Material Development: It seems the company has assessed the business environment and re-started online Dmart Ready program in a lot of pincodes across the country.

I personally received a message stating that Dmart Ready is back for my locality (Pune)

I did login to checkout and this time the entire assortment (Grocery, F&B, Stationery, Home Appliances, Kitchen /Crockery/ Utensils ) have been made available for delviery.

If this is a long term vision to re-start Online business and for good, then it is a welcome move as this will help protect the downside of revenue loss due to Covid as well as Jiomart etc. As i don’t see the current state of its online business as an expansion move.

I don’t think it is prudent to bet against the future. And the future is e commerce for all branded products which do form a large chunk of Dmart sales.

I have no view on investing here but as a business if they want to be be as good as they have been in the last decade they need to have an online presence.

With the crazy PE multiples a gangster move could be to dilute equity and take over new age startups to bolster their online presence.

With the right vision investors have no issues with a little losses e.g Amazon.

Though if the current management is not adept at it then they could hire someone else for the online vertical.

Not invested but see this as a classic case of the old ways of doing things working so well that the company is reluctant to do things the new way.

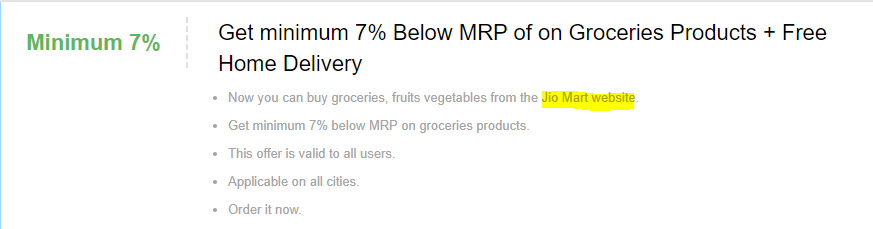

The competition of discounts is turning interesting, while Dmart has minimum 6% discount on all items… Jiomart started with 5% (plus free home delivery)

just saw this (looks like special for few days e.g. Ganpati Mahotsav) as their website is showing 5%

I sometimes wonder that is price everything for customers? There are so many things which I as a customer would need -

Quality of products - specially fruits and vegetables fresh or not

Quality of private labels - Packaging and product

Availability of sub-segments - If only grocery available or I can order more stuff like fruits etc.

Availability of brands of my choice

How clean the stuff comes and the feel when I open the packet. Many places you order and its filled with mud and dirt.

Convenience of ordering - personal touch would be better

Convenience of delivery - whether I get my slot and also if delivery person respect my time or deliver me bulk stuff at 10 pm in night leaving me to wash them till midnight!!! This has happened with me, I don’t want to name from where.

If above all satisfies, then I would pay a little more than MRP also as it saves me time, diesel and get stuff delivered at home.

Its NOT about any individual customer as Dmart has approx 20 crore bill cuts in a year and every customer will have his own preference. I guess all these 20 Crore visitors (no of customers will be different as each customer will have multiple bills in a year) loose their comfort / fuel cost / ordering from phone, app / delivery at comfortable timing etc and prefer to visit physical store to have the material of their own preference.

There is another set of customer, who shop as per their own choice but they are excluded from this analysis.

The core of the post is towards expected price war hitting the margin and nothing else. Do we see the 20 cr bill cuts getting a hit with this price war, which is already impacted due to covid?

Covid has already disrupted multiple businesses, with or without price wars and they quote losses but still stocks quote at excellent valuations because investors believe that once Covid is gone, things would resume as before. Couple of years of losses doesn’t seem to matter to markets in case of quality businesses.

Price war will add to the troubles no doubt about it, but can RIL/AMAZON compete in instore DMART after 2 years? Can they compete with the private labels quality of trent’s Star after COVID? Can they position themself as the best quality and cheapest instore (Dmart) or the best instore shopping experience (Star) after couple of years? If yes, I see serious threat to Dmart and Trent, if no then well RIL will compete with maybe a Super App yet to come after 2 years…till that time investors are fine with losses.

Pls note above are not just my thoughts but more of observations of investors and market conditions/movements.

There is nothing substantial in this article. A long read of the same old story and threats. Aldi - a discount broker is significantly smaller than Walmart/Amazon but has developed its own niche. As long as management knows what they are doing and keep running the business well, competition will be opportunities. Indeed, these are situations to be watchful as an investor. On a lighter note, from RIL- Future deal, Avenue moved one notch ahead from being number 3 to a numero two position

The contribution of Reliance Retail to the topline of a fast-moving consumer goods company (FMCG) before the Future deal was around 6 per cent, which has now increased to 9 per cent following the acquisition.

DMart, on the other hand, contributes just four per cent to the sales of an FMCG company, which is not expected to change in the foreseeable future.

I visited a Dmart store in a tier II city on Friday 09th of Oct.2020 at 1300 hours after reading a few articles that Jiomart is affecting Dmart in a big way.

The store was packed with customers even on a working day in the afternoon. Most of the customers were buying grocery & fmcg products. Garment , Crockery & Plastic sections were less crowded than usual.

I feel Grofer & Big Basket are facing more impact of Jiomart than Dmart.

The picture would be clear on declaration of July August Sept.quarter results on 17th October .

If anyone from the forum has recently visited a Dmart store in his/her city, please update your experience.

The short term impact may be somewhat clear in this and next Q results but actual impacts would be clear only couple of year or so. What would be important to see Dmart growth once coronavirus recedes. I am hopeful as physical retail is here to stay and grow and if that happens, Dmart will do well.

Disc: Invested, adding more on dips hence highly biased

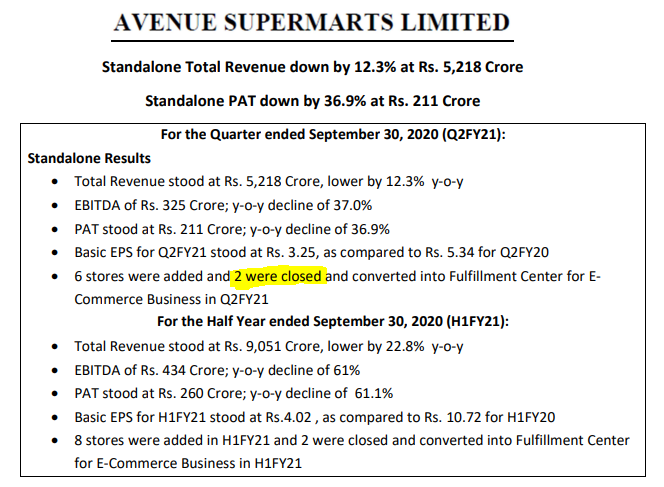

QoQ

EBITDA margin 6.2% vs 8.7%

PAT margin 4.0% vs 5.6%

H1FY21

Rev 9,051 vs 11730.

EBITDA 434 vs 1111

EBITDA margin 4.8% vs 9.5%

Net Profit 260 vs 669

PAT margin 2.8% vs 5.7%

Basic EPS 4.02 vs 10.72

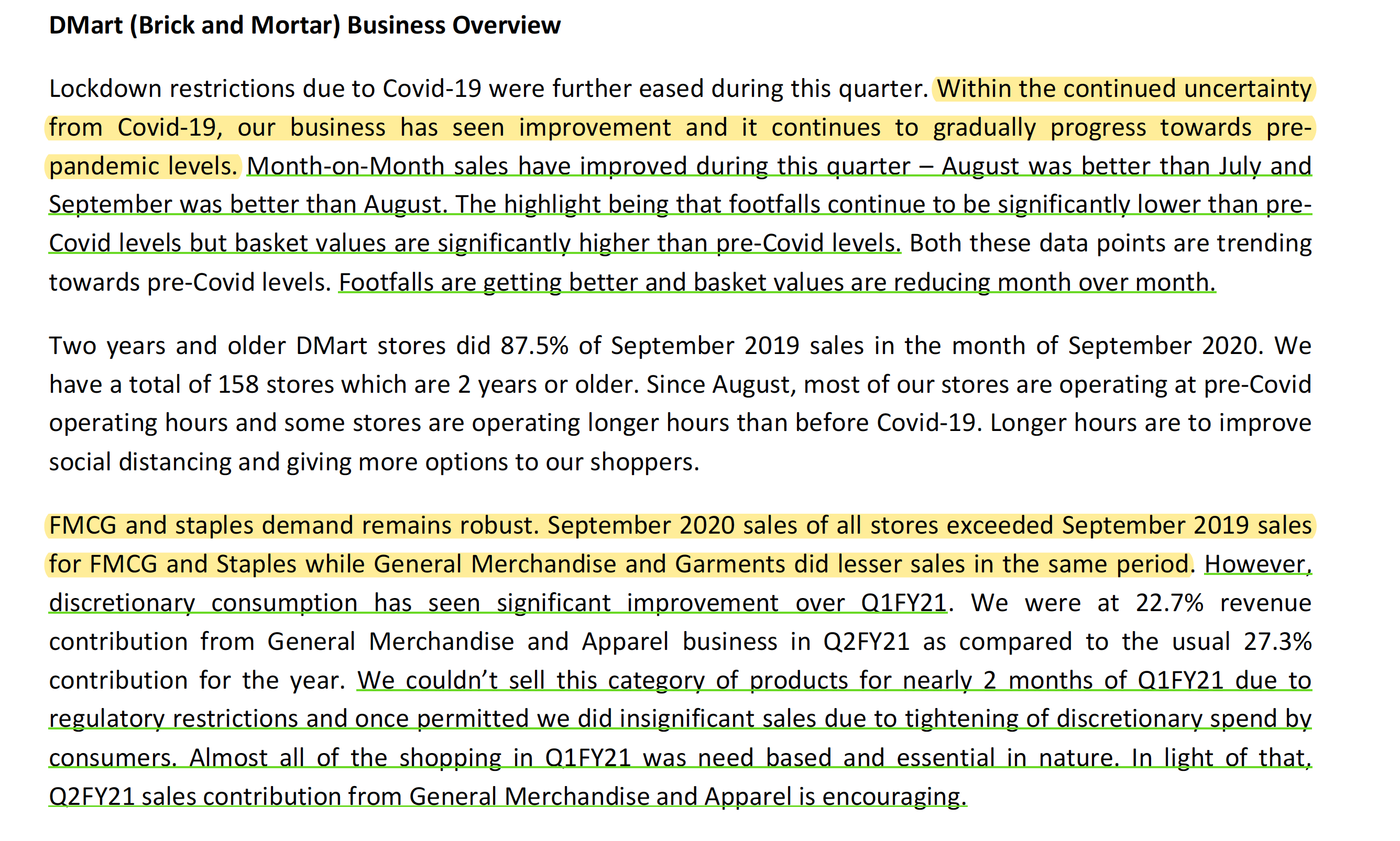

Month-on-Month sales have improved during this quarter – August was better than July and

September was better than August

Two years and older DMart stores (158) did 87.5% of September 2019 sales in the month of September 2020

FMCG and staples demand remains robust. September 2020 sales of all stores exceeded September 2019 sales for FMCG and Staples while General Merchandise and Garments did lesser sales in the same period.

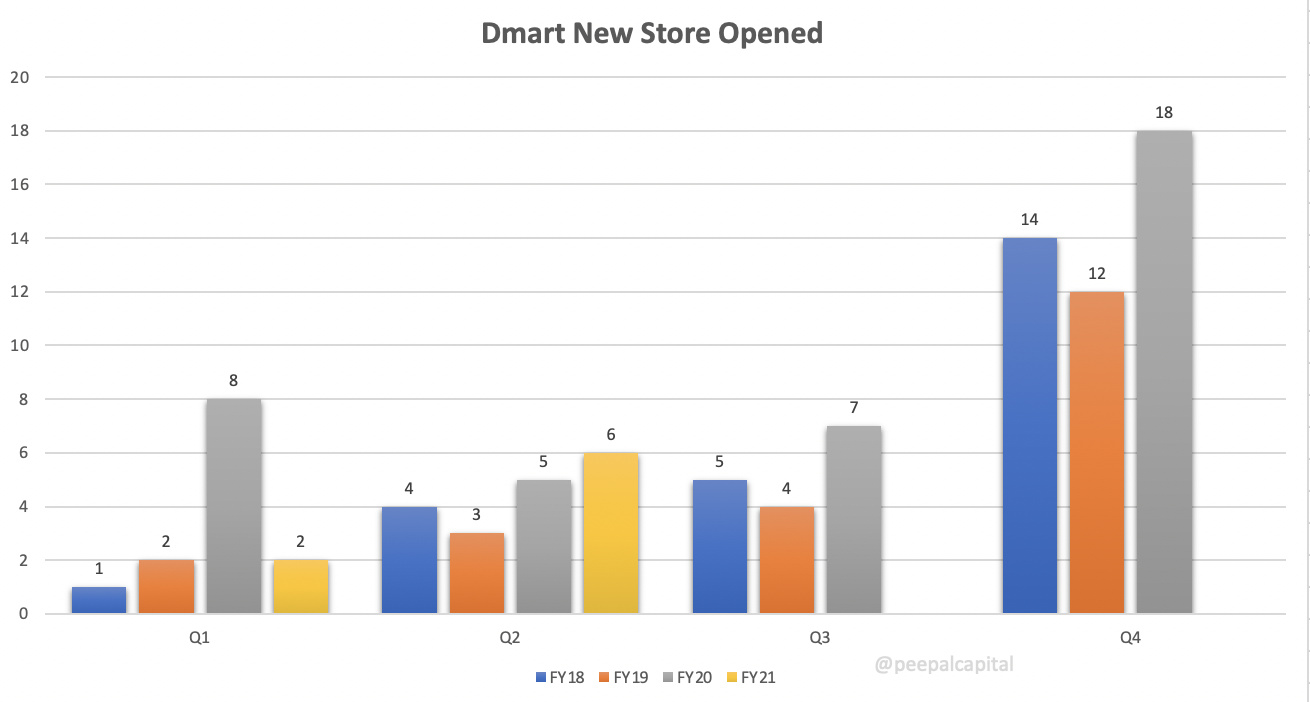

Opened six new DMart stores during the quarter and closed two stores for customers and converted them into fulfillment centers (FC) for ECommerce business. Both closed stores are in Mumbai (One each in Mira Road and Kalyan)

Ecommerce

On one side people criticise that they don’t do online and when they do by getting FC’s done to expand coverage that is portrayed differently. Personally I would not want them to go aggressive in online space.

We continue to increase our footprint in Mumbai Metropolitan Region covering additional pin codes. Mira Road and Kalyan FC addition was to deepen our reach and serve customers better in these regions. We have also expanded our E-Commerce operations in select pin codes of Pune City.

Depending on what our position in any stock is we view the same data & commentary differently. The trick is perhaps to invert.

Yes Deepak I did and you can find mention of MoM sales increase in my post

Regarding stores opening / closing and changing them to FC, I would love if they don’t close the running store & open a fresh FC for Dmart Ready. In history of 2 decades, this is the first quarter when they did close running stores. Isn’t it a big shift from existing trajectory which management was following. I am watching this space closely for new developments.

A rough calculation shows that during pre-covid era, 2 stores did generate revenue of 48 Cr per annum and PAT contribution was approx 6.5 cr. Do we have any commentary from management indicating FCs reaching these levels in how many quarters / years from now.

We need to track this conversion from other angles as well, which gives clarity if management action of conversion of running store to FC for Dmart Ready was for profit improvement or they were forced to convert due to other business reasons.

FMCG and staples sales at all stores higher than YoY in Sept…

General merchandise is at 22.7 % in Q2 compared to 27.3% at 2019 annual contributions.(from insignificant levels in Q1)

Store addition pace at Half year is getting closer to last year. Should catch up at yearly level.

IMO All levers are aligned well to get back to trajectory with festive season kicking in…expect Q3 to be a beat on all fronts, sales & margins. QIP money if used smartly will further add to growth base.

FC setup to support Dmart ready is inline with mgmt comments of experiments in e-commerce. This will likle stay at pilot levels. Immaterial in overall scheme of things for now but still ON.

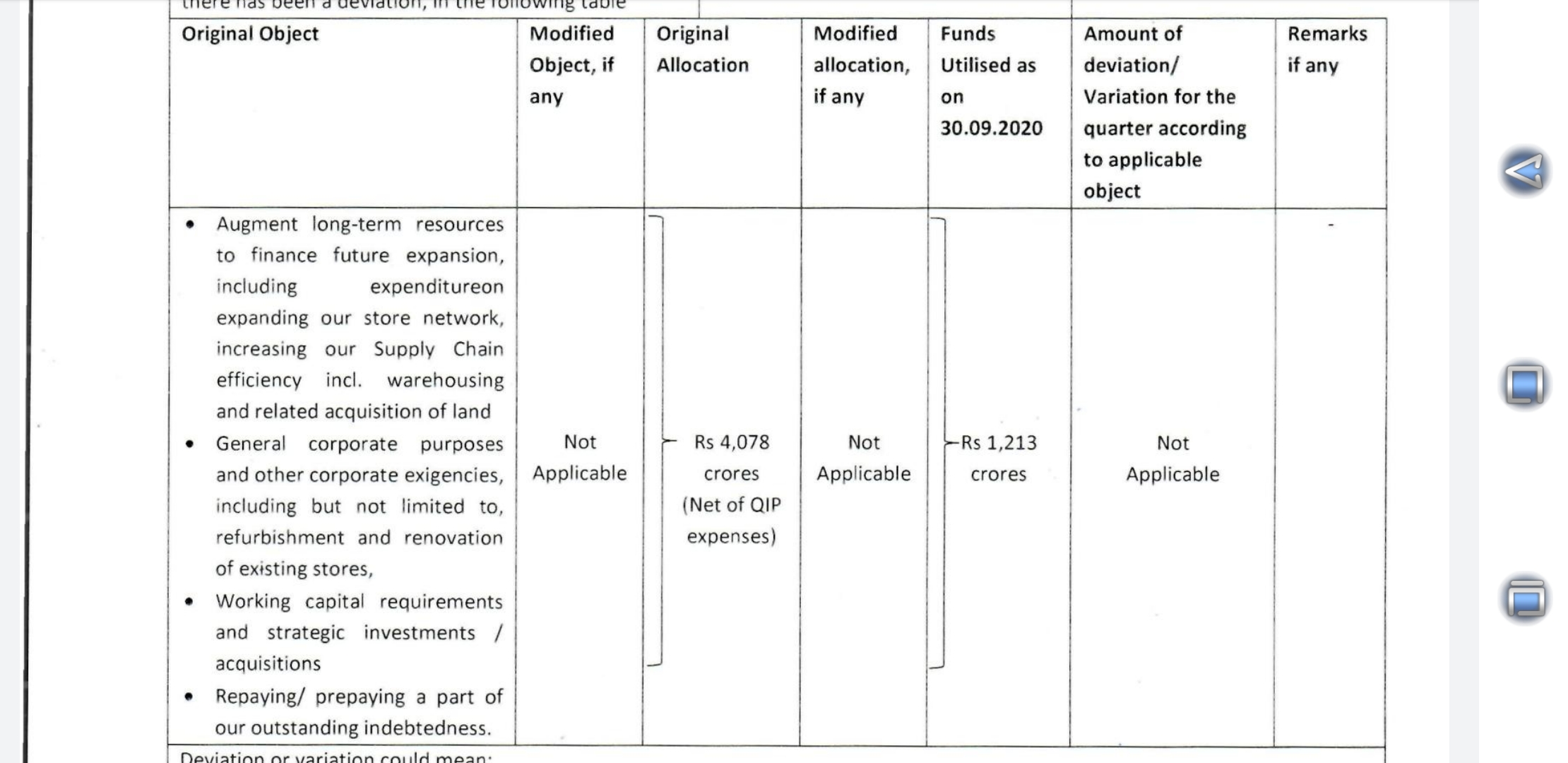

QIP funds utilization update, this is buyers market and land acquisition may have been at favorable terms to Dmart, though Neville did mention in a concall that type of location and quality preferred by Dmart usually dont go cheap - still assuming 25-50Cr as store per land parcel Dmart buys, and majority of spend(1200 cr+ in 6 months) going in land acquisition, a good base is being built for future expansion

One of the things I just couldn’t fathom was as to why they were forced to convert two well established stores into e-commerce inventory holdings instead of purchasing two other lands which could have been present in the city outskirts(as they usually are) , which would have been very cheap too(from acquisition point). Does anyone know about this.

I am no expert and did not go or think deeply through this but first answer which comes to me is in the quality of perishables that a nearby star bazaar supplies online via starquik and what a jiomart or a big basket supplies…there is no match to a near inventory in case of perishables and I personally did not give a second chance to those supplying me inferior quality stuff at home and at inconvinient times…