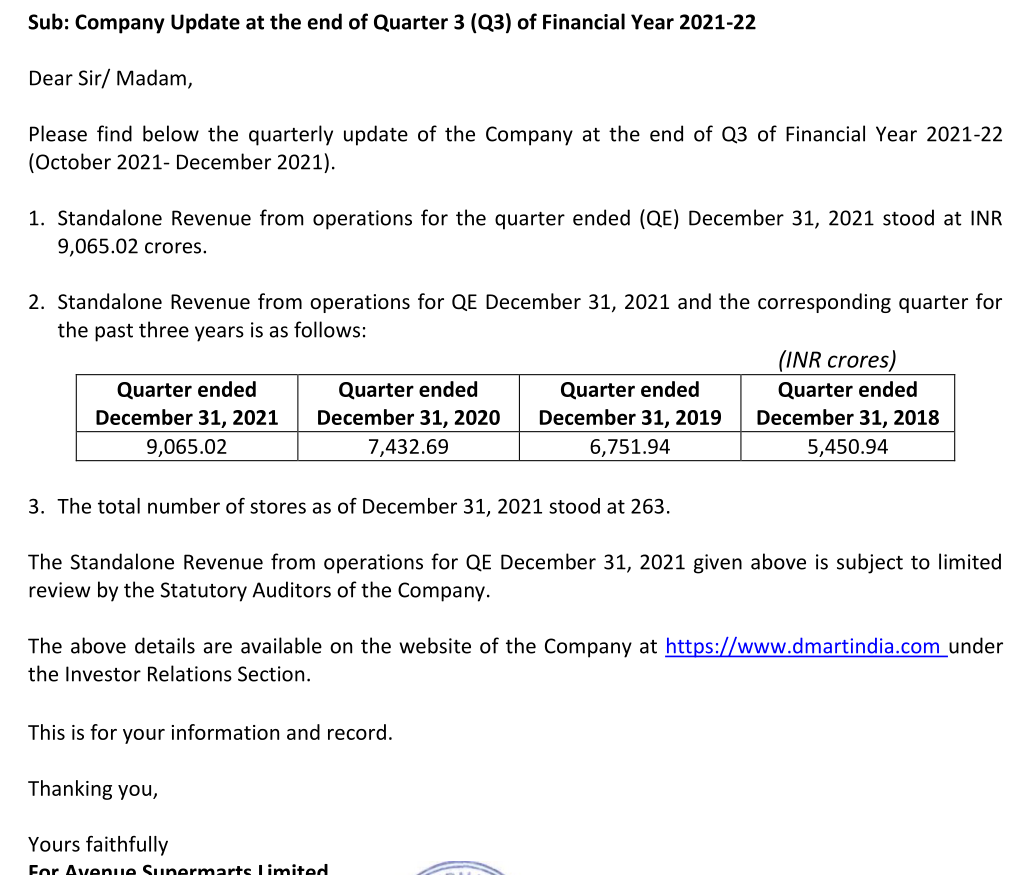

In Q2FY22, company did soft launch of D-Mart Ready in cities of Surat and Vadodara.D-Mart Ready is now available in seven cities: Mumbai Metropolitan region, Ahmedabad, Pune, Bangalore, Hyderabad and now Surat and Vadodara.

The business has got a huge runway. The way they are opening big hypermarts now like In Haryana recently, coupled with Online, I think 25% to 30% growth looks certain for the next 5 years.Lets see.

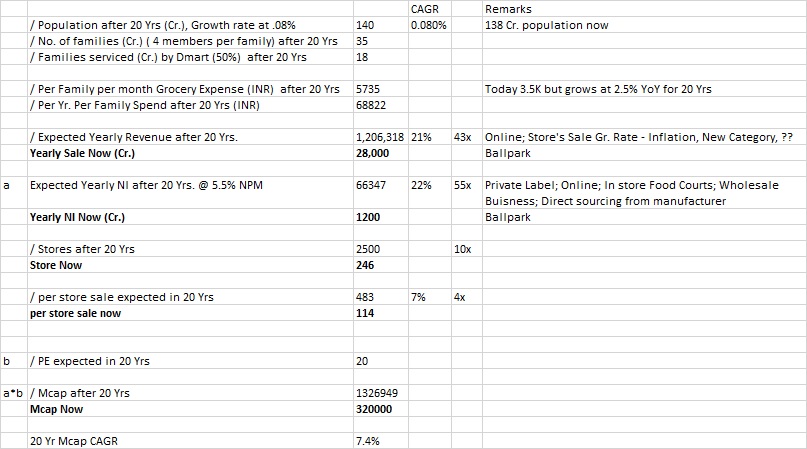

For all the valuation conscious folks, please do read this article.It made me stay with D-Mart since its listing. And I keep adding on at intervals.

Disclosure- holding and adding since IPO.