Interesting take. Although, it will be helpful if you further expand your argument with a couple of examples. What kind of headwinds and regulatory burdens do you think retail industry might face? (especially the brick and mortal retailers)

2 Likes

You speak a lot about regulations hurting Retail industry and compared Retail with regulation heavy Resources PSUs etc. but I could not see any specific regulation mention that did hurt Dmart or any other retail player or the kind of regulations for RETAIL that you fear would come in future.

If you think deeply, government regulations are in every sector. It is just that in which it becomes a leading variable that would matter. Personally this is precisely why I have stayed away from resources, PSUs so far and to an extent with healthcare/pharma as well…but till date have never imagined RETAIL to be a sector where I should fear regulation so much to the extent of selling out or not investing.

Would be great if you put specific points only regarding Retail industry government regulations that are hurting retail at present or may at future and also government motivation that you mention. Thanks

3 Likes

I’ve been asked to explain or give examples of how regulation can impact the retail industry. Well, let us remember a couple of incidents involving government and certain government departments. A few months back the Commerce minister came out with a statement that they will not allow online retailers to indule in predatory pricing (whatever it is) so as to harm the Indian kirana traders. This is fine if principels of predatory pricing is consistently applied. I personally believe regulations should be made based on common principles and not for specific business groups. Here the minister was pitting the kirana traders against online retailers. Anyway.

So I wonder how come a company which makes most of its profits from a highly regulated & government interface industry like petroleum and uses those profits to build a telecom company and uses predatory pricing to ramp up their user base to 100 million subscribers within the timeframe allowed for testing and validation? If predatory pricing is bad, it is bad for every industry and evry company in every industry. Here we see the government and other departments being very flexible with the definition of rules.

We all know that because of the excellent relation DMart maintians with their suppliers they get additional discounts. Now tomorrow the regulators may decide that it is not in the interest of other retailers that suppliers should give additional discount to any one retailer. I have no guarantee that the government cannot bring out such a regulation because our regulations are not based on principles but on protecting groups.

Similarly we know that Dmart runs a highly efficient store system. The government may bring about regulations about distancing between counters and customers in a store or the maximum customers allowed inside a store. Again very likely. DMart will be impacted very badly.

What if the govenment makes it mandatory for retailers to share their algorithms to regulators to investigate any real or imaginary flouting of rules? How will DMart be impacted? All these are not only possible but also probable. When we are paying 100 multiple for a company we expect to be invested in the said company for at least 10 years to make decent returns. If the regulations set back the business even for one year we have a problem.

We will have no problem if the regulatons are based on sound principles and are predictable. So smart companies can compete fairly knowing the rules upfront. But if regulations pit one company against another in the same industry then we have a much bigger problem selecting winners because it is not only smart business strategies which win but also how much the regulatory bodies will allow a particular company to win. I am fearful about that aspect. All these fears may not materialize but in case even some of them materialize over the course of the next few years then our investments can be set back by a significant period.

Basically I do not want government to select winners and losers. I want the markets to do that. If there is apossibility of the former then better give that industry a pass.

7 Likes

To your question about regulations specific to the retail industry. If regulations are standardised for the whole industry then everybody knows the rules upfront and play by it and the smartest ones win. For example in the case of Telecom so long as Jio was less than 30% market share and Airtel and Vodafone above 30% they could not reduce prices because of significant market power (SMP). But Reliance could cross-subsidize, basically using petrochem profits to give Jio for free. It may not have been deliberate but it resulted in one company getting all the advantages.

If all the regulations are known upfront then all competitors can compete fairly. But newer regulations which somehow give advantage to one player distorts the industry dynamics. I’m not saying all these are deliberate but does not give me much comfort. The simple formula for me if Reliance competes in an industry then better get out before it is too late. I fear unfair regulations.

1 Like

In the telecom industry, not all was played fairly.

The below article is an interesting read.

Caveat: The Wire definitely has a left wing bias but the data itself is not incorrect.

1 Like

D Mart has stopped providing home delivery of items in my locality. On website or app they are asking to visit the store in person to make purchase. I believe most of the people are scared of visiting a mall and DMart stores are one of the overcrowded places.

Most of people will still prefer to get items home delivered or will visit store next door.

Is DMart management is missing a trick here to increase revenue and open another revenue stream.

Would we see more drop in sales?

1 Like

Dear Rushikesh

Thank you for your post and Welcome to this forum…

You may be right in your thinking!

A lot of unending debate is being made on this point…

May be if you go through the previous messages by members both for and against … you would get a meaningful insight…

Social media platforms are lately flooded with complaints of late/no delivery by Jiomart. In such unprecedented times there is huge rise in the volumes of orders in E-commerce/food delivery space.

If one has to look at this closely it all really boils down to how efficient the company is at managing inventory at broader level, no wonder amazon has multiple warehouses and co-ordination points to ensure same day or 2 day delivery with prime.

Last mile delivery is very dependent on how the inventory is managed. You can have the most sophisticated software to track but you cannot track it in real-time unless all systems are inter-connected on the backend.

I do believe Reliance is now figuring out all challenges faced by competitors past and present on how to deliver effectively. But since Reliance is flush with money from Jio, I dont expect them to be cost-conscious at the moment as they look to beat out Dmart.

Their day of reckoning will come in 1-2 years time when they have bled a lot of money and then realize that they may have to pivot to something else. Thoughts!

Disc. Not invested

7 Likes

Yes , I ordered couple of time in jio mart few things I gave feedback

Expected delivery date they dont show in app and they take time as you mentioned. There is no express delivery like prime

They missed couple of items in the order and refund is marathon process of emails etc

Mine is big apartment they are not ready to drop in security guard room unlike amazon and others deliver there and message/call us and leave and we pick up later. I was in meeting had to go out due to repeated calls from their delivery man.

This means they will take time to improve on these things.

Article talks about Dmart eCommerce revenue & losses.

http://upflow.co/l/IkLL/news/food-entertainment/grocery/dmarts-ecommerce-unit-doubles-sales-but-loss-widenes-too/77341967utm_source=dlvr.it&utm_medium=twitter

Good to see D-Mart management sticking to their competence and not getting wildly experimental. That being said, D-Mart’s super has high PE finally started raising some eye-brows and the stock may no longer command former valuations at least until the crisis is fully dealt with. Brokerages have already started throwing the towel from Buy/Overweight Calls to Underperform/Sell Calls. The Outlook is not very positive.

Disl: Exited last week

Hi

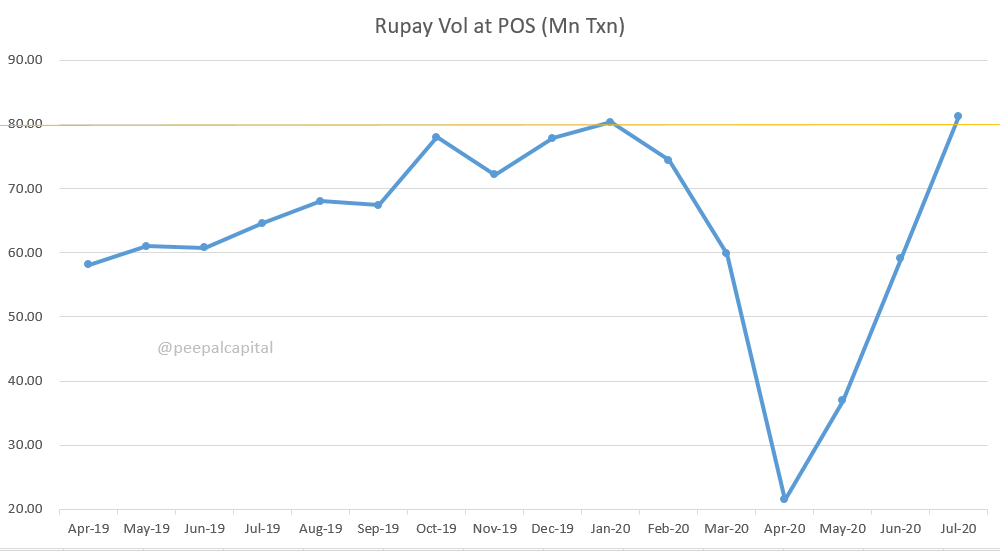

I was looking at the earliest data I could get hold on to gauge physical retail sales. Rupay card transactions have reached lifetime high in the month of July (previous high in Jan '20). Rupay is the dominat market player in the 835+ Mn cards in force in the country thus a good proxy for consumption. Unfortunately RBI data for all cards comes with a delay of 2 odd months.

Aside.

Most of us expected Dmart to start aggressive online deliveries during the lockdown period and were dissatisfied that Dmart could not or did not intend to scale & put resources into online delivery. One of my friends whose parents stay in Bombay told me that Dmart was focusing on apartment based deliveries. This resonated with me. As I have seen this to be successful in a startup I am invested in (same grocery/milk delivery). Folks from Bombay can confirm.

This online grocery space is filled especially in the metro cities and even food delivery startups whose businesses are languishing have switched to grocery delivery (eg swiggy). Online delivery of perishables is a cash guzzling machine. As an investor in Dmart I would not want them to enter this business yet.

Also with new companies taking on the 100 PE tag people seem to have forgotten Dmart bashing. Neither it is part of any ‘cans’.

Let us see how the future pans out. I only hope the management executes as efficiently as possible in their core areas of strengths.

Rgds

Disc: continue to be invested since IPO. Not registered for any advisory services.

9 Likes

just one addition, Rupay is also a player in online payments so may not truly reflect physical retail sales as data would include both physical and online transactions via Rupay. Thanks

This is physical POS data. Ecom numbers are separate.

I have been tracking payments data since 2012 as I am from this industry.

Rgds

4 Likes

Allright, this is excellent insight. Physical POS data is above its pre lockdown phase is encouraging. Would be great if you can share e-commerce similar data as well, if you have and it can be shared. For ecommerce, I see it is generally dominated by CCAvenues and Rupay (until sometime back it was mostly CCavenues only). My observations are only from consumer perspective. Would be great to have your insights as a specialist here. Thanks!

1 Like

Key notes for upcoming quarters

- Working to expand the company’s network into new cities

- New store construction activities hit by lockdown & social distancing norms imposed

- Some store openings slated for this year will have to be pushed to the next year

- Opened 38 stores in FY 2019-20 due to ‘some’ rollover from the previous year (they could open only 21 in FY 2018-19)

- Total 59 stores added in last 2 years … expect similar addition in next 2 years - so no growth in store addition

- Old stores had 30k sqft size but newer ones are 50k sqft

- Larger store size is giving better returns in medium & long term

- Brand has matured and new cities are returning larger absolute sales numbers much earlier

- Small stores tend to peak out faster and find difficult to keep growing due to their physical inability to support more customers

- CAGR has flattened to single digit… it will just grow at inflation rate or lower … to address this they are opening larger stores

- key downside to open larger stores is that initial construction related costs are higher but looking at capital expenditure needed to put up a large store in relation to revenue generated by the store, it actually tends to be lower and therefore more economical

- Other-way… to double the revenue (& Profit) generated by a store, the company doesn’t have to double its investment in it… its not a proportionate increase in capital expenses

- They are no longer averse to looking at rental properties, given the correction seen in the real estate market

8 Likes

Come December , there is going to be another Giant Online Stores / E- Commerce platform to take on Reliance & Amazon.

Yes , all Tata Consumer Products, Star Bazzar, Trent …Groceries, Salt, dress material , vegetables, fruits …everything under the Sun and Moon would be available under one TATA Super App…

1 Like

This is indeed very interesting. I read about it few months back in one of Chandra’s interviews. Just thinking loud, if this would be a collection of apps like say a star quik, croma, Tata Aig etc together in one app with backward integration in place or something totally new? What this would mean is that say the revenue generated from a click on croma and digital sales would belong 100% to croma or to the entity which owns this app and hence owns a significant cut in the revenues?

This brings me to the second most important question for me now…which Tata entity would own this super app and responsible for its innovations, cost and finally the revenue cuts, if any!

- Regarding effect on Dmart - I would reiterate what I have been saying multiple times. Pie is huge, runway is huge and all light ships of decent size & strong sails will reach the shores. Infact, with such clutter in online space, it makes even more sense to focus on its inherent strengths of offline retail and come back with a bang when pandemic situation normalizes.

Disc: Invested in both Trent and Dmart. Looking for opportunities to add more. This is not a buy/sell recommendation and views are biased.

Hi

Thought to chime in.

For the ‘superapps’ being done by any Indian entity be it Reliance or Tata there is one significant advantage from an e-commerce perspective (FDI regulations) and multiple problems they will have to solve in order to actually bring world class customer service. For a B2C tech product the customer is all that matters. If a product does not offer selection, convenience and pricing benefits he will not stick around to a company’s offering.

Let me take an example Reliance, under Jio it started its Payments app Jio Pay almost 6+ years back. The market was filled with promise. The app ‘improved’ over the years but is not as good as an app a few kids can make in a fortnight. I think they wouldn’t even have 5% retail market share. Jiomart website looks super nice. But the feedback of delivery, quality and returns have been poor when compared to bigbasket. Now the counter is that they will improve. Yes they will. So will the competition. Tata already ventured into e-commerce but that was a failure. Fashion as a category I guess only Myntra cracked. Multiple examples. It is like saying why couldn’t have HDFC bank done a PayTM given the strategic advantage of a scheduled commerical banking license.

The answer is only one thing - execution.

These super apps are all inspired by China. Checkout something called WeChat Mini Programs. That’s another universe out there.

Coming to the company of this thread. I personally believe like some gentelman has said earlier the retail offline pie is large. And I hope that Dmart sticks to its core competencies and doesn’t venture into e-tailing. The game is stacked against them in the online world. Investors will shun Dmart if it burns cash to establish a ‘large’ online business. That is the not the reason for our investement in Dmart. I don’t want to take the often quoted example of Walmart and physical retail again.

Rgds

Edit: Sorry forgot to disclose my views are biased because I have a position in dmart.

12 Likes